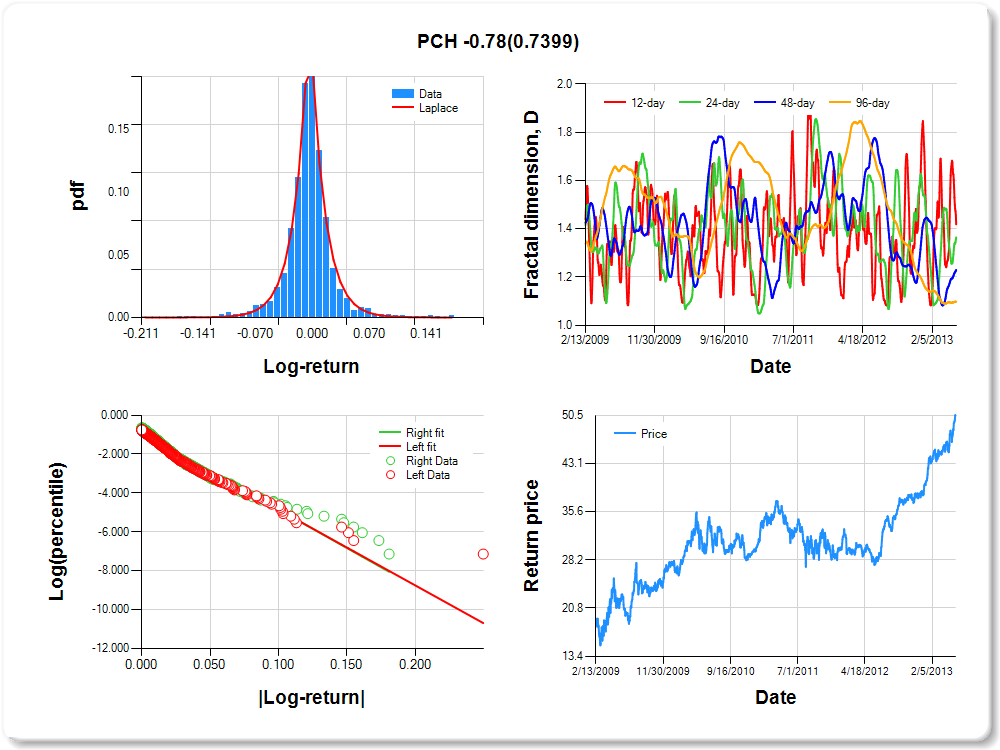

PCH

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.11 |

-0.09 |

-0.04 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.05 |

0.10 |

0.14 |

0.49 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.279 |

0.140 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.959 |

0.053 |

-17.988 |

0.0000 |

|log-return| |

-38.945 |

1.679 |

-23.199 |

0.0000 |

I(right-tail) |

0.093 |

0.074 |

1.268 |

0.2050 |

|log-return|*I(right-tail) |

-0.777 |

2.340 |

-0.332 |

0.7399 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.581 |

0.635 |

0.770 |

0.902 |

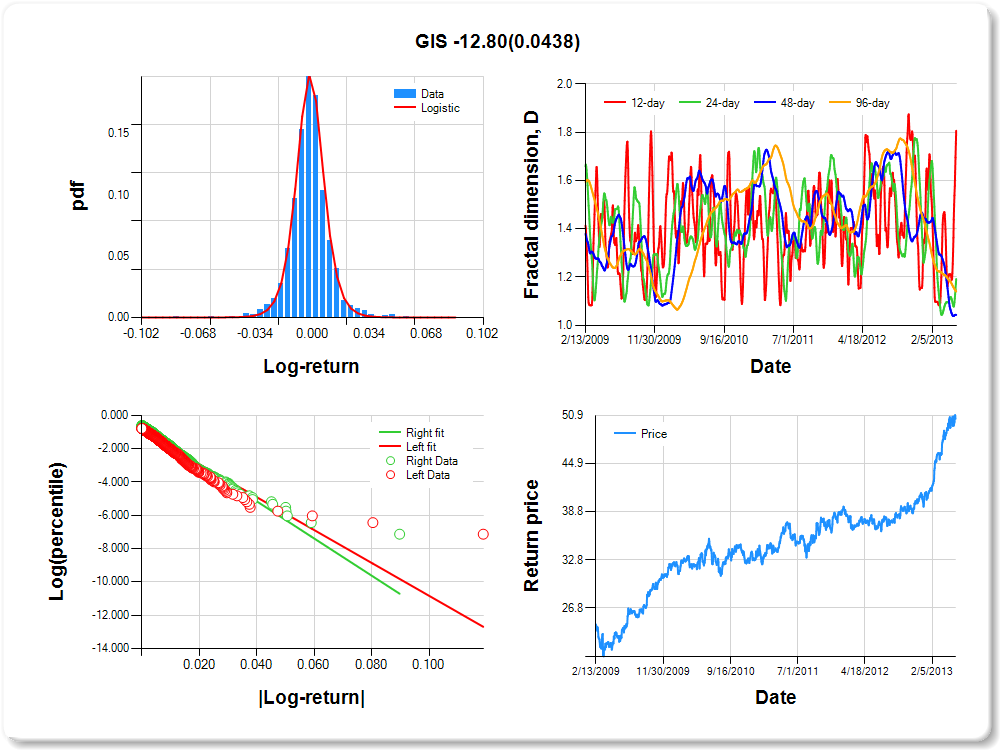

GIS

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.03 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.05 |

