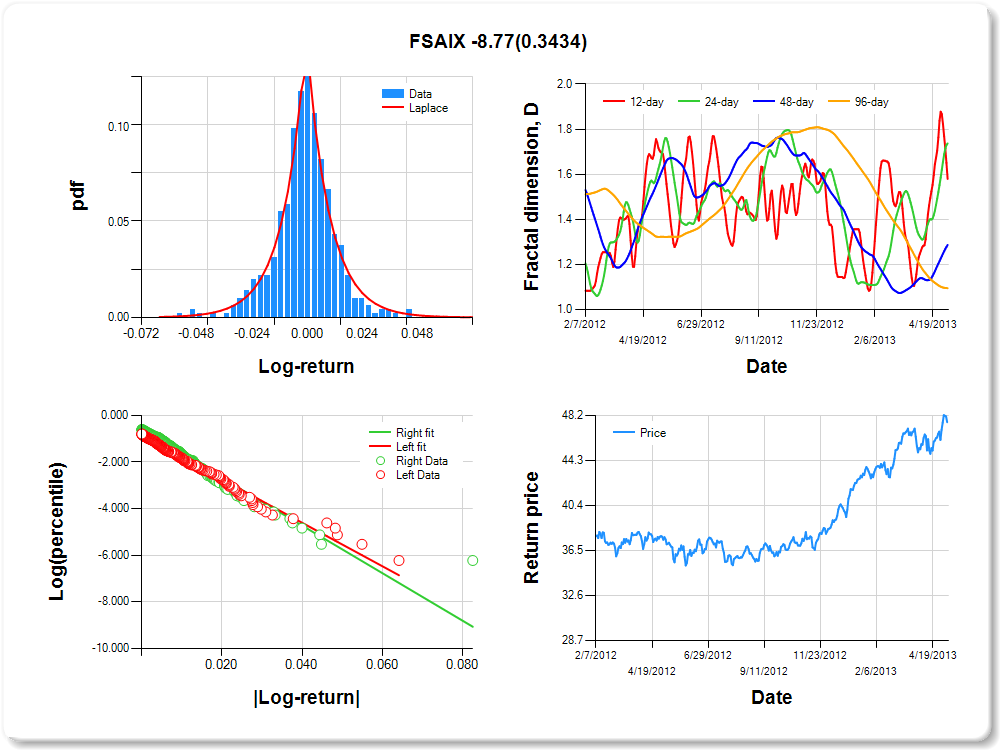

FSAIX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.05 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.04 |

0.00 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.190 |

0.233 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.868 |

0.093 |

-9.360 |

0.0000 |

|log-return| |

-93.090 |

6.523 |

-14.271 |

0.0000 |

I(right-tail) |

0.232 |

0.127 |

1.828 |

0.0681 |

|log-return|*I(right-tail) |

-8.771 |

9.249 |

-0.948 |

0.3434 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.421 |

0.263 |

0.714 |

0.905 |

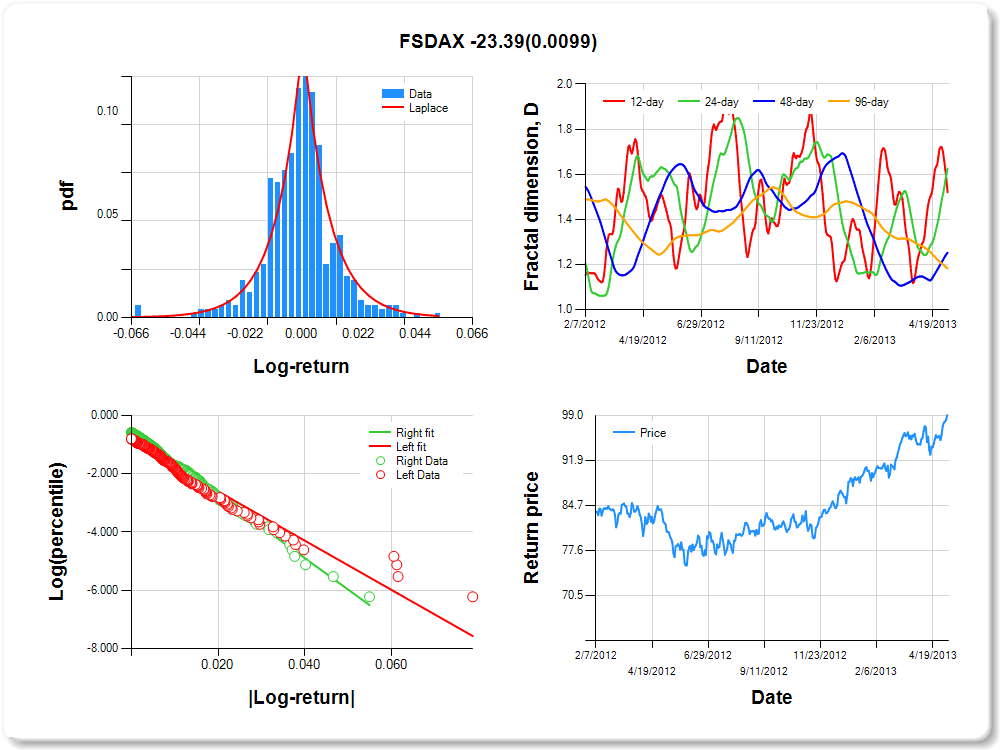

FSDAX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.04 |

2.41 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.347 |

0.254 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.916 |

0.092 |

-9.998 |

0.0000 |

|log-return| |

-84.560 |

6.041 |

-13.999 |

0.0000 |

I(right-tail) |

0.337 |

0.126 |

2.682 |

0.0076 |

|log-return|*I(right-tail) |

-23.387 |

9.033 |

-2.589 |

0.0099 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.480 |

0.375 |

0.748 |

0.818 |

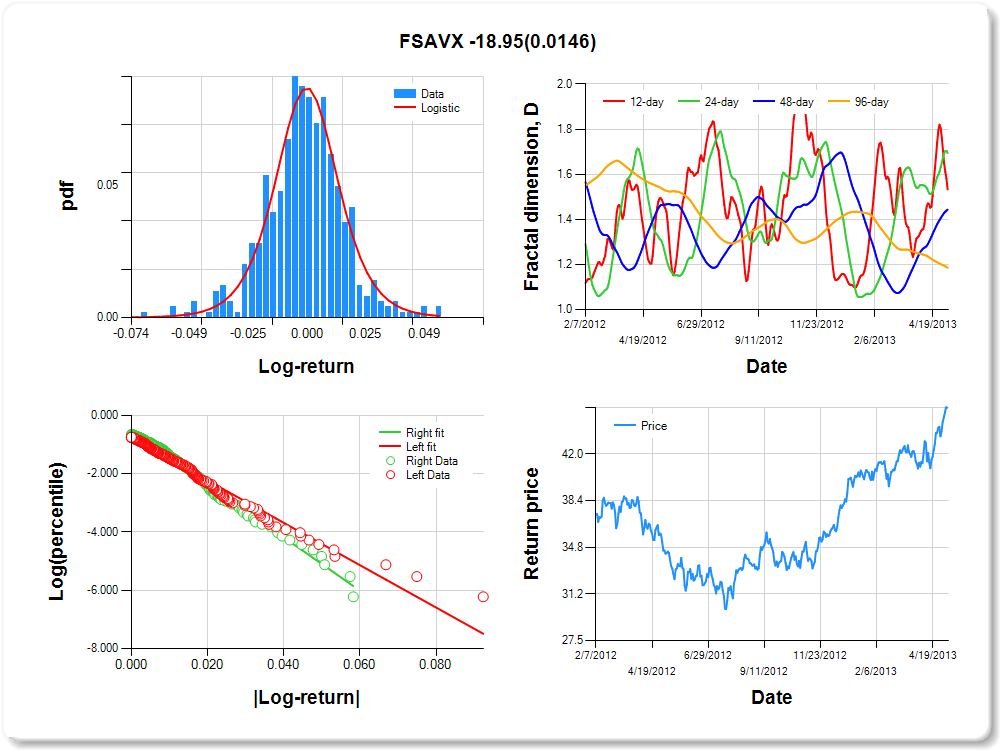

FSAVX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.05 |

1.38 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.416 |

0.198 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.767 |

0.093 |

-8.256 |

0.0000 |

|log-return| |

-72.639 |

4.967 |

-14.623 |

0.0000 |

I(right-tail) |

0.265 |

0.134 |

1.980 |

0.0482 |

|log-return|*I(right-tail) |

-18.946 |

7.732 |

-2.450 |

0.0146 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.467 |

0.306 |

0.557 |

0.815 |

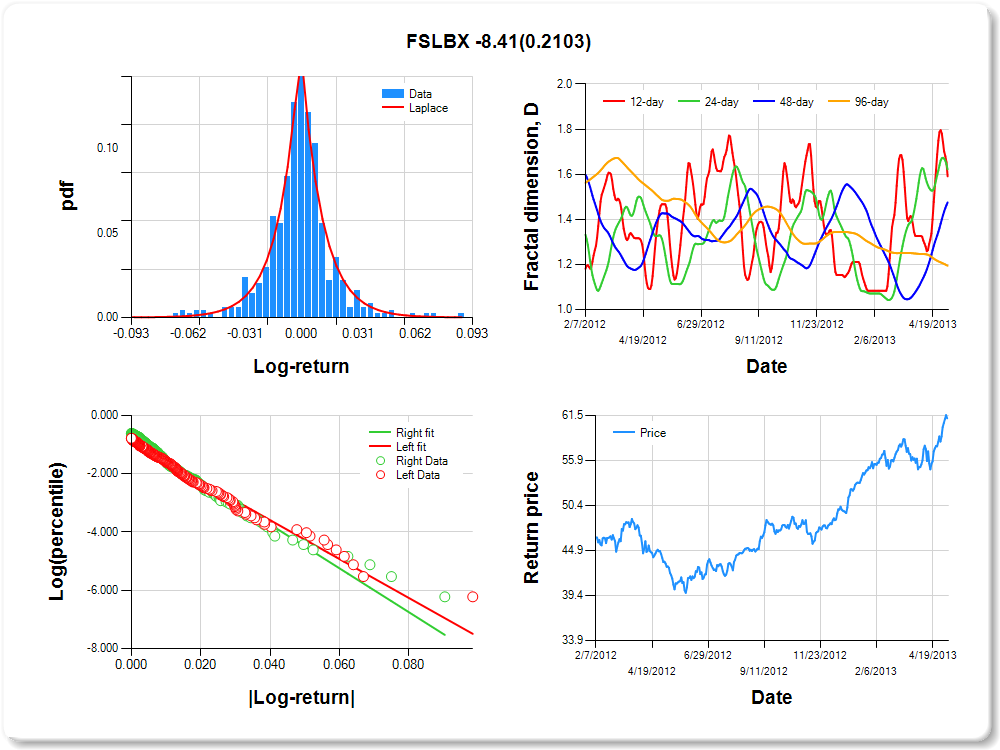

FSLBX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.06 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.06 |