1.31 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.248 |

0.086 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.954 |

0.057 |

-16.825 |

0.0000 |

|log-return| |

-98.678 |

4.508 |

-21.890 |

0.0000 |

I(right-tail) |

0.266 |

0.078 |

3.407 |

0.0007 |

|log-return|*I(right-tail) |

-12.804 |

6.344 |

-2.018 |

0.0438 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.193 |

0.808 |

0.957 |

0.860 |

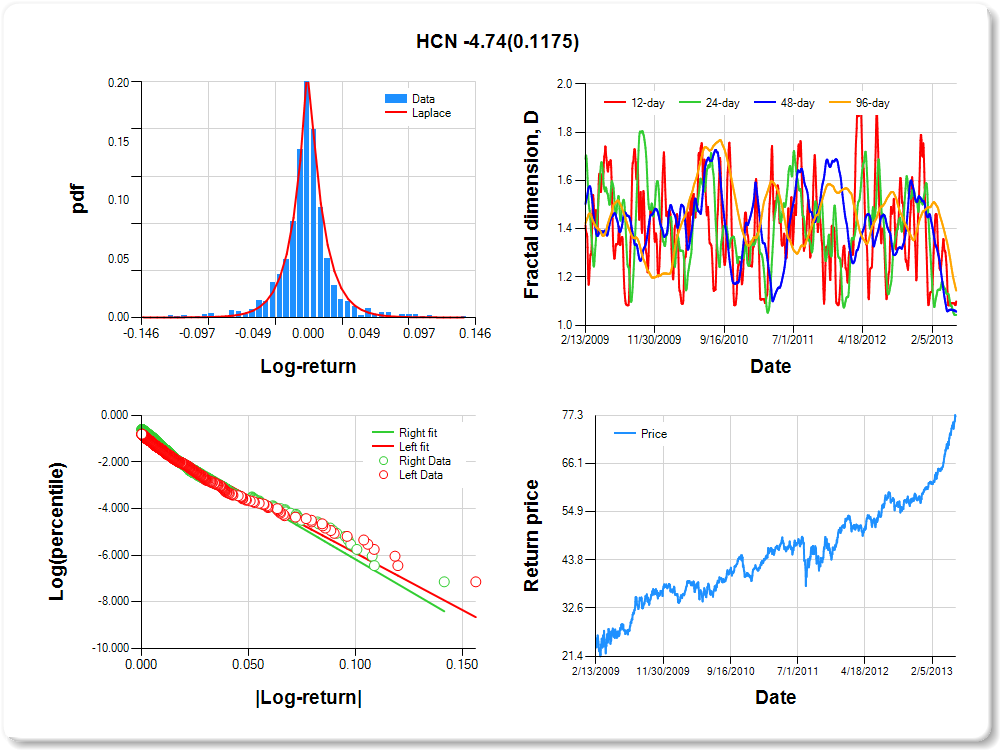

HCN

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.10 |

-0.08 |

-0.04 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.08 |

0.10 |

1.48 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.113 |

0.151 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.013 |

0.055 |

-18.544 |

0.0000 |

|log-return| |

-48.885 |

2.146 |

-22.777 |

0.0000 |

I(right-tail) |

0.202 |

0.074 |

2.736 |

0.0063 |

|log-return|*I(right-tail) |

-4.745 |

3.029 |

-1.566 |

0.1175 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.901 |

0.957 |

0.944 |

0.856 |

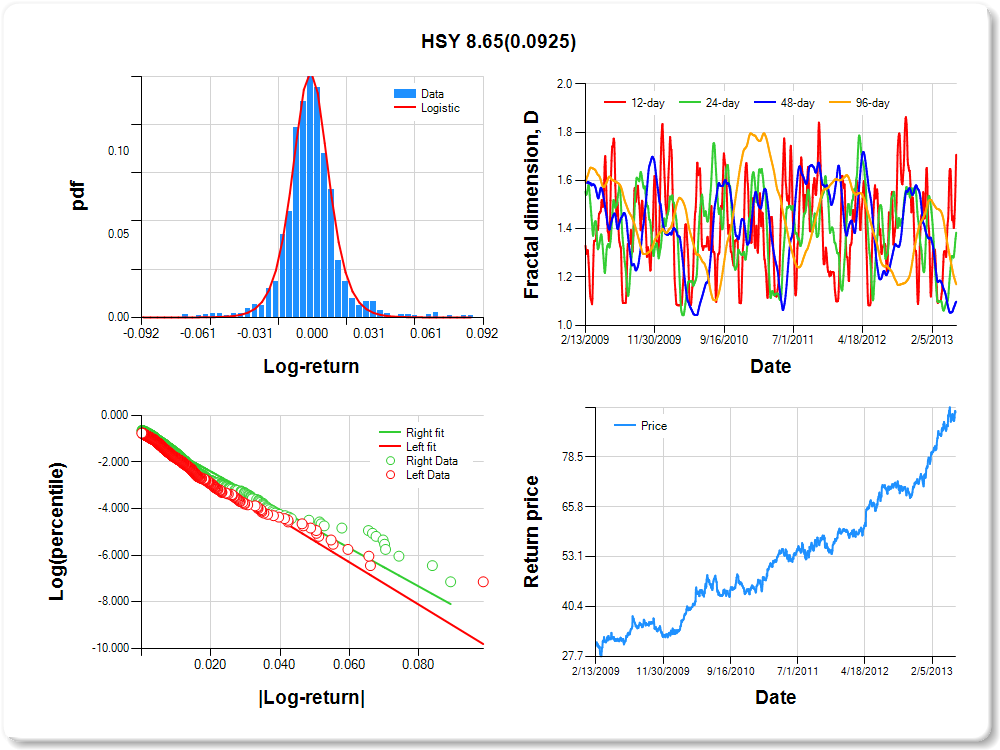

HSY

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.05 |

0.07 |

0.87 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.100 |

0.116 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.862 |

0.057 |

-15.250 |

0.0000 |

|log-return| |

-90.609 |

3.899 |

-23.238 |

0.0000 |

I(right-tail) |

0.087 |

0.077 |

1.124 |

0.2612 |

|log-return|*I(right-tail) |

8.648 |

5.136 |

1.684 |

0.0925 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.293 |

0.616 |

0.902 |

0.830 |

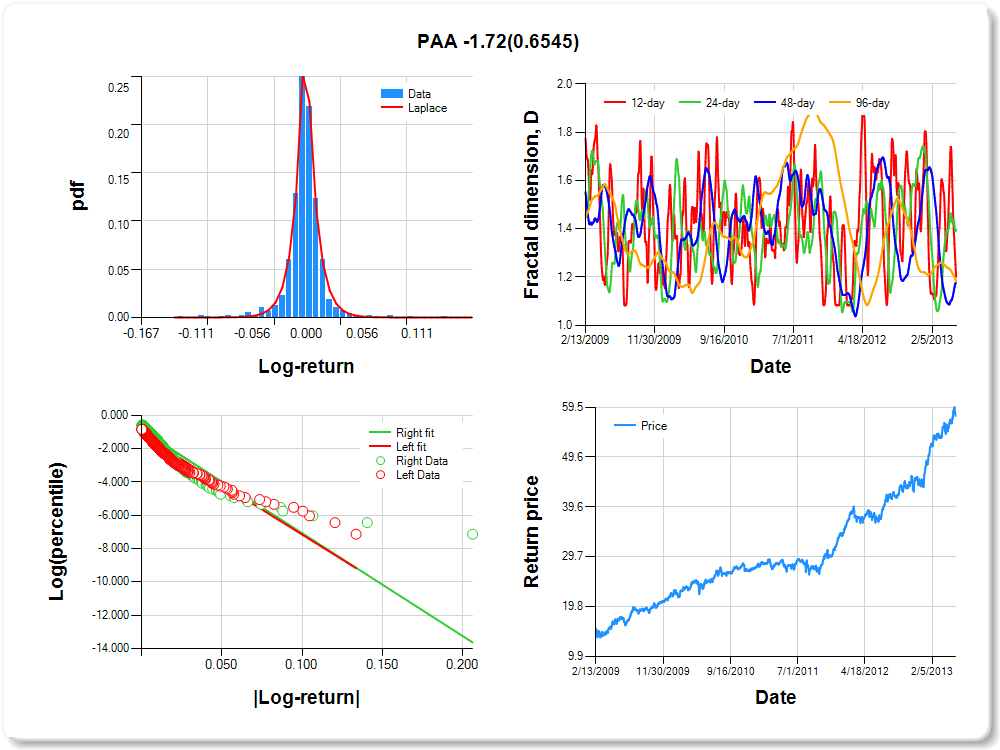

PAA

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.08 |

-0.06 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.05 |

0.07 |

0.86 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.349 |

0.099 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.157 |

0.053 |

-21.700 |

0.0000 |

|log-return| |

-59.975 |

2.767 |

-21.672 |

0.0000 |

I(right-tail) |

0.257 |

0.072 |

3.581 |

0.0004 |

|log-return|*I(right-tail) |

-1.715 |

3.832 |

-0.448 |

0.6545 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.799 |

0.605 |

0.818 |

0.819 |

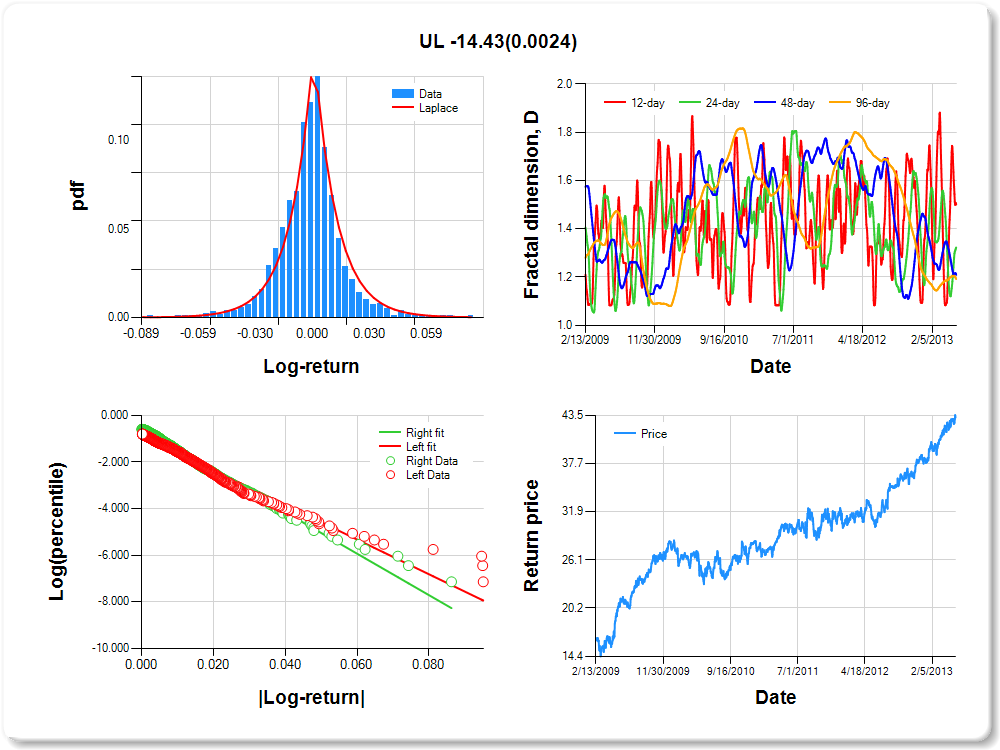

UL

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.04 |

0.05 |

-0.02 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.130 |

0.225 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.861 |

0.059 |

-14.639 |

0.0000 |

|log-return| |

-74.293 |

3.249 |

-22.866 |

0.0000 |

I(right-tail) |

0.263 |

0.080 |

3.277 |

0.0011 |

|log-return|*I(right-tail) |

-14.426 |

4.747 |

-3.039 |

0.0024 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.499 |

0.678 |

0.791 |

0.809 |

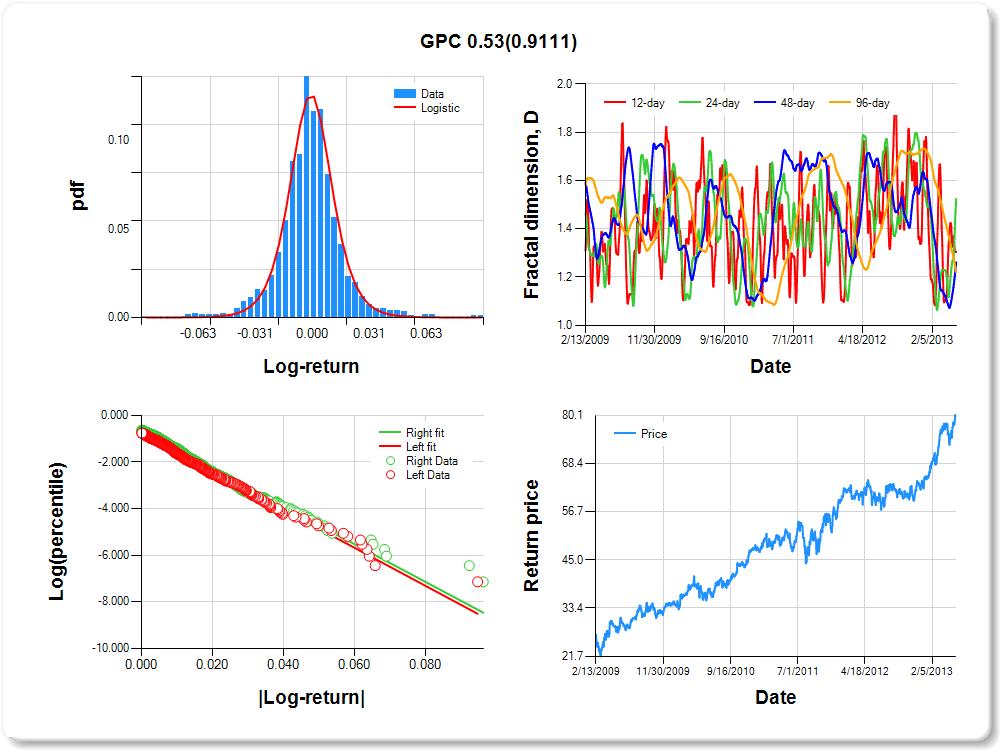

GPC

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.06 |

1.04 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.005 |

0.136 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.787 |

0.058 |

-13.480 |

0.0000 |

|log-return| |

-81.388 |

3.453 |

-23.571 |

0.0000 |

I(right-tail) |

0.126 |

0.080 |

1.570 |