3.51 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.092 |

0.212 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.916 |

0.089 |

-10.252 |

0.0000 |

|log-return| |

-66.780 |

4.662 |

-14.325 |

0.0000 |

I(right-tail) |

0.188 |

0.122 |

1.541 |

0.1240 |

|log-return|*I(right-tail) |

-8.413 |

6.706 |

-1.254 |

0.2103 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.409 |

0.378 |

0.525 |

0.806 |

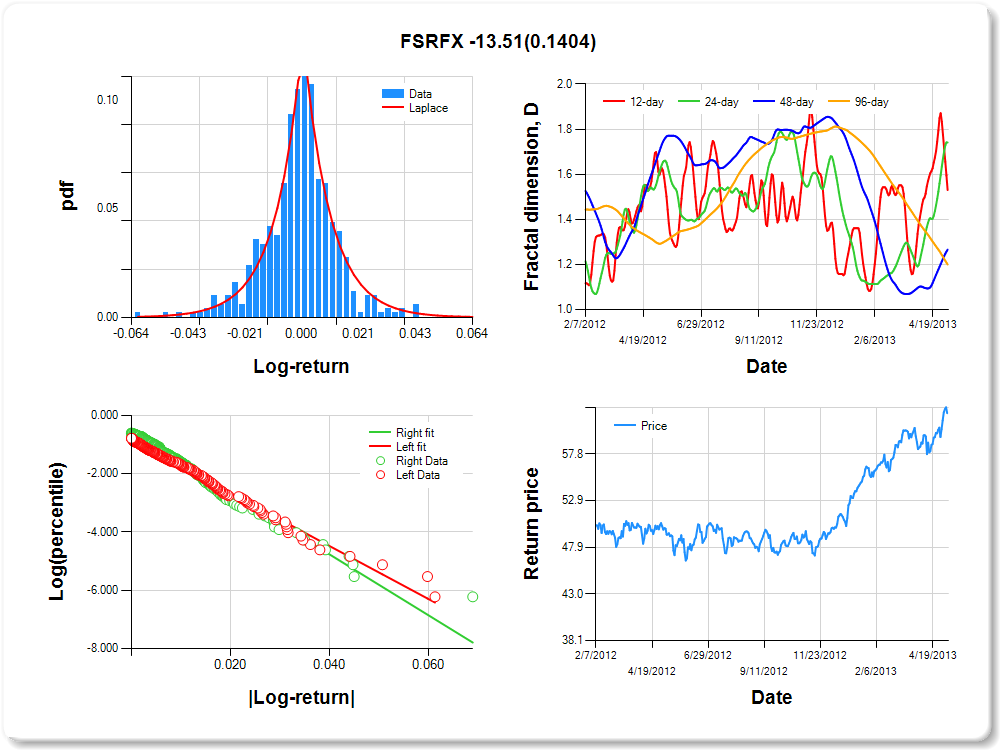

FSRFX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

2.16 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.057 |

0.266 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.828 |

0.093 |

-8.886 |

0.0000 |

|log-return| |

-90.995 |

6.311 |

-14.419 |

0.0000 |

I(right-tail) |

0.256 |

0.129 |

1.986 |

0.0476 |

|log-return|*I(right-tail) |

-13.515 |

9.152 |

-1.477 |

0.1404 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.470 |

0.259 |

0.734 |

0.800 |

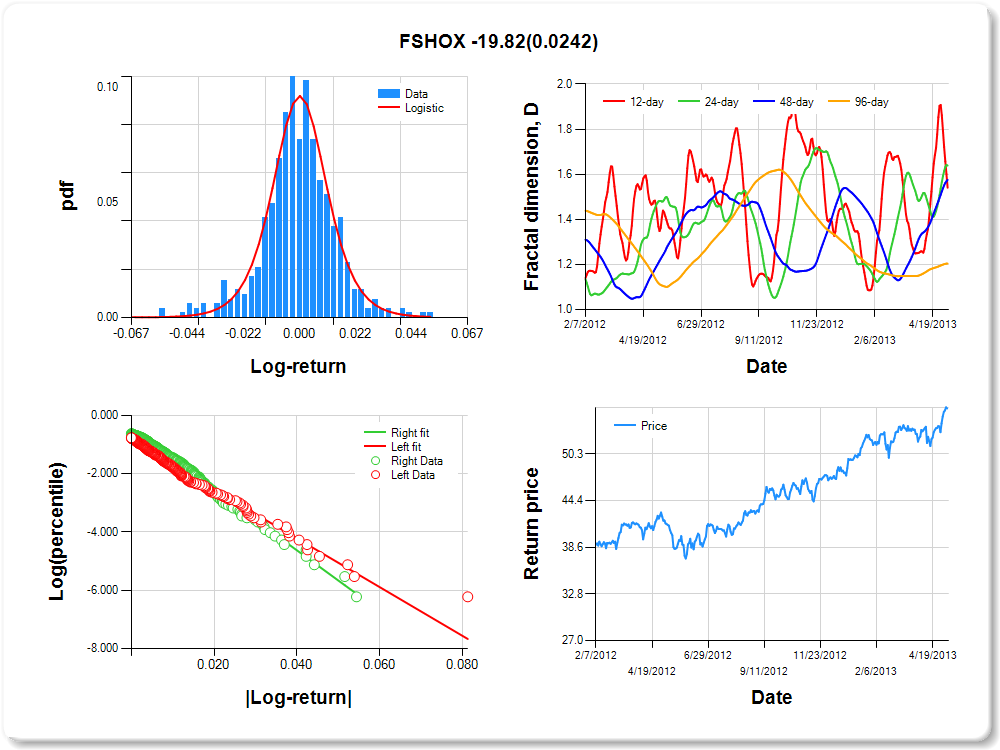

FSHOX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.03 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.04 |

1.58 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.376 |

0.178 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.865 |

0.090 |

-9.606 |

0.0000 |

|log-return| |

-83.577 |

5.776 |

-14.471 |

0.0000 |

I(right-tail) |

0.387 |

0.131 |

2.953 |

0.0033 |

|log-return|*I(right-tail) |

-19.821 |

8.764 |

-2.262 |

0.0242 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.459 |

0.361 |

0.425 |

0.796 |

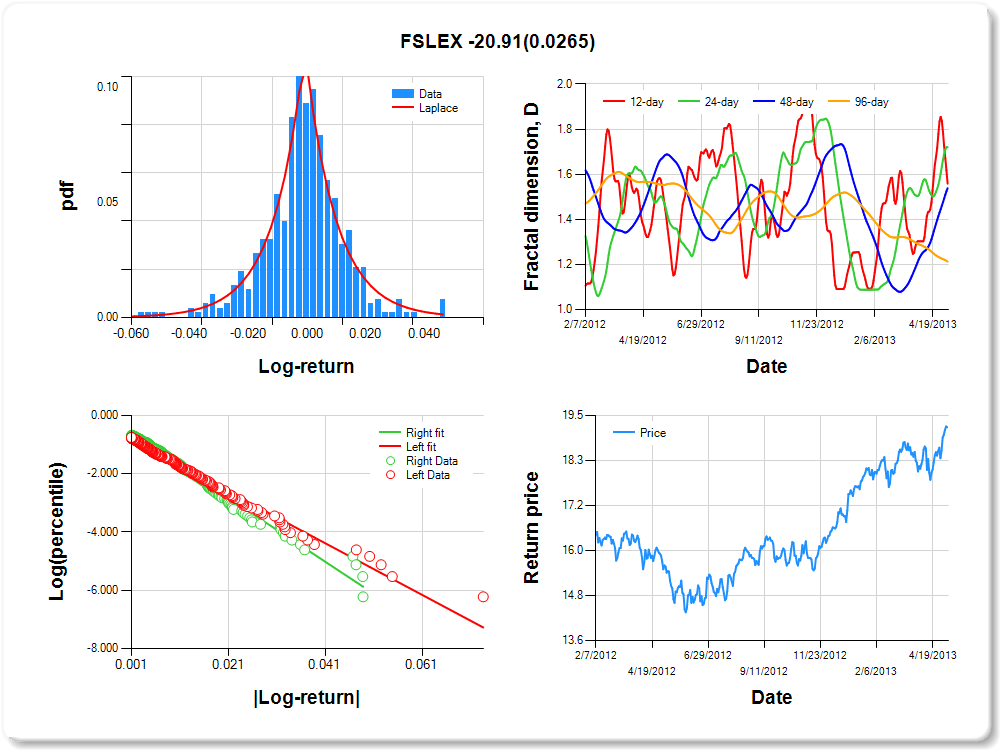

FSLEX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.05 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

3.44 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.360 |

0.294 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.799 |

0.092 |

-8.701 |

0.0000 |

|log-return| |

-88.618 |

6.060 |

-14.623 |

0.0000 |

I(right-tail) |

0.213 |

0.132 |

1.611 |

0.1078 |

|log-return|*I(right-tail) |

-20.912 |

9.398 |

-2.225 |

0.0265 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.442 |

0.280 |

0.461 |

0.787 |

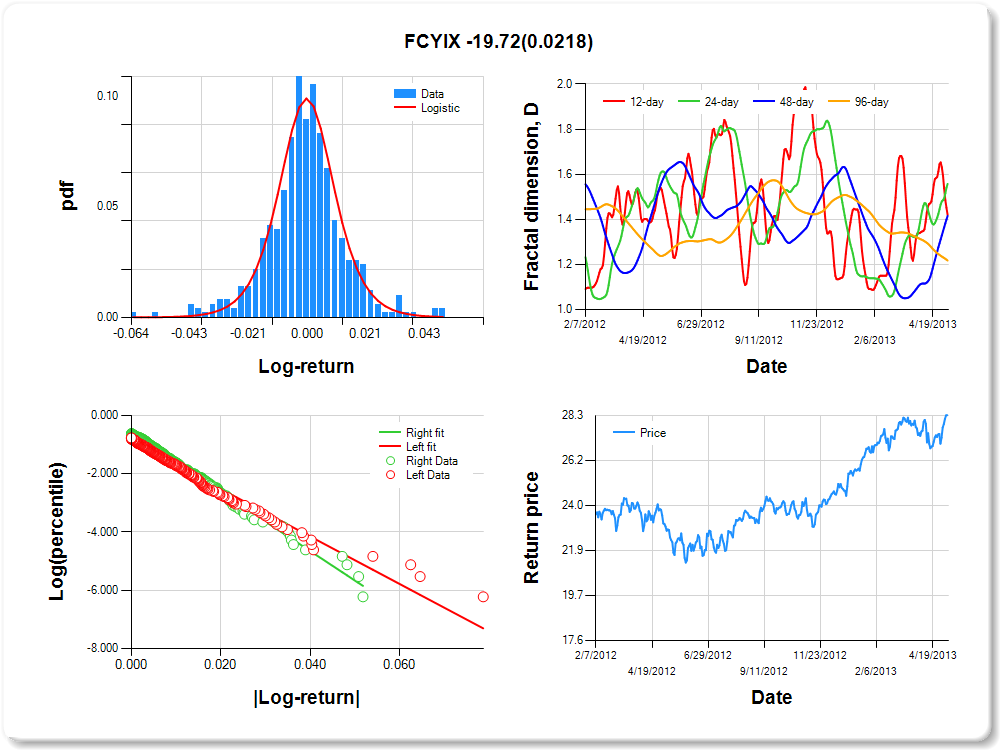

FCYIX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.04 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