0.1166 |

|log-return|*I(right-tail) |

0.528 |

4.729 |

0.112 |

0.9111 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.696 |

0.476 |

0.739 |

0.781 |

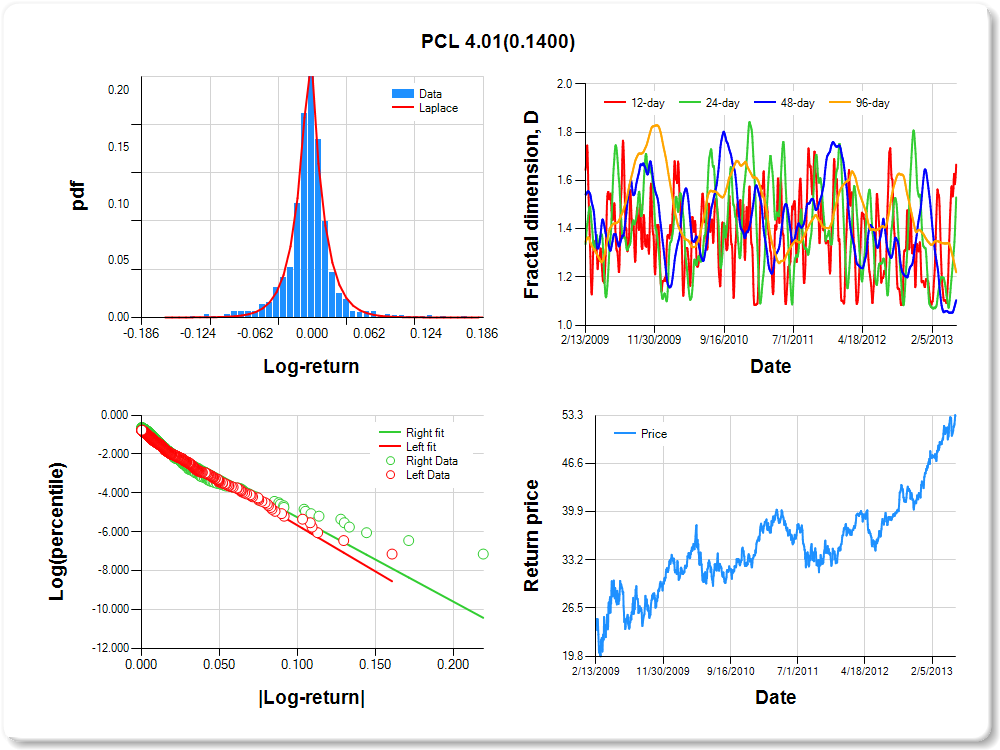

PCL

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.10 |

-0.08 |

-0.04 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.09 |

0.12 |

1.50 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.257 |

0.133 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.929 |

0.055 |

-17.010 |

0.0000 |

|log-return| |

-47.399 |

2.024 |

-23.418 |

0.0000 |

I(right-tail) |

0.011 |

0.073 |

0.154 |

0.8773 |

|log-return|*I(right-tail) |

4.008 |

2.714 |

1.477 |

0.1400 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.334 |

0.470 |

0.896 |

0.780 |

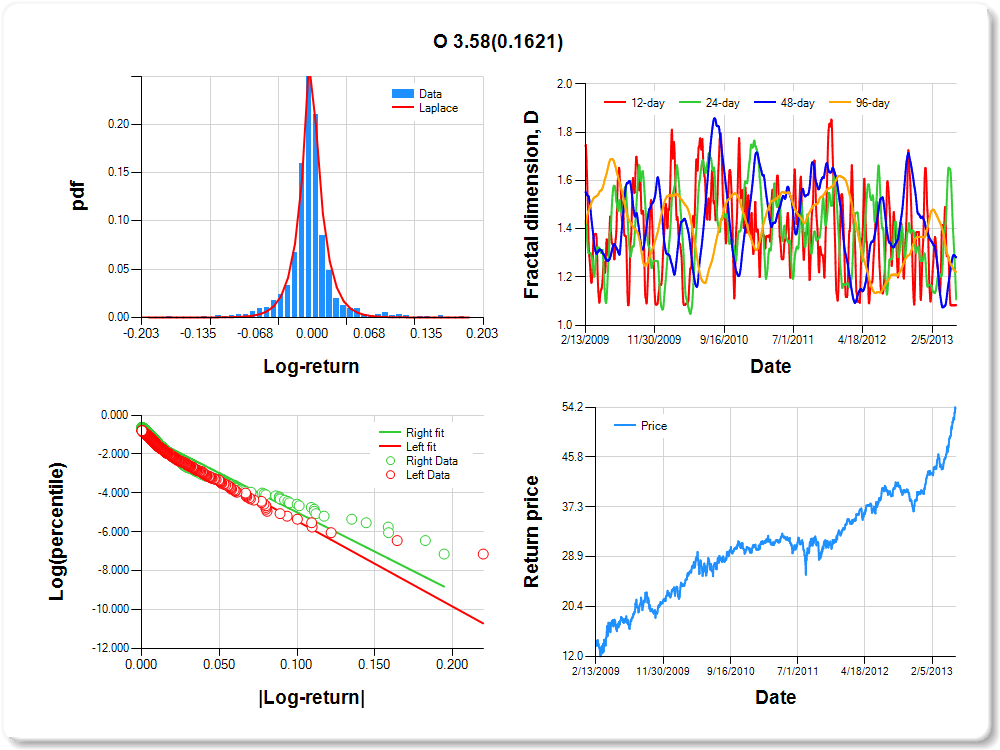

O

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.10 |

-0.08 |

-0.04 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.10 |

0.12 |

0.66 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.122 |

0.111 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.042 |

0.053 |

-19.564 |

0.0000 |

|log-return| |

-43.947 |

1.941 |

-22.637 |

0.0000 |

I(right-tail) |

0.087 |

0.071 |

1.220 |

0.2225 |

|log-return|*I(right-tail) |

3.579 |

2.559 |

1.399 |

0.1621 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.917 |

0.893 |

0.719 |

0.779 |

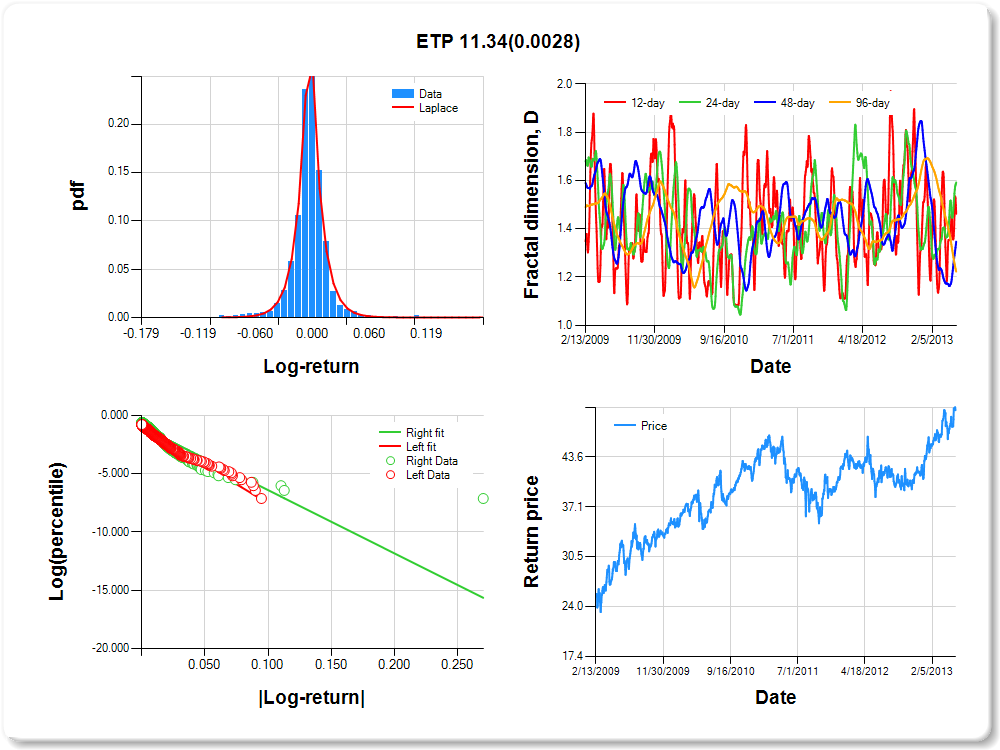

ETP

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.06 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.05 |