3.17 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.380 |

0.174 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.874 |

0.090 |

-9.688 |

0.0000 |

|log-return| |

-81.527 |

5.659 |

-14.407 |

0.0000 |

I(right-tail) |

0.295 |

0.127 |

2.319 |

0.0208 |

|log-return|*I(right-tail) |

-19.725 |

8.573 |

-2.301 |

0.0218 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.580 |

0.442 |

0.585 |

0.783 |

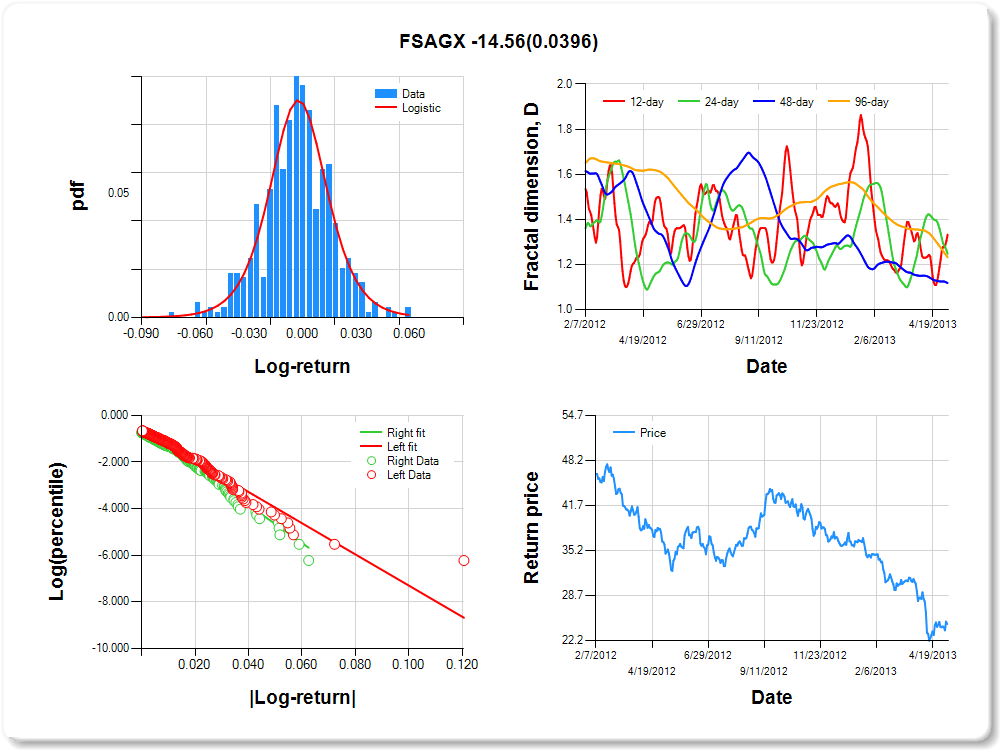

FSAGX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.05 |

2.23 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.531 |

0.197 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.610 |

0.093 |

-6.556 |

0.0000 |

|log-return| |

-66.830 |

4.420 |

-15.119 |

0.0000 |

I(right-tail) |

0.028 |

0.137 |

0.204 |

0.8385 |

|log-return|*I(right-tail) |

-14.559 |

7.058 |

-2.063 |

0.0396 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.668 |

0.753 |

0.882 |

0.768 |

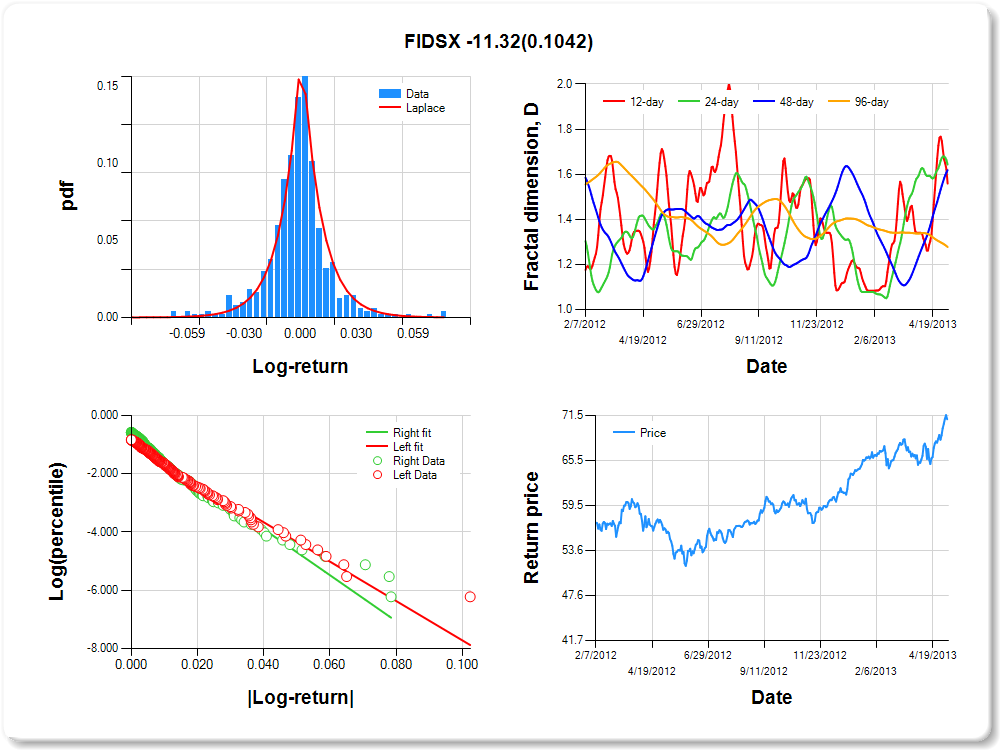

FIDSX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.06 |

4.50 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.268 |

0.193 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.959 |

0.092 |

-10.420 |

0.0000 |

|log-return| |

-67.552 |

4.856 |

-13.910 |

0.0000 |

I(right-tail) |

0.214 |

0.121 |

1.765 |

0.0782 |

|log-return|*I(right-tail) |

-11.315 |

6.950 |

-1.628 |

0.1042 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.441 |

0.356 |

0.382 |

0.723 |

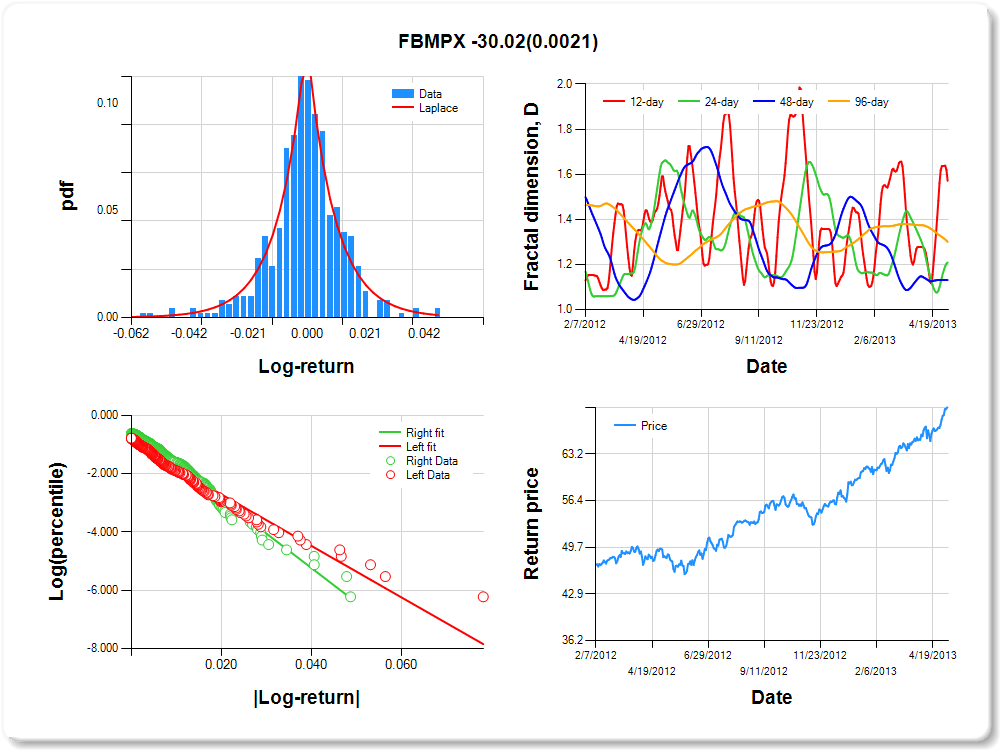

FBMPX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.05 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.04 |

0.86 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.424 |

0.263 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.937 |

0.088 |

-10.632 |

0.0000 |

|log-return| |

-88.263 |

6.185 |

-14.271 |

0.0000 |

I(right-tail) |

0.446 |

0.128 |

3.474 |

0.0006 |

|log-return|*I(right-tail) |

-30.018 |

9.726 |

-3.086 |

0.0021 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.429 |

0.791 |

0.869 |

0.700 |

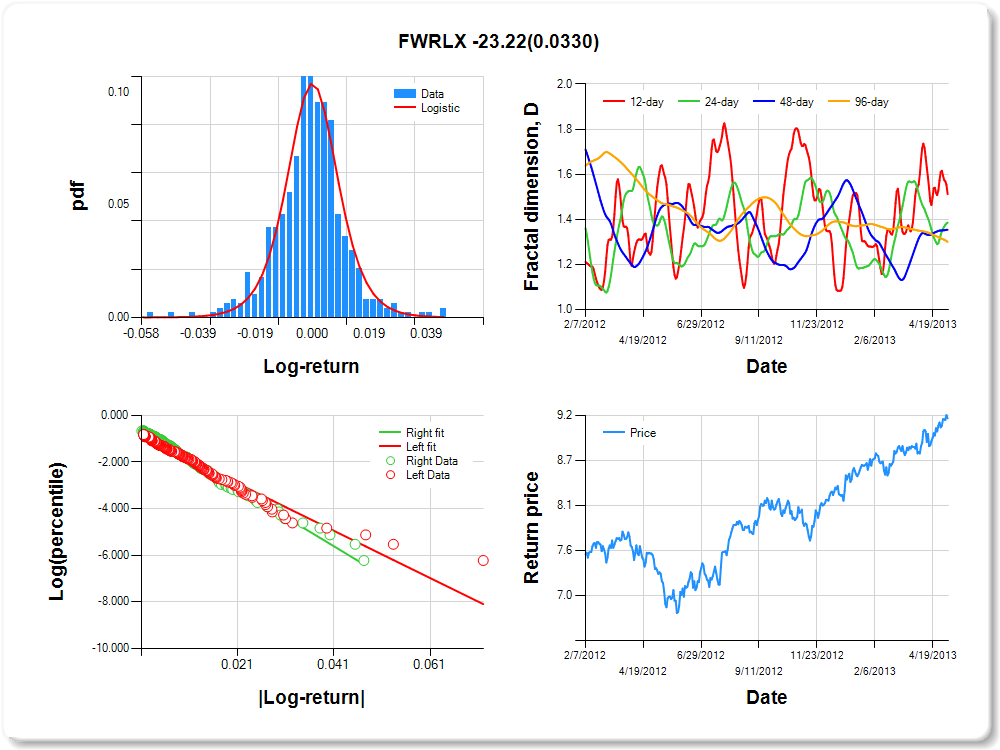

FWRLX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.03 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.04 |

1.90 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.393 |

0.165 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.839 |

0.097 |

-8.658 |

0.0000 |

|log-return| |

-101.121 |

7.252 |

-13.944 |

0.0000 |

I(right-tail) |

0.283 |

0.135 |

2.087 |

0.0374 |

|log-return|*I(right-tail) |

-23.221 |

10.858 |

-2.139 |

0.0330 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.488 |

0.615 |

0.646 |

0.700 |

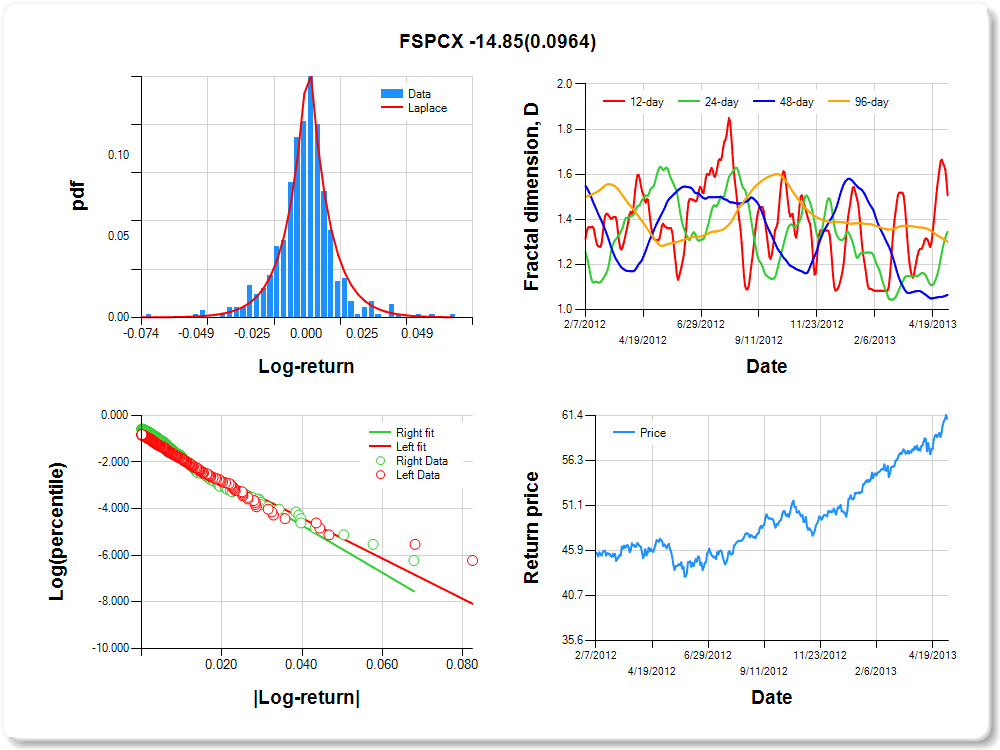

FSPCX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.04 |

2.67 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.214 |

0.203 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.956 |

0.091 |

-10.481 |

0.0000 |

|log-return| |

-86.197 |

6.208 |

-13.885 |

0.0000 |

I(right-tail) |

0.285 |

0.123 |

2.309 |

0.0213 |

|log-return|*I(right-tail) |

-14.851 |

8.915 |

-1.666 |

0.0964 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.493 |

0.655 |

0.935 |

0.699 |

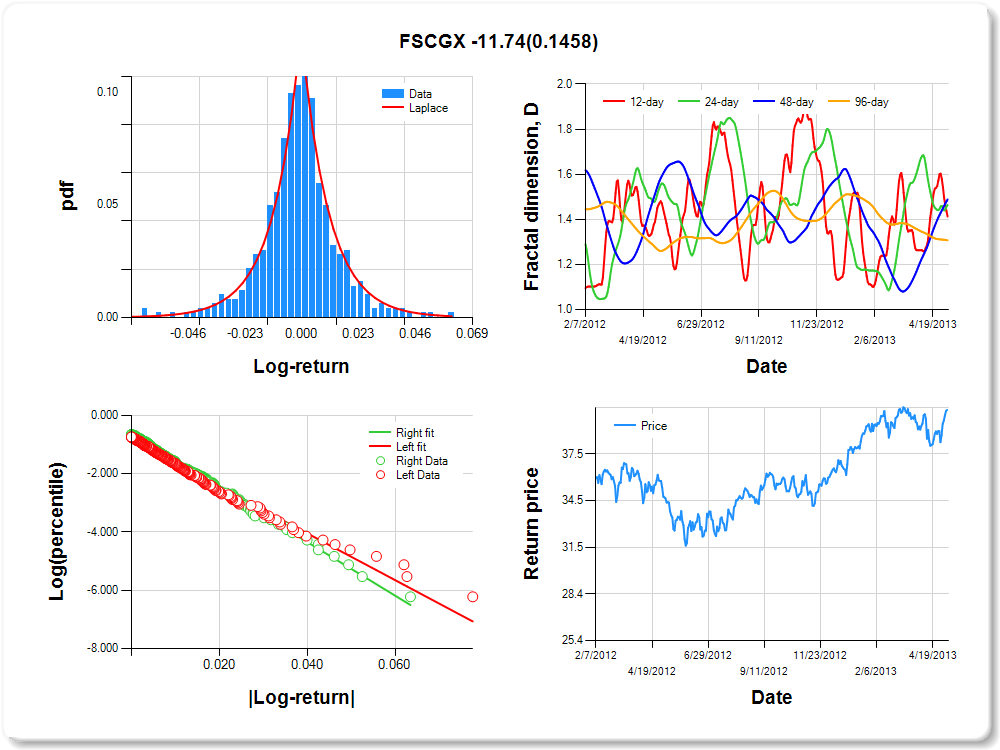

FSCGX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.04 |

0.05 |

3.75 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.196 |

0.271 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.823 |

0.089 |

-9.222 |

0.0000 |

|log-return| |

-80.246 |

5.450 |

-14.723 |

0.0000 |

I(right-tail) |

0.175 |

0.126 |

1.383 |

0.1672 |

|log-return|*I(right-tail) |

-11.740 |

8.060 |

-1.457 |

0.1458 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.587 |

0.536 |

0.512 |

0.693 |

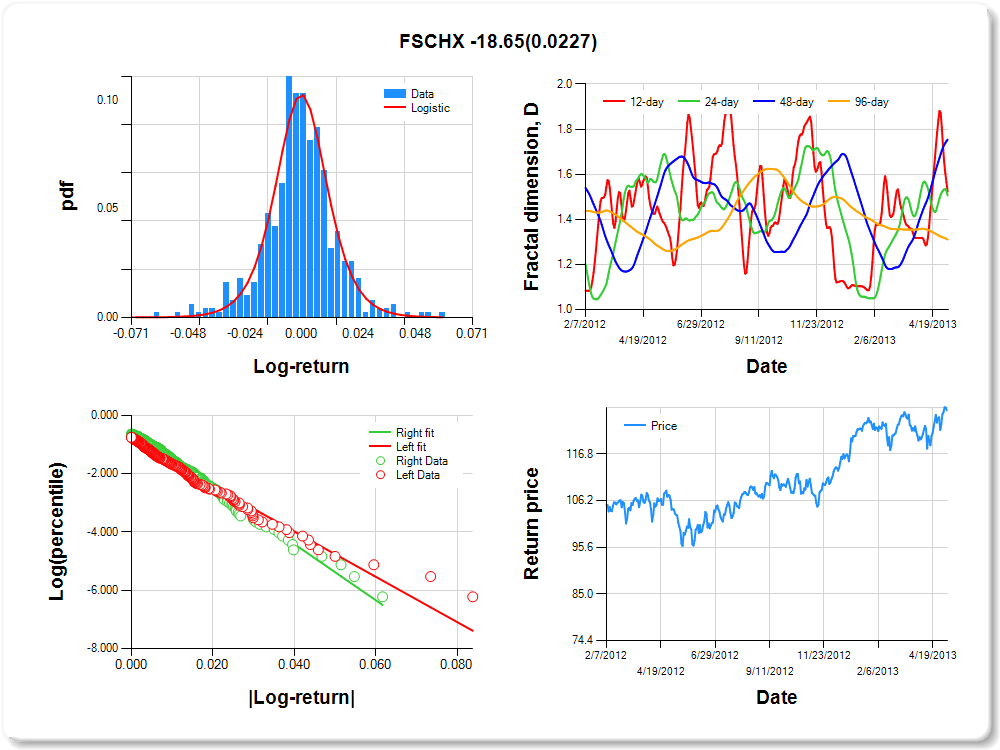

FSCHX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.04 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