0.06 |

1.02 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.817 |

0.103 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.989 |

0.055 |

-18.002 |

0.0000 |

|log-return| |

-65.602 |

2.874 |

-22.829 |

0.0000 |

I(right-tail) |

-0.001 |

0.073 |

-0.015 |

0.9877 |

|log-return|*I(right-tail) |

11.338 |

3.791 |

2.990 |

0.0028 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.538 |

0.408 |

0.653 |

0.778 |

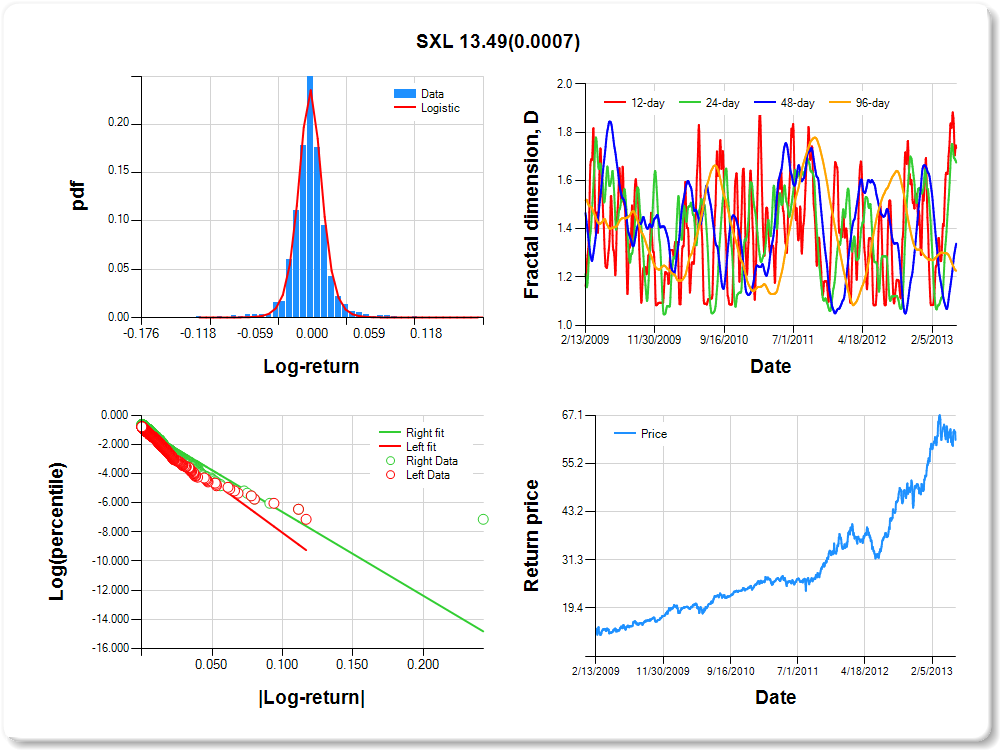

SXL

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.05 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.08 |

1.57 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.588 |

0.074 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.961 |

0.056 |

-17.302 |

0.0000 |

|log-return| |

-70.886 |

3.131 |

-22.639 |

0.0000 |

I(right-tail) |

0.068 |

0.074 |

0.917 |

0.3592 |

|log-return|*I(right-tail) |

13.494 |

3.987 |

3.384 |

0.0007 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.265 |

0.325 |

0.661 |

0.774 |

DUK

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.05 |

0.36 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.093 |

0.079 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.991 |

0.055 |

-18.159 |

0.0000 |

|log-return| |

-90.083 |

4.013 |

-22.449 |

0.0000 |

I(right-tail) |

0.156 |

0.076 |

2.055 |

0.0401 |

|log-return|*I(right-tail) |

-0.651 |

5.568 |

-0.117 |

0.9069 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.678 |

0.762 |

0.939 |

0.771 |

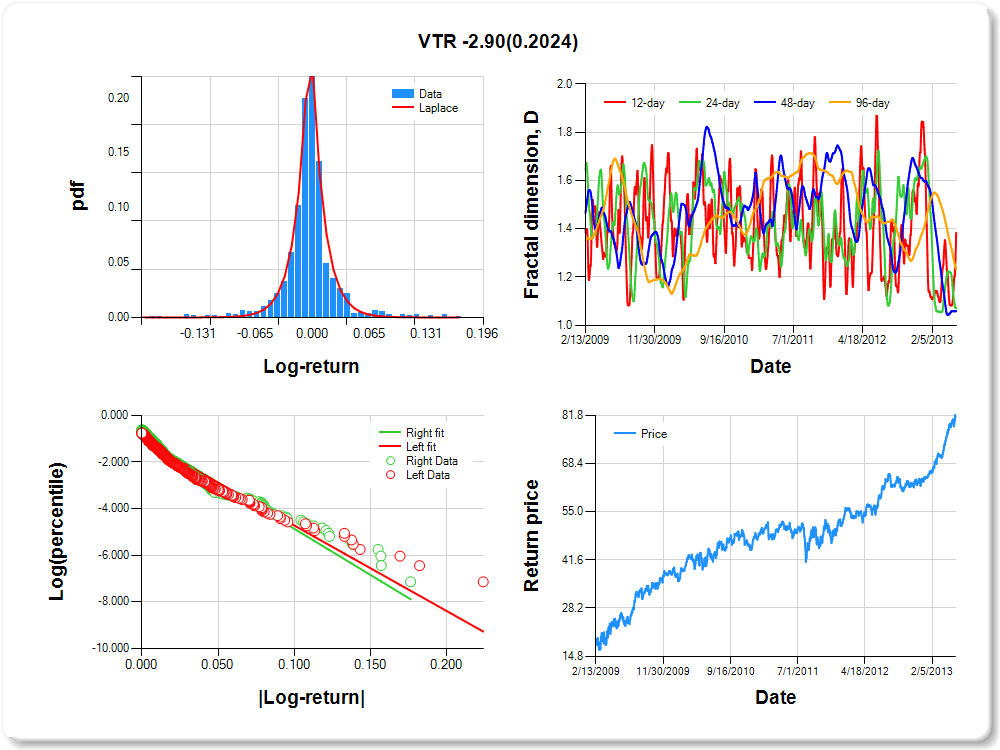

VTR

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.13 |

-0.09 |

-0.04 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.11 |

0.13 |

1.16 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.214 |

0.124 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.051 |

0.052 |

-20.370 |

0.0000 |

|log-return| |

-36.711 |

1.599 |

-22.954 |

0.0000 |

I(right-tail) |

0.147 |

0.071 |

2.068 |

0.0389 |

|log-return|*I(right-tail) |

-2.897 |

2.272 |

-1.275 |

0.2024 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.616 |

0.929 |

0.942 |

0.768 |

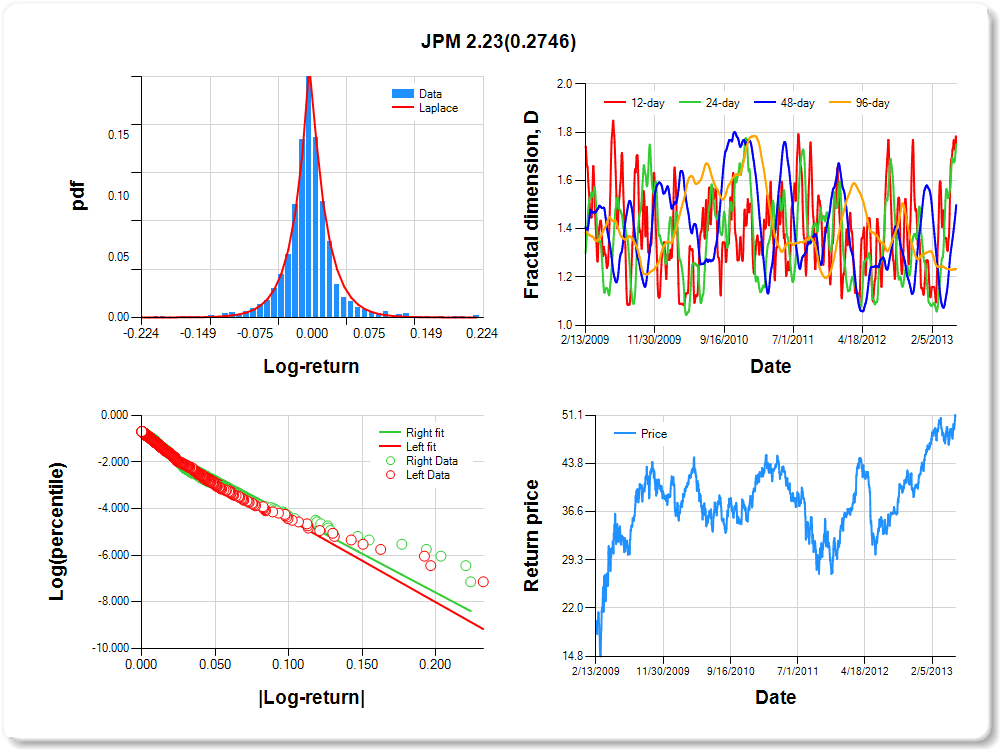

JPM

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.13 |

-0.10 |

-0.05 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.05 |

0.13 |

0.16 |

1.27 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.041 |

0.157 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.898 |

0.052 |

-17.307 |