1.90 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.288 |

0.167 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.873 |

0.088 |

-9.890 |

0.0000 |

|log-return| |

-77.705 |

5.331 |

-14.576 |

0.0000 |

I(right-tail) |

0.317 |

0.128 |

2.478 |

0.0136 |

|log-return|*I(right-tail) |

-18.653 |

8.160 |

-2.286 |

0.0227 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.477 |

0.493 |

0.246 |

0.689 |

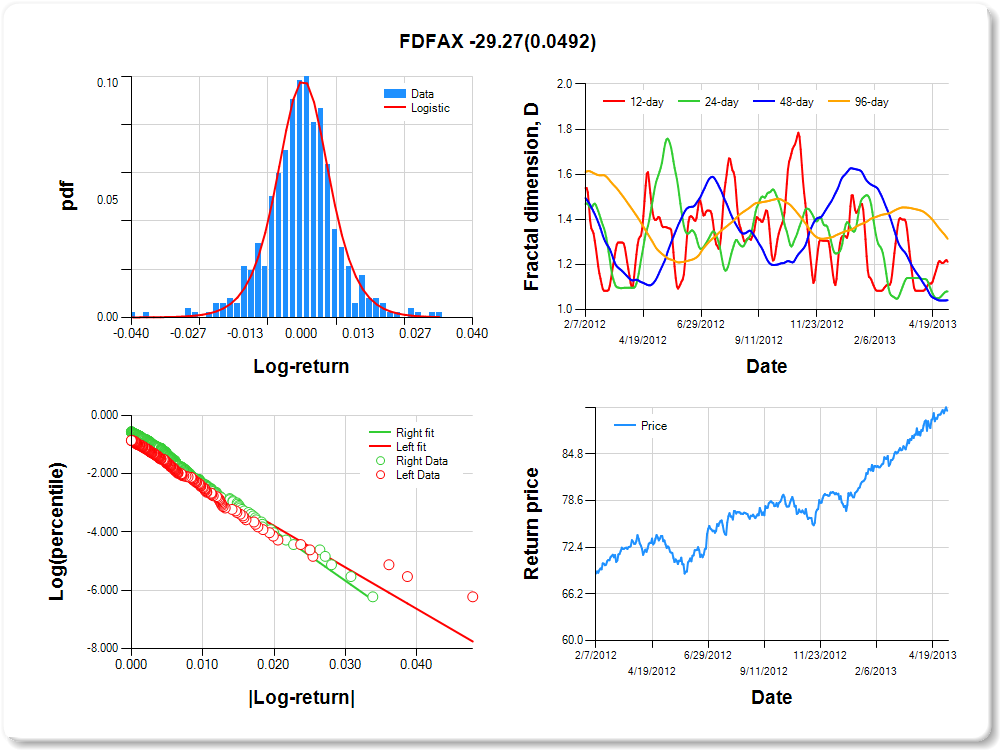

FDFAX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.01 |

0.02 |

0.03 |

1.37 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.340 |

0.170 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.929 |

0.096 |

-9.672 |

0.0000 |

|log-return| |

-142.470 |

10.437 |

-13.651 |

0.0000 |

I(right-tail) |

0.421 |

0.130 |

3.244 |

0.0013 |

|log-return|*I(right-tail) |

-29.273 |

14.846 |

-1.972 |

0.0492 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.788 |

0.919 |

0.958 |

0.686 |

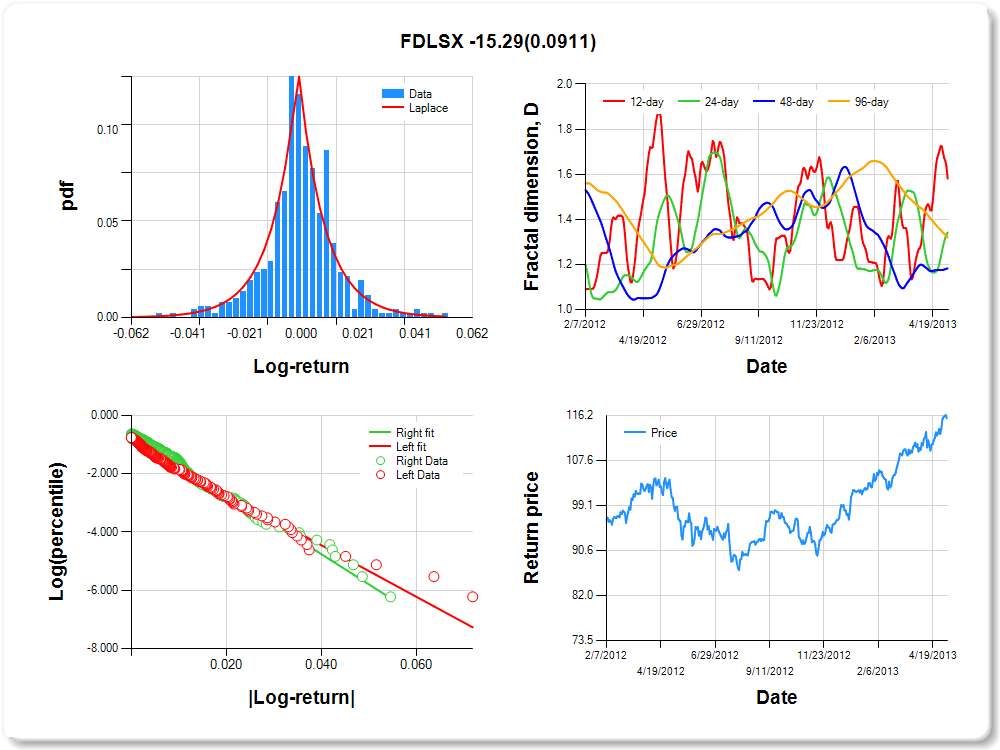

FDLSX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.02 |

0.04 |

0.04 |

2.13 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.233 |

0.259 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.918 |

0.087 |

-10.568 |

0.0000 |

|log-return| |

-88.546 |

6.097 |

-14.523 |

0.0000 |

I(right-tail) |

0.307 |

0.125 |

2.463 |

0.0141 |

|log-return|*I(right-tail) |

-15.293 |

9.034 |

-1.693 |

0.0911 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.419 |

0.657 |

0.817 |

0.680 |

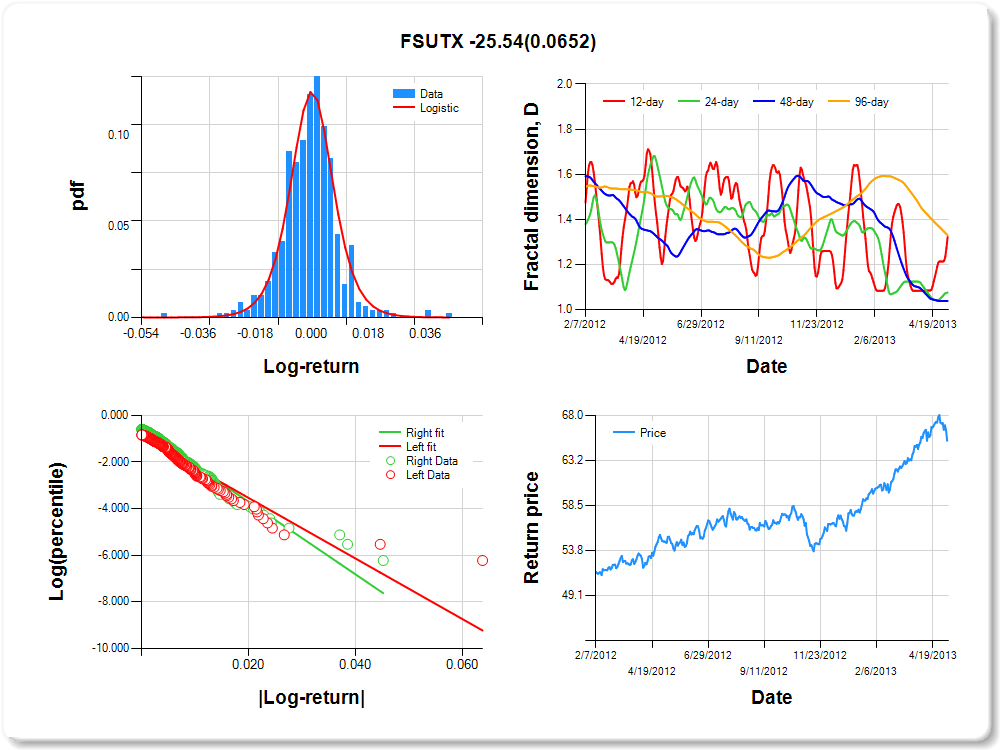

FSUTX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.03 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.01 |

0.02 |

0.03 |

2.26 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.323 |

0.138 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.931 |

0.095 |

-9.777 |

0.0000 |

|log-return| |

-129.733 |

9.694 |

-13.383 |

0.0000 |

I(right-tail) |

0.347 |

0.129 |

2.686 |

0.0075 |

|log-return|*I(right-tail) |

-25.540 |

13.819 |

-1.848 |

0.0652 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.678 |

0.924 |

0.962 |

0.671 |

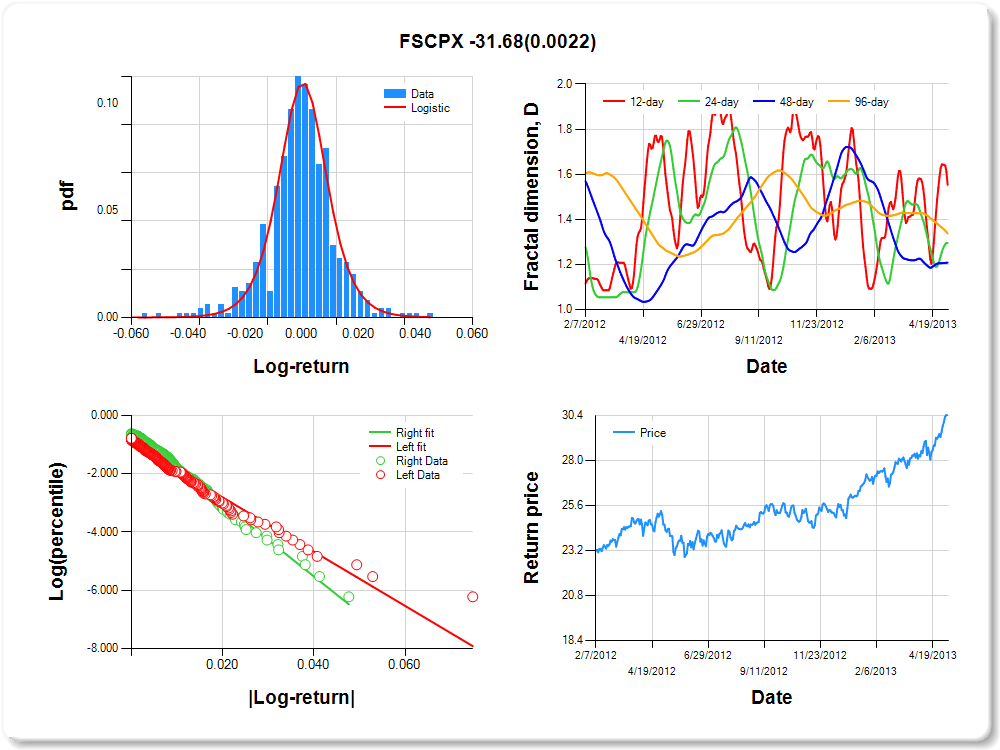

FSCPX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.04 |

2.72 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.421 |

0.156 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.922 |

0.089 |

-10.340 |

0.0000 |

|log-return| |

-93.055 |

6.522 |

-14.268 |

0.0000 |

I(right-tail) |

0.430 |

0.130 |

3.302 |

0.0010 |

|log-return|*I(right-tail) |

-31.680 |

10.293 |

-3.078 |

0.0022 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.447 |

0.704 |

0.792 |

0.662 |

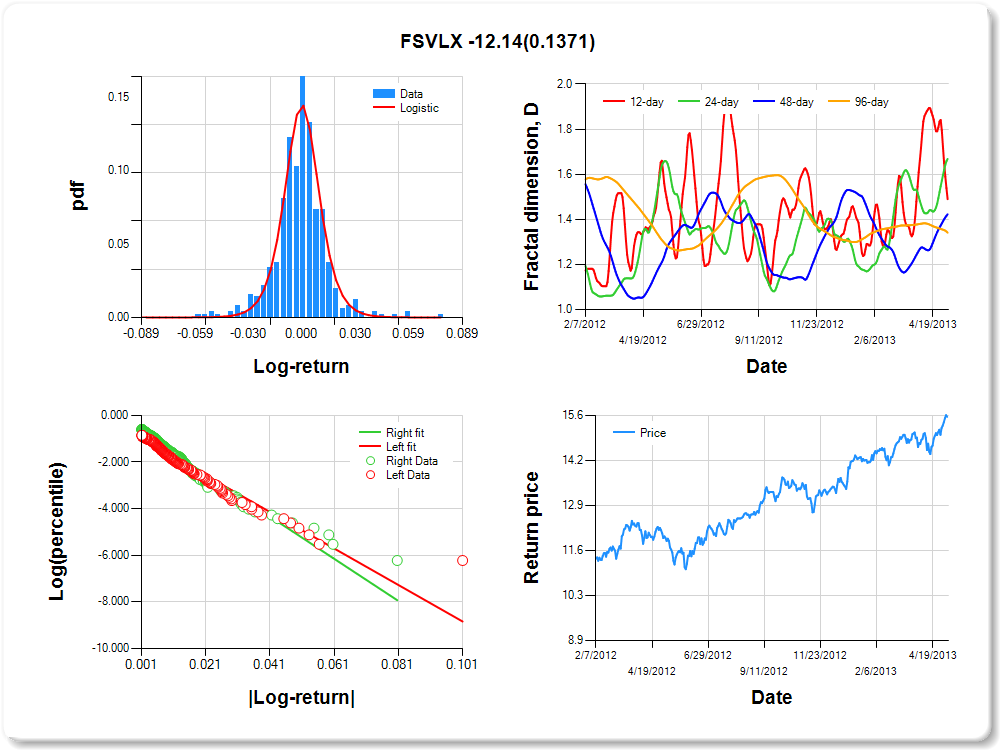

FSVLX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.05 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.06 |