0.0000 |

|log-return| |

-35.557 |

1.484 |

-23.962 |

0.0000 |

I(right-tail) |

-0.036 |

0.073 |

-0.489 |

0.6249 |

|log-return|*I(right-tail) |

2.235 |

2.045 |

1.093 |

0.2746 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.254 |

0.249 |

0.501 |

0.766 |

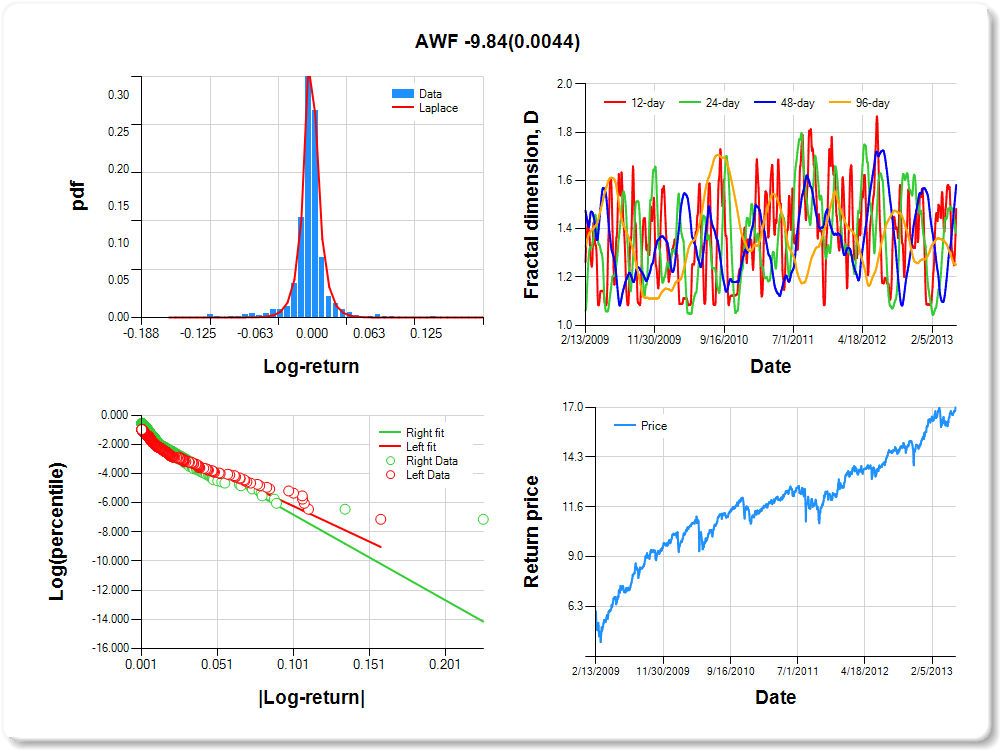

AWF

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.10 |

-0.07 |

-0.03 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.03 |

0.05 |

0.08 |

-0.05 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.282 |

0.072 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.338 |

0.056 |

-24.034 |

0.0000 |

|log-return| |

-48.721 |

2.410 |

-20.217 |

0.0000 |

I(right-tail) |

0.399 |

0.072 |

5.576 |

0.0000 |

|log-return|*I(right-tail) |

-9.843 |

3.447 |

-2.855 |

0.0044 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.517 |

0.617 |

0.418 |

0.747 |

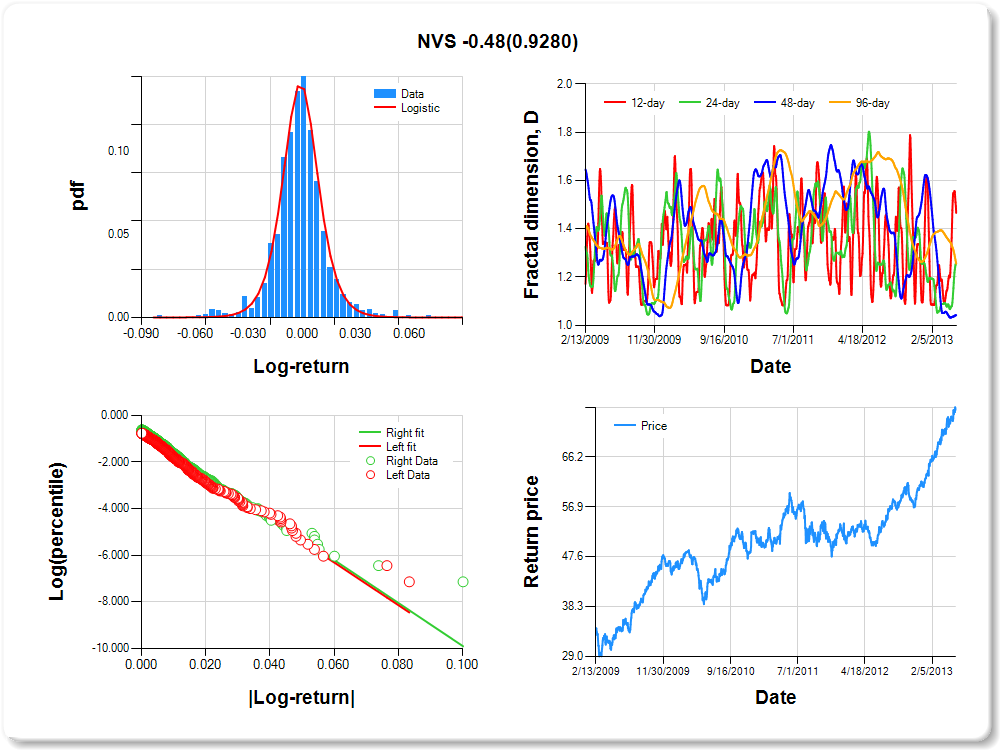

NVS

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.06 |

0.62 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.143 |

0.122 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.820 |

0.058 |

-14.142 |

0.0000 |

|log-return| |

-91.325 |

3.910 |

-23.358 |

0.0000 |

I(right-tail) |

0.132 |

0.079 |

1.671 |

0.0951 |

|log-return|*I(right-tail) |

-0.484 |

5.356 |

-0.090 |

0.9280 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.534 |

0.742 |

0.958 |

0.745 |

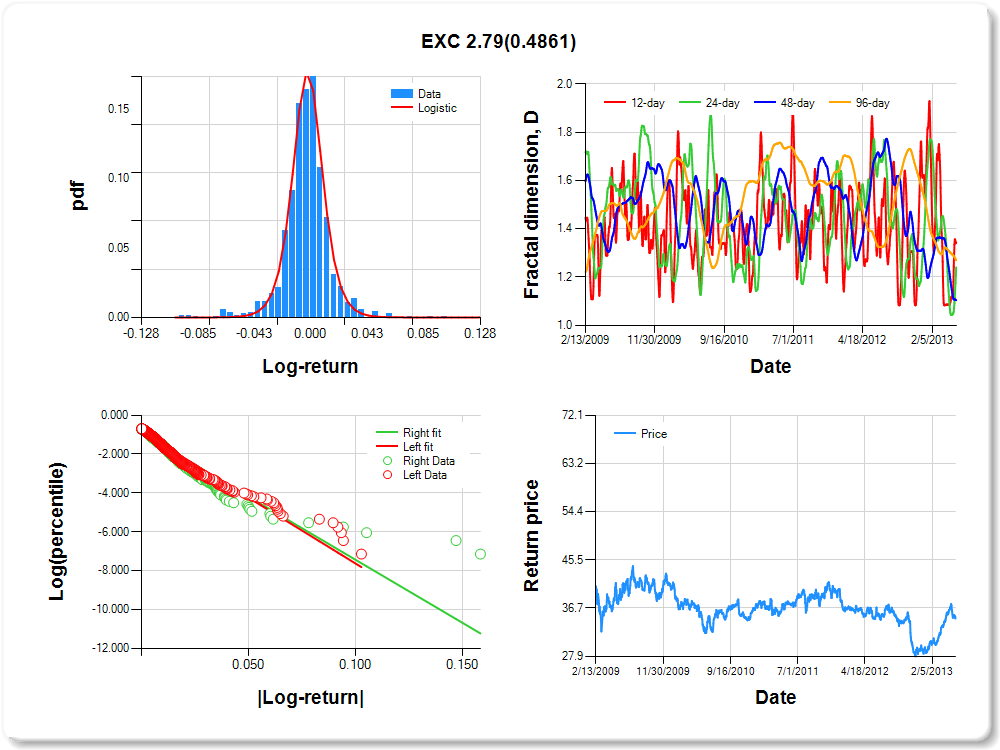

EXC

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.08 |

-0.06 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.04 |

0.06 |

0.00 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.365 |

0.097 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.849 |

0.053 |

-16.005 |

0.0000 |

|log-return| |

-67.621 |

2.818 |

-23.993 |

0.0000 |

I(right-tail) |

-0.089 |

0.075 |

-1.193 |

0.2331 |