2.46 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.224 |

0.118 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.975 |

0.094 |

-10.404 |

0.0000 |

|log-return| |

-78.059 |

5.765 |

-13.539 |

0.0000 |

I(right-tail) |

0.297 |

0.126 |

2.357 |

0.0188 |

|log-return|*I(right-tail) |

-12.142 |

8.154 |

-1.489 |

0.1371 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.510 |

0.332 |

0.577 |

0.659 |

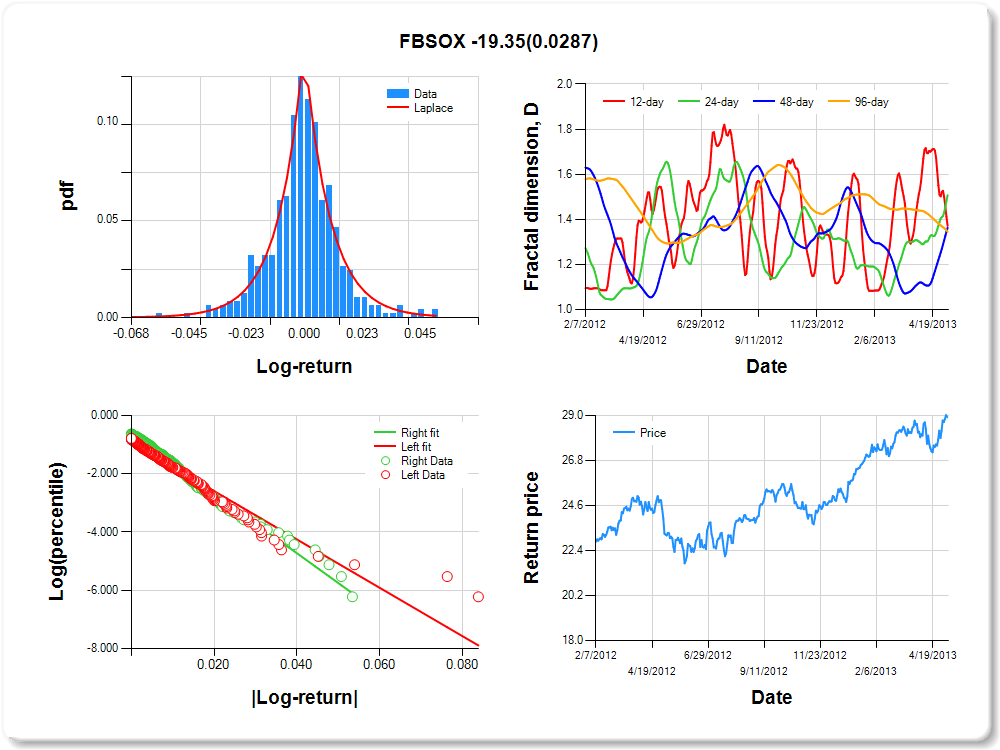

FBSOX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

1.12 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.406 |

0.249 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.915 |

0.090 |

-10.115 |

0.0000 |

|log-return| |

-82.907 |

5.891 |

-14.073 |

0.0000 |

I(right-tail) |

0.307 |

0.127 |

2.412 |

0.0162 |

|log-return|*I(right-tail) |

-19.352 |

8.817 |

-2.195 |

0.0287 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.629 |

0.492 |

0.637 |

0.655 |

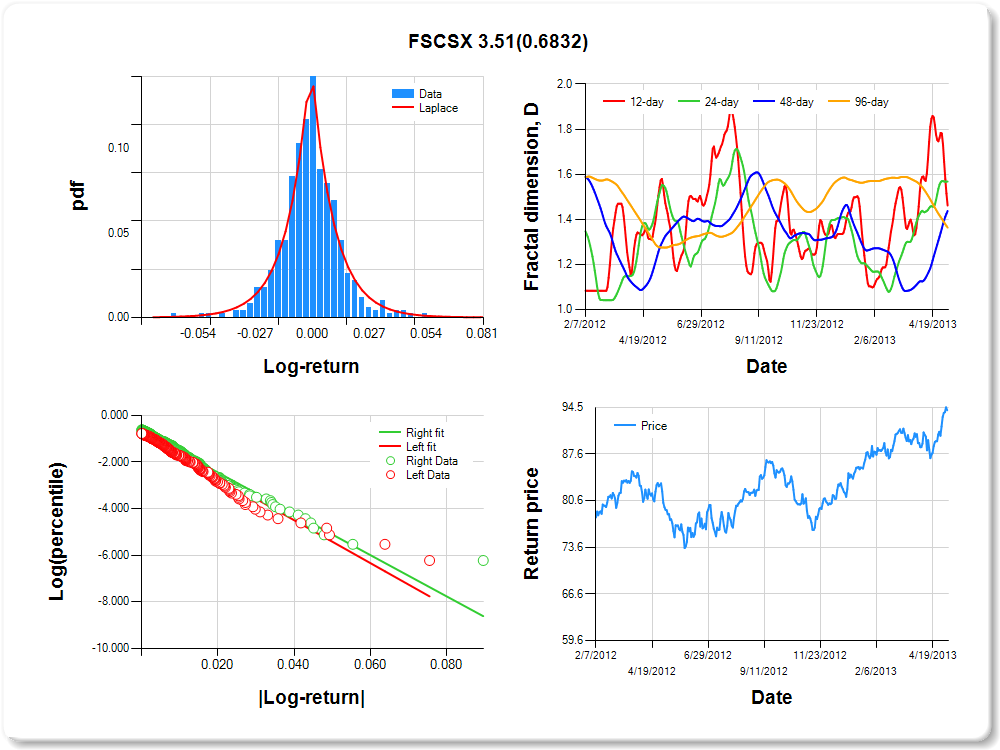

FSCSX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

2.29 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.129 |

0.224 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.817 |

0.094 |

-8.719 |

0.0000 |

|log-return| |

-91.905 |

6.437 |

-14.278 |

0.0000 |

I(right-tail) |

0.132 |

0.127 |

1.045 |

0.2967 |

|log-return|*I(right-tail) |

3.512 |

8.599 |

0.408 |

0.6832 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.539 |

0.432 |

0.563 |

0.637 |

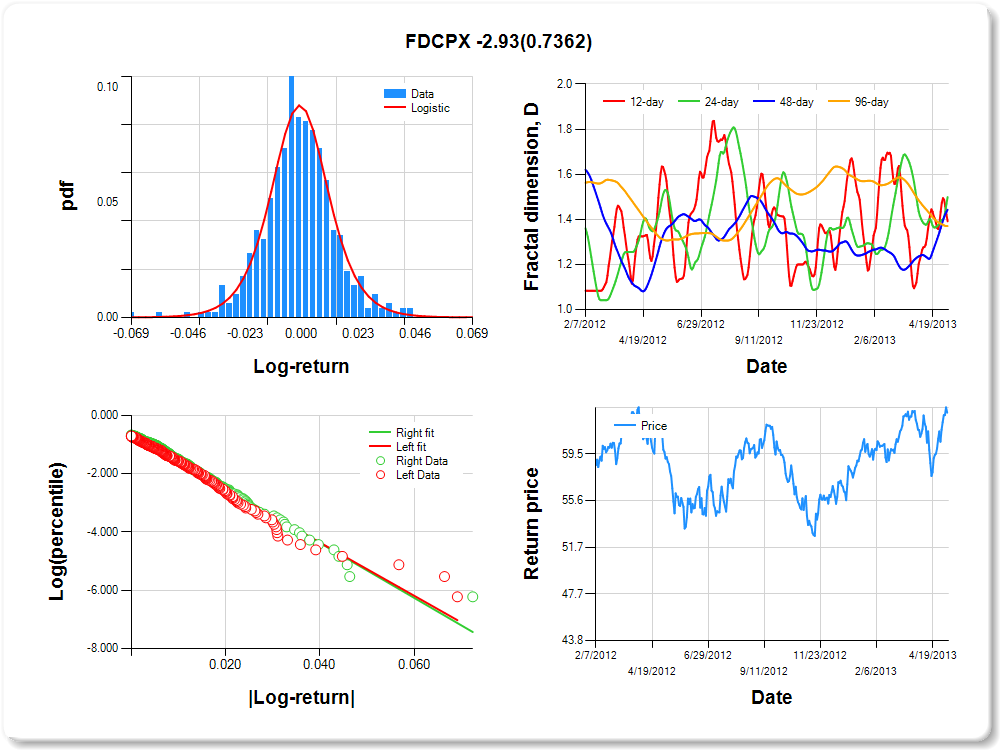

FDCPX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.04 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

2.94 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.028 |

0.186 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.699 |

0.092 |

-7.573 |

0.0000 |

|log-return| |

-91.396 |

6.127 |

-14.918 |

0.0000 |

I(right-tail) |

0.105 |

0.132 |

0.793 |

0.4280 |

|log-return|*I(right-tail) |

-2.932 |

8.699 |

-0.337 |

0.7362 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.608 |

0.501 |

0.557 |

0.629 |

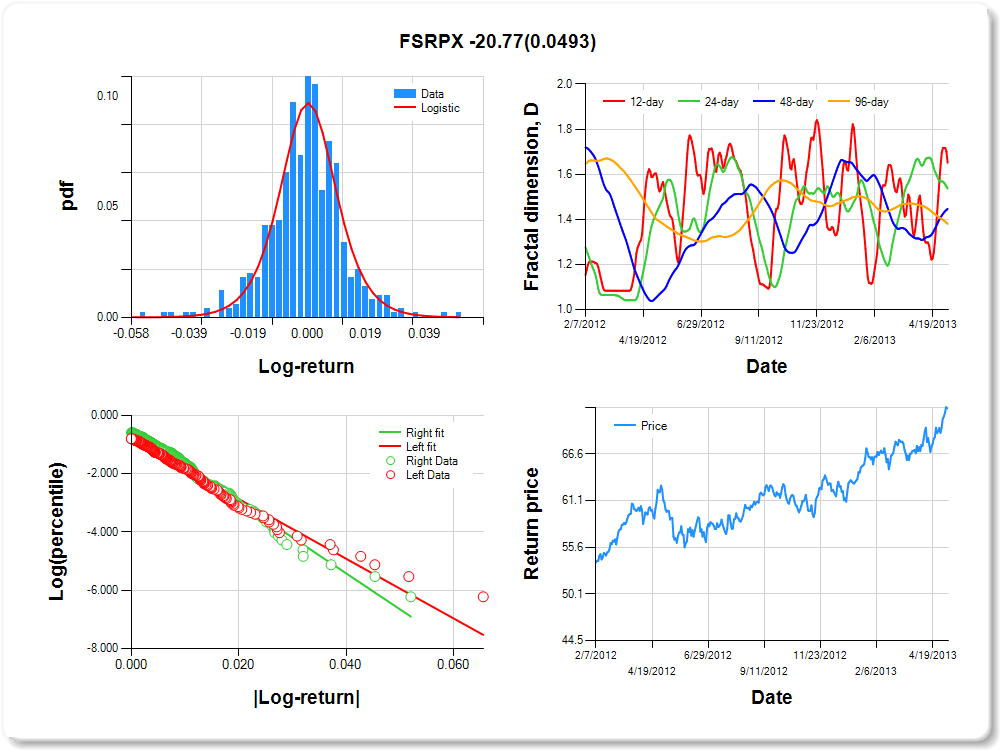

FSRPX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.03 |

1.90 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.238 |

0.177 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.817 |

0.095 |

-8.556 |

0.0000 |

|log-return| |

-102.251 |

7.193 |

-14.214 |

0.0000 |

I(right-tail) |

0.334 |

0.132 |

2.527 |

0.0118 |

|log-return|*I(right-tail) |

-20.774 |

10.543 |

-1.970 |

0.0493 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.349 |

0.463 |

0.553 |

0.620 |

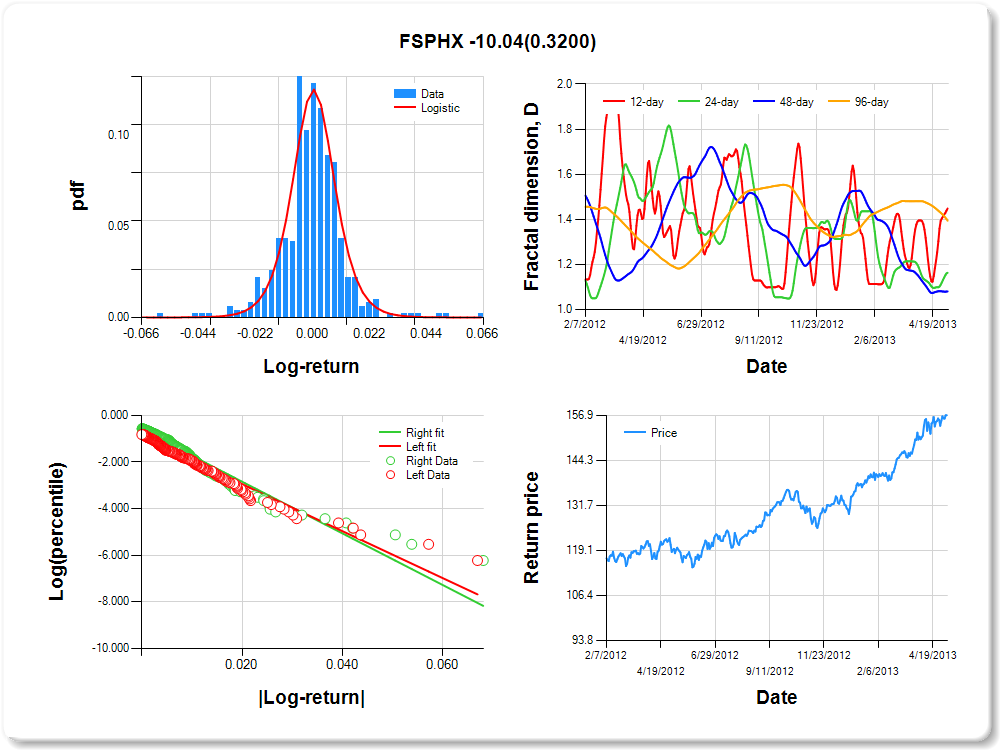

FSPHX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.04 |

-0.02 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.02 |

0.04 |

0.04 |

3.86 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.030 |

0.137 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.937 |

0.092 |

-10.188 |

0.0000 |

|log-return| |

-100.671 |

7.221 |

-13.941 |

0.0000 |

I(right-tail) |

0.307 |

0.125 |

2.469 |

0.0139 |

|log-return|*I(right-tail) |

-10.035 |

10.081 |

-0.995 |

0.3200 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.552 |

0.837 |

0.919 |

0.606 |

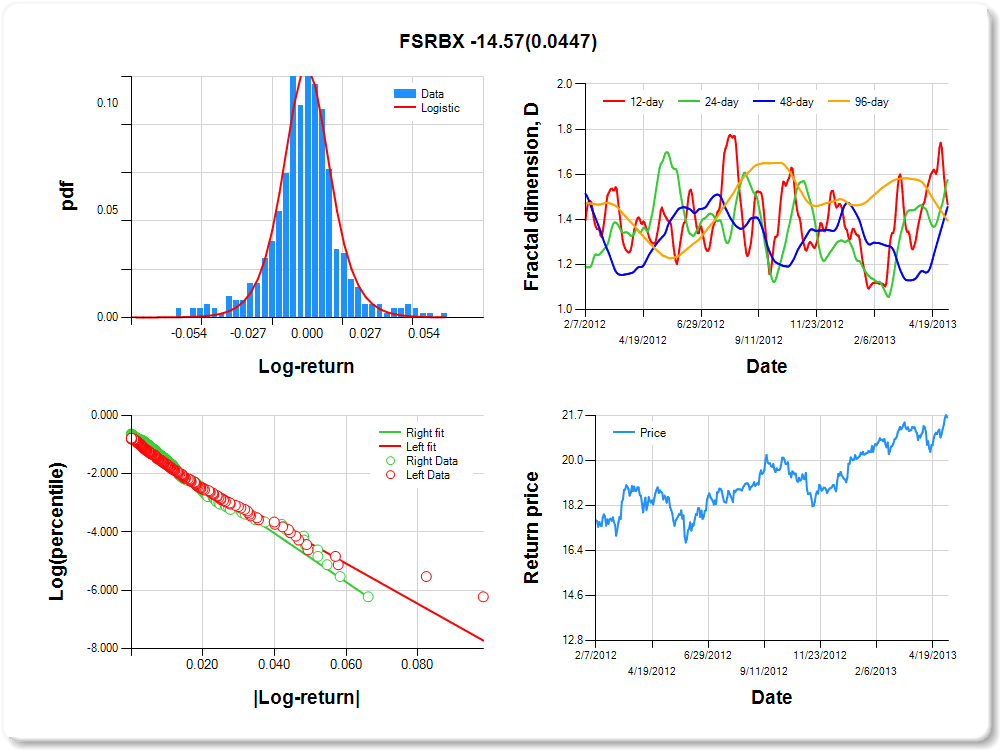

FSRBX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.05 |

0.05 |

3.40 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.361 |

0.146 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.919 |

0.089 |

-10.329 |

0.0000 |

|log-return| |

-68.954 |

4.830 |

-14.276 |

0.0000 |

I(right-tail) |

0.246 |

0.125 |

1.974 |

0.0490 |

|log-return|*I(right-tail) |

-14.574 |

7.241 |

-2.013 |

0.0447 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.533 |

0.425 |

0.545 |

0.605 |

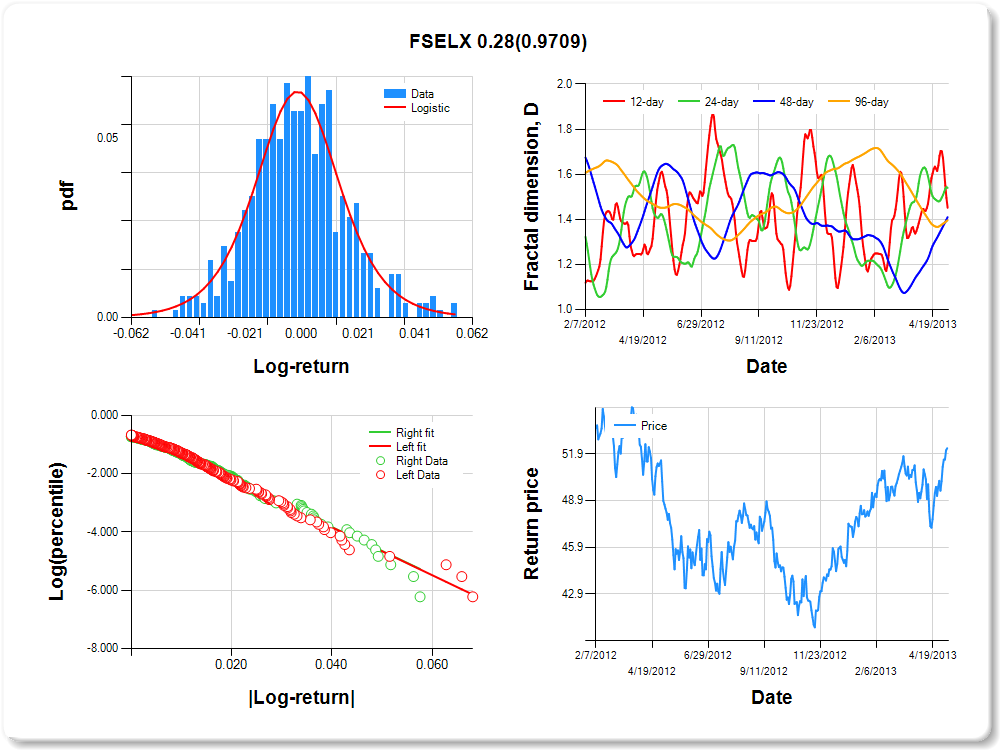

FSELX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.04 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.05 |

3.57 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.132 |

0.273 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.544 |

0.096 |

-5.643 |

0.0000 |

|log-return| |

-82.136 |

5.376 |

-15.280 |

0.0000 |

I(right-tail) |

-0.003 |

0.139 |

-0.025 |

0.9801 |

|log-return|*I(right-tail) |

0.280 |

7.681 |

0.036 |

0.9709 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.549 |

0.460 |

0.590 |

0.604 |

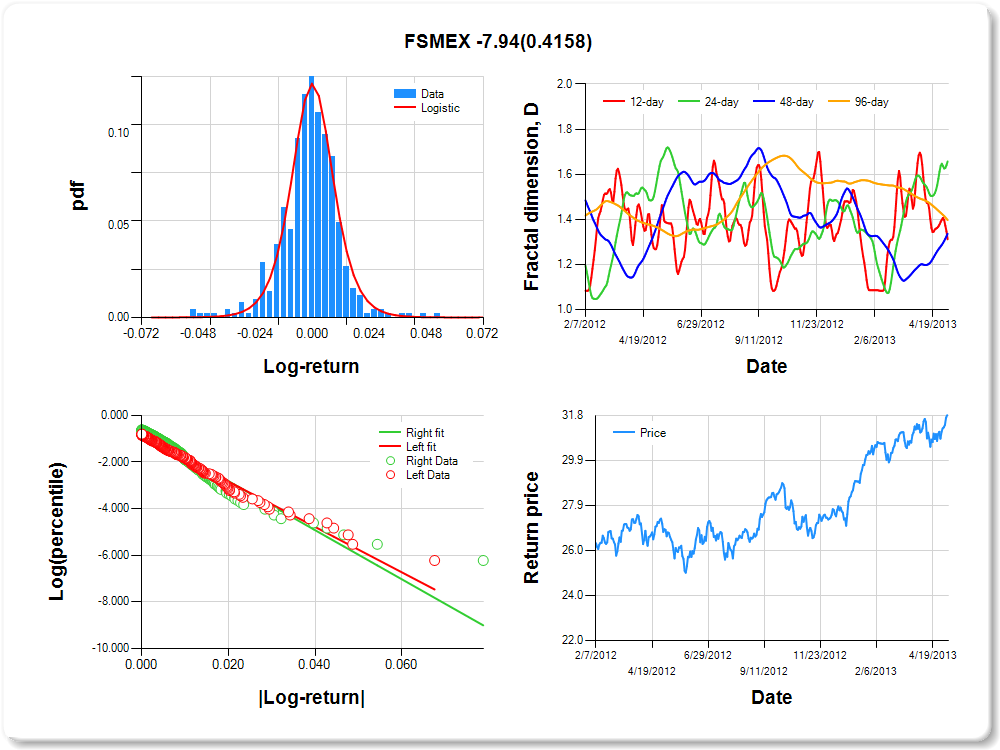

FSMEX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.04 |

2.03 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.098 |

0.135 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.872 |

0.093 |

-9.371 |

0.0000 |

|log-return| |

-97.230 |

6.853 |

-14.189 |

0.0000 |

I(right-tail) |

0.180 |

0.127 |

1.424 |

0.1551 |

|log-return|*I(right-tail) |

-7.941 |

9.749 |

-0.815 |

0.4158 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.688 |

0.343 |

0.664 |

0.603 |

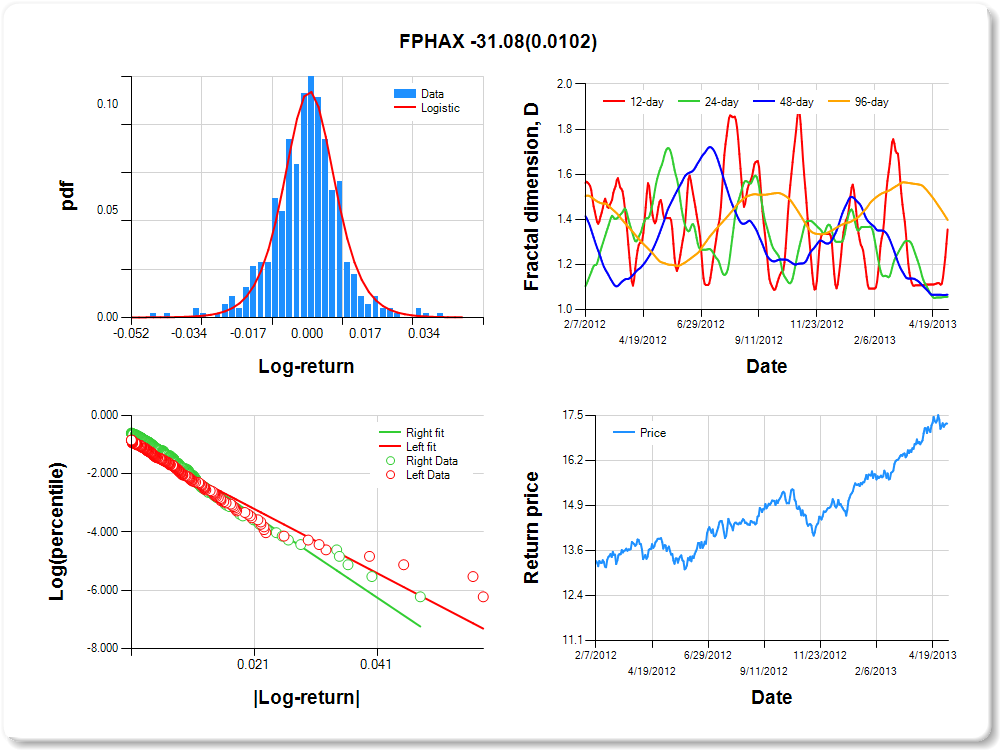

FPHAX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.02 |

0.03 |

0.04 |

2.90 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.221 |

0.162 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.944 |

0.094 |

-10.036 |

0.0000 |

|log-return| |

-110.141 |

8.044 |

-13.692 |

0.0000 |

I(right-tail) |

0.425 |

0.131 |

3.241 |

0.0013 |

|log-return|*I(right-tail) |

-31.077 |

12.049 |

-2.579 |

0.0102 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.645 |

0.943 |

0.934 |

0.603 |

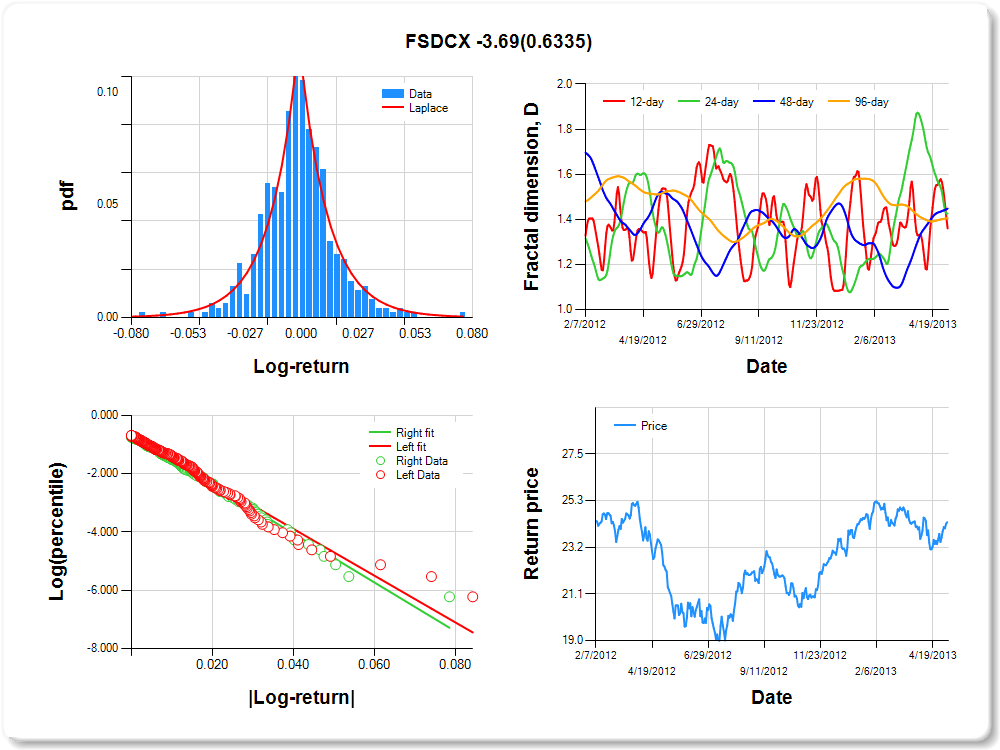

FSDCX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.04 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.05 |

2.25 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.064 |

0.280 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.664 |

0.092 |

-7.206 |

0.0000 |

|log-return| |

-80.225 |

5.326 |

-15.063 |

0.0000 |

I(right-tail) |

-0.010 |

0.132 |

-0.073 |

0.9416 |

|log-return|*I(right-tail) |

-3.693 |

7.740 |

-0.477 |

0.6335 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.640 |

0.574 |

0.552 |

0.595 |

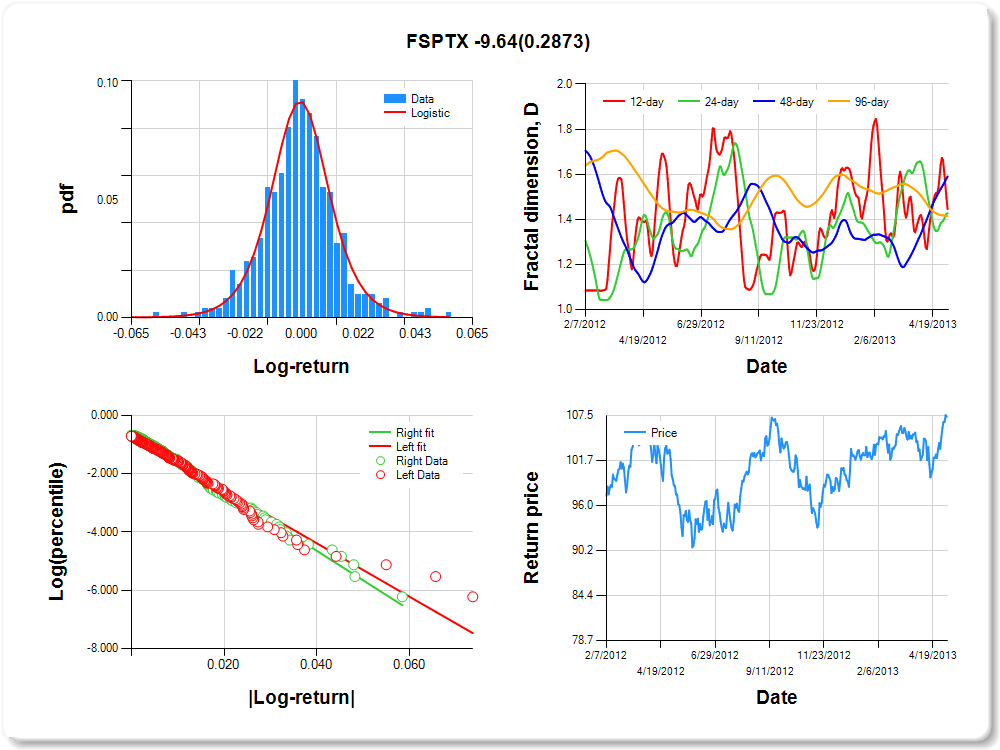

FSPTX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

1.47 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.212 |

0.186 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.719 |

0.092 |

-7.832 |

0.0000 |

|log-return| |

-91.620 |

6.168 |

-14.854 |

0.0000 |

I(right-tail) |

0.128 |

0.132 |

0.970 |

0.3327 |

|log-return|*I(right-tail) |

-9.642 |

9.052 |

-1.065 |

0.2873 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.554 |

0.573 |

0.410 |

0.586 |

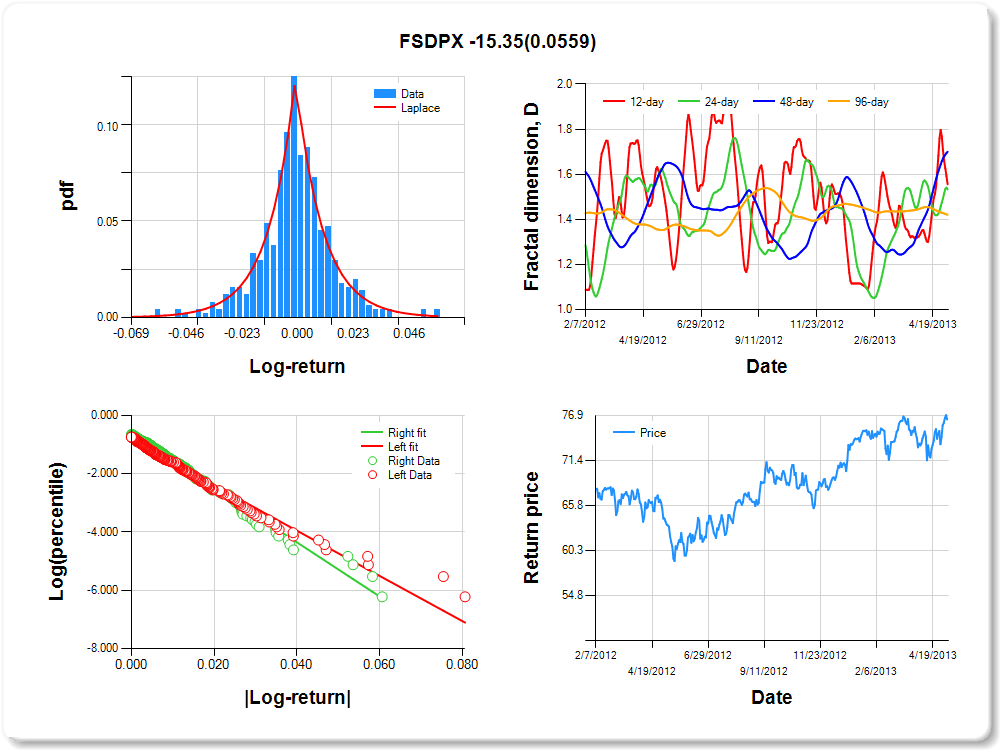

FSDPX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.04 |

0.05 |

3.09 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.250 |

0.272 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.847 |

0.089 |

-9.559 |

0.0000 |

|log-return| |

-77.553 |

5.289 |

-14.662 |

0.0000 |

I(right-tail) |

0.218 |

0.127 |

1.719 |

0.0862 |

|log-return|*I(right-tail) |

-15.350 |

8.009 |

-1.917 |

0.0559 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.444 |

0.467 |

0.300 |

0.580 |

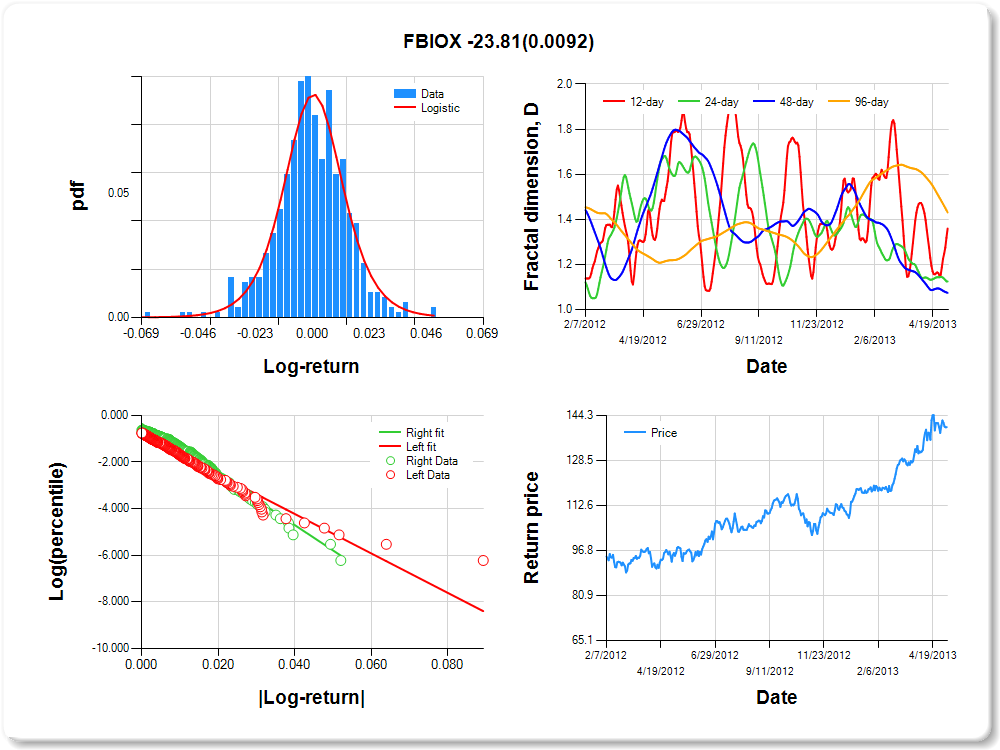

FBIOX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.04 |

2.07 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.494 |

0.191 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.846 |

0.090 |

-9.362 |

0.0000 |

|log-return| |

-84.575 |

5.871 |

-14.404 |

0.0000 |

I(right-tail) |

0.475 |

0.136 |

3.499 |

0.0005 |

|log-return|*I(right-tail) |

-23.814 |

9.112 |

-2.614 |

0.0092 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.641 |

0.875 |

0.926 |

0.569 |

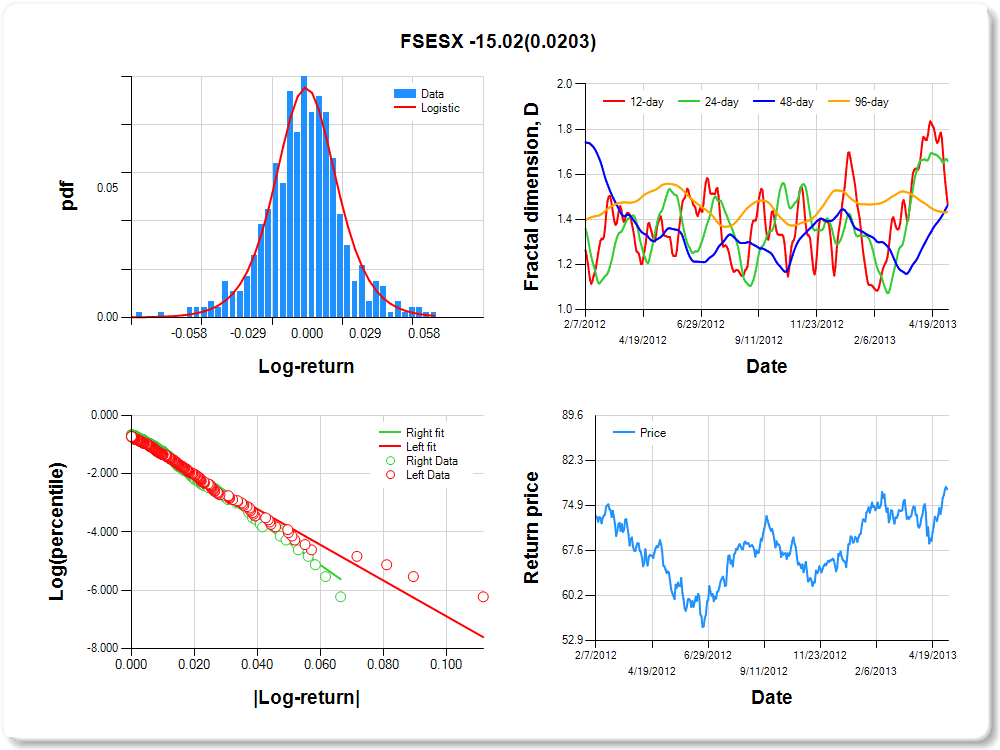

FSESX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.08 |

-0.06 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.06 |

3.07 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.455 |

0.194 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.756 |

0.091 |

-8.295 |

0.0000 |

|log-return| |

-61.328 |

4.144 |

-14.799 |

0.0000 |

I(right-tail) |

0.213 |

0.132 |

1.621 |

0.1056 |

|log-return|*I(right-tail) |

-15.022 |

6.453 |

-2.328 |

0.0203 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.532 |

0.341 |

0.537 |

0.566 |

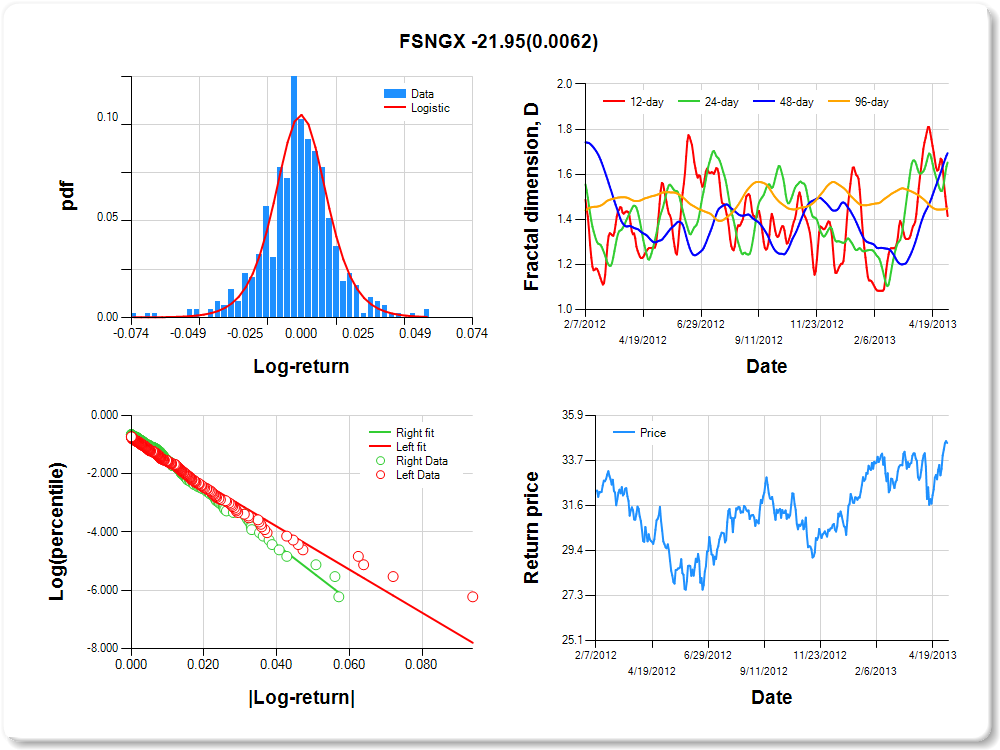

FSNGX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.04 |

4.13 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.440 |

0.169 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.836 |

0.089 |

-9.448 |

0.0000 |

|log-return| |

-73.972 |

5.045 |

-14.662 |

0.0000 |

I(right-tail) |

0.256 |

0.128 |

1.997 |

0.0463 |

|log-return|*I(right-tail) |

-21.953 |

7.993 |

-2.746 |

0.0062 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.585 |

0.348 |

0.306 |

0.551 |

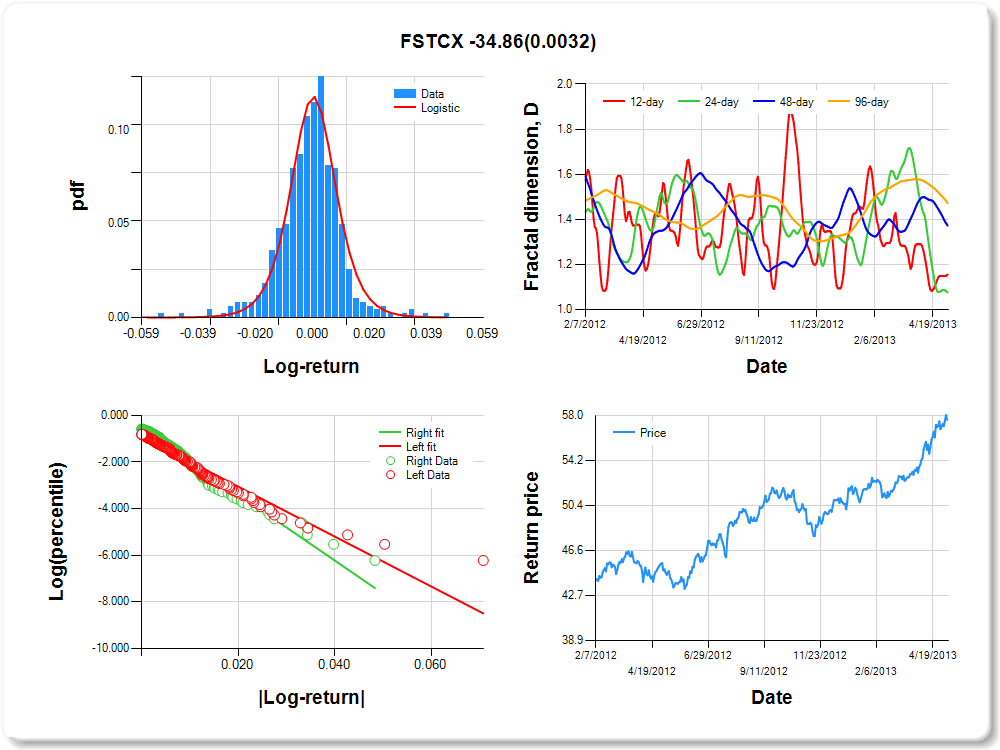

FSTCX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.03 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.01 |

0.03 |

0.04 |

2.27 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.365 |

0.145 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.908 |

0.093 |

-9.773 |

0.0000 |

|log-return| |

-106.837 |

7.683 |

-13.905 |

0.0000 |

I(right-tail) |

0.375 |

0.129 |

2.919 |

0.0037 |

|log-return|*I(right-tail) |

-34.859 |

11.776 |

-2.960 |

0.0032 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.845 |

0.924 |

0.628 |

0.528 |

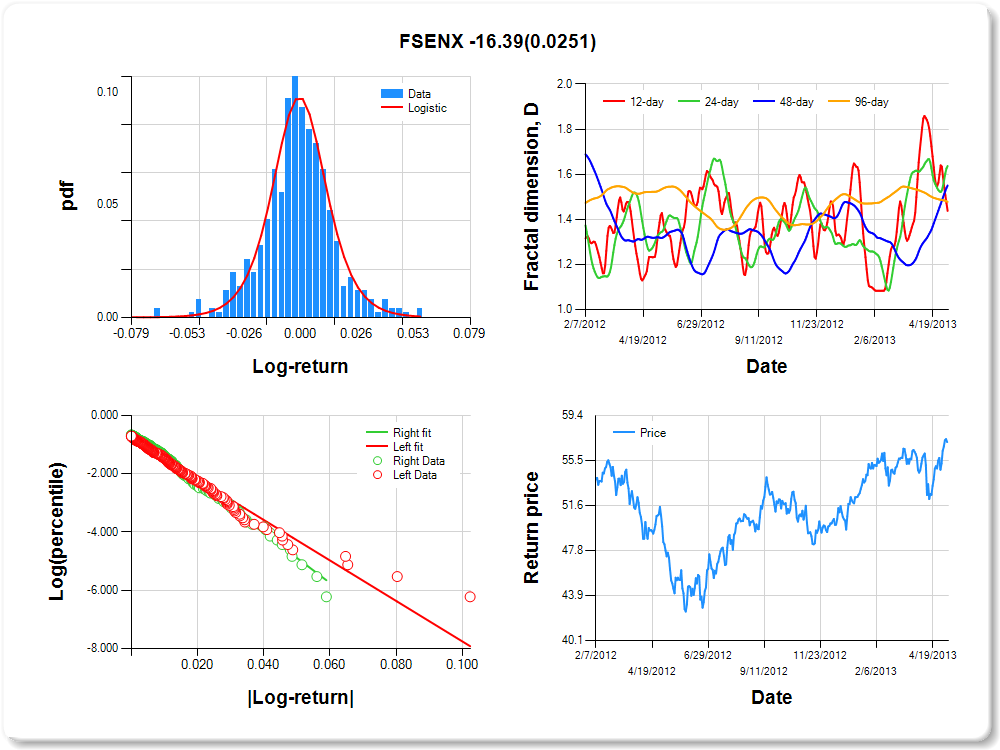

FSENX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.05 |

3.77 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.482 |

0.176 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.801 |

0.088 |

-9.114 |

0.0000 |

|log-return| |

-69.485 |

4.681 |

-14.845 |

0.0000 |

I(right-tail) |

0.215 |

0.129 |

1.669 |

0.0958 |

|log-return|*I(right-tail) |

-16.395 |

7.296 |

-2.247 |

0.0251 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.562 |

0.363 |

0.450 |

0.522 |

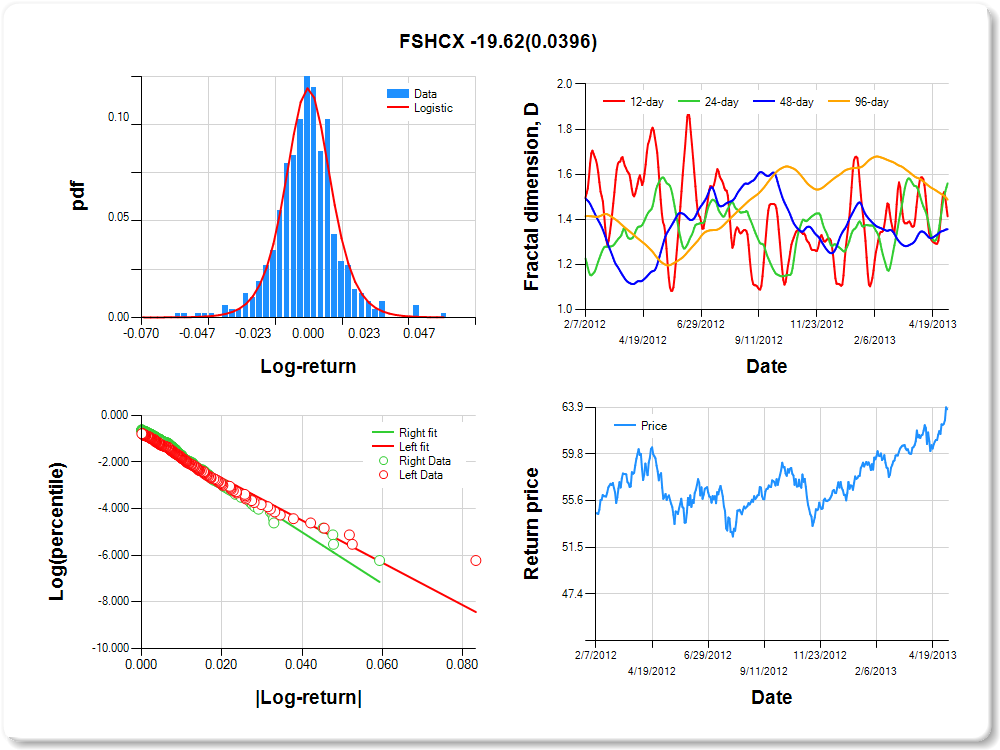

FSHCX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.05 |

3.51 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.315 |

0.149 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.872 |

0.092 |

-9.496 |

0.0000 |

|log-return| |

-90.609 |

6.396 |

-14.168 |

0.0000 |

I(right-tail) |

0.280 |

0.128 |

2.184 |

0.0294 |

|log-return|*I(right-tail) |

-19.618 |

9.510 |

-2.063 |

0.0396 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.586 |

0.440 |

0.644 |

0.512 |

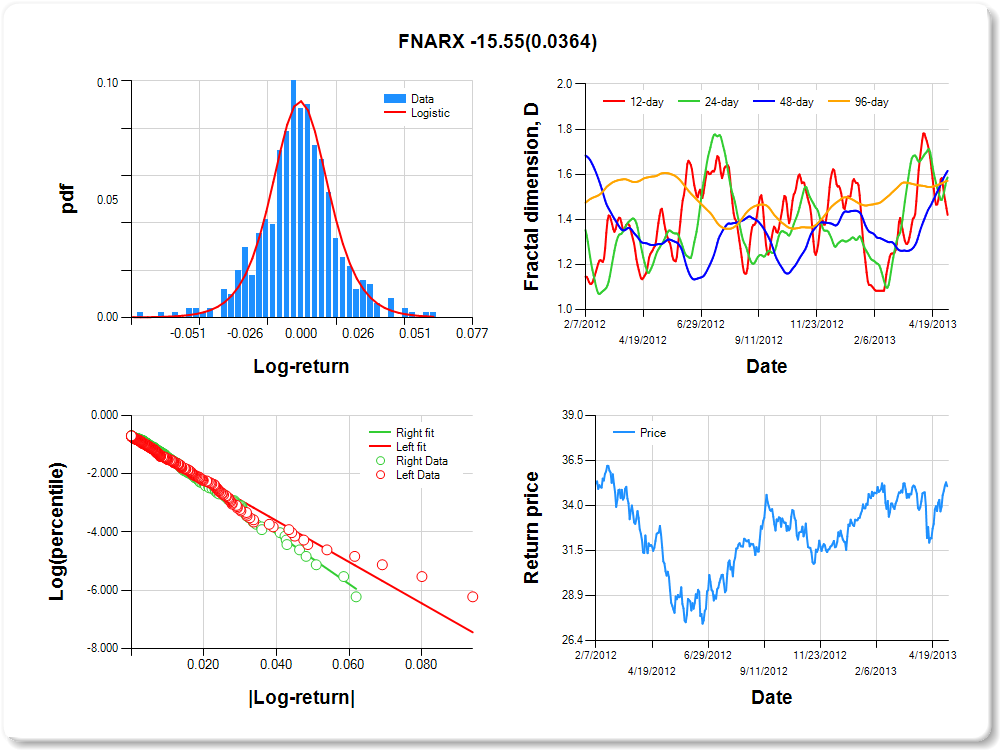

FNARX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.04 |

0.05 |

2.81 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.368 |

0.186 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.770 |

0.089 |

-8.705 |

0.0000 |

|log-return| |

-70.778 |

4.733 |

-14.954 |

0.0000 |

I(right-tail) |

0.183 |

0.131 |

1.397 |

0.1630 |

|log-return|*I(right-tail) |

-15.548 |

7.411 |

-2.098 |

0.0364 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.580 |

0.414 |

0.384 |

0.429 |