|log-return|*I(right-tail) |

2.793 |

4.008 |

0.697 |

0.4861 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.658 |

0.760 |

0.896 |

0.730 |

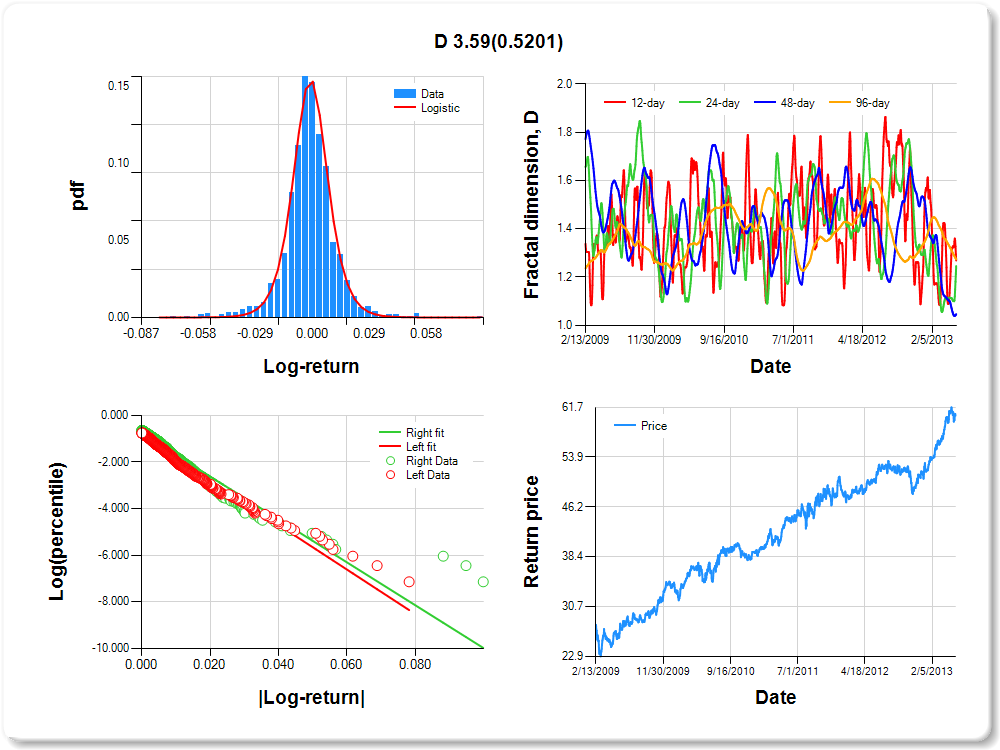

D

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

2.18 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.194 |

0.111 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.869 |

0.056 |

-15.549 |

0.0000 |

|log-return| |

-95.505 |

4.072 |

-23.457 |

0.0000 |

I(right-tail) |

0.093 |

0.077 |

1.201 |

0.2299 |

|log-return|*I(right-tail) |

3.587 |

5.575 |

0.643 |

0.5201 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.731 |

0.754 |

0.954 |

0.727 |

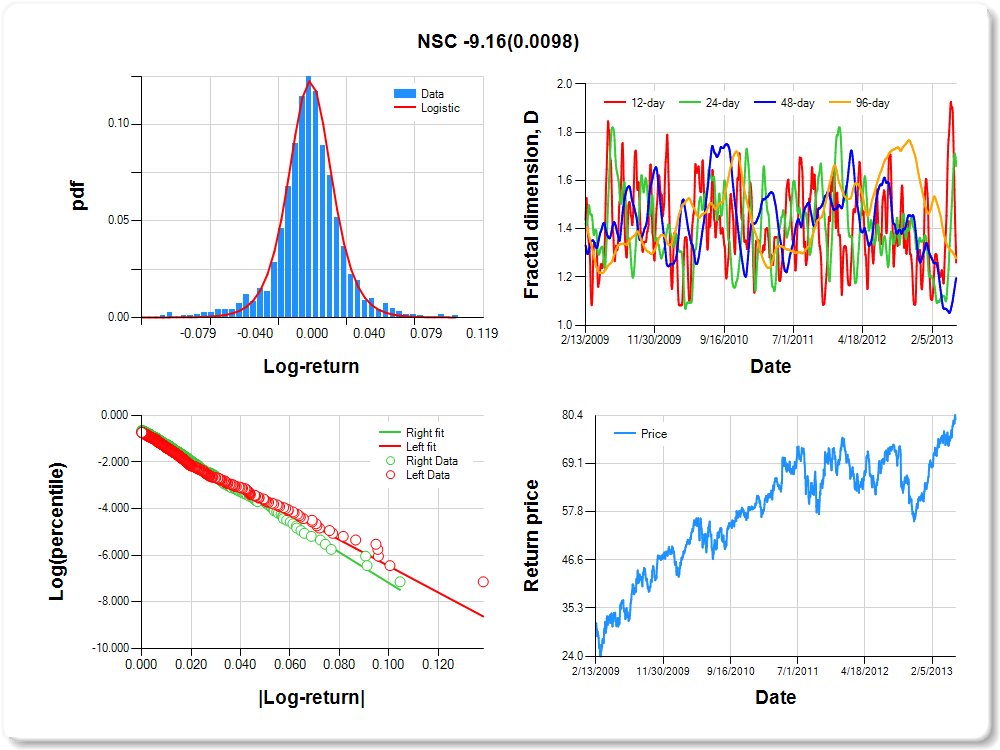

NSC

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.08 |

-0.07 |

-0.04 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.06 |

0.07 |

-0.06 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.249 |

0.141 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.823 |

0.056 |

-14.739 |

0.0000 |

|log-return| |

-56.419 |

2.368 |

-23.828 |

0.0000 |

I(right-tail) |

0.197 |

0.080 |

2.475 |

0.0134 |

|log-return|*I(right-tail) |

-9.155 |

3.537 |

-2.589 |

0.0098 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.740 |

0.340 |

0.804 |

0.723 |

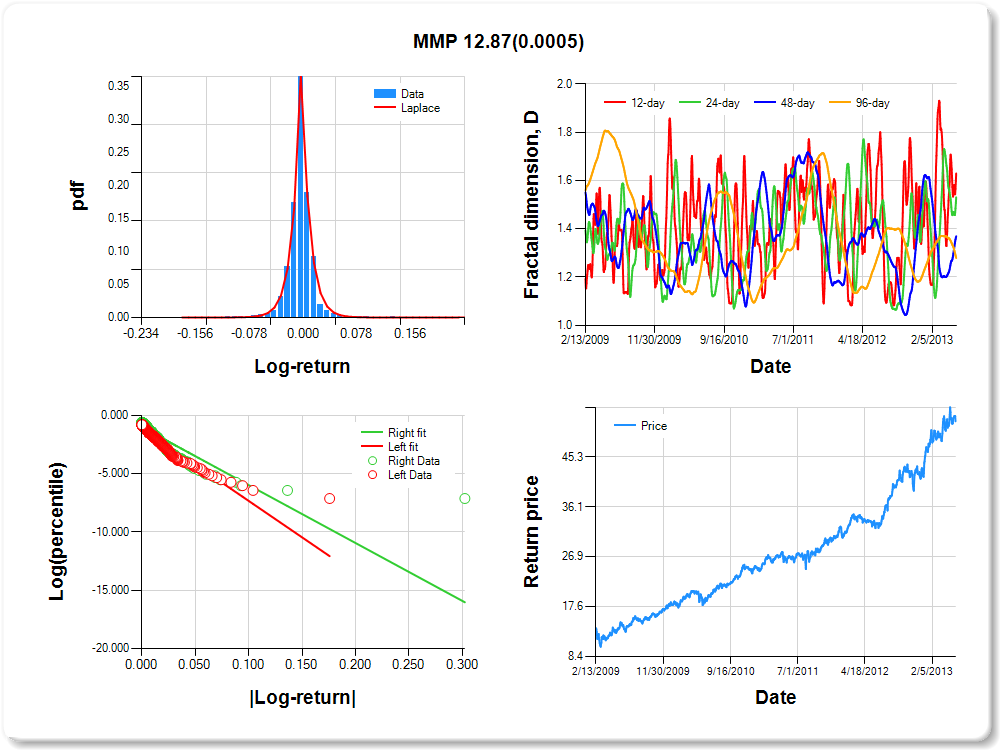

MMP

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.05 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.05 |

0.07 |

1.04 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.441 |

0.086 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.083 |

0.054 |

-20.059 |

0.0000 |

|log-return| |

-62.517 |

2.862 |

-21.845 |

0.0000 |

I(right-tail) |

0.065 |

0.071 |

0.908 |

0.3640 |

|log-return|*I(right-tail) |

12.867 |

3.665 |

3.511 |

0.0005 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.370 |

0.469 |

0.631 |

0.721 |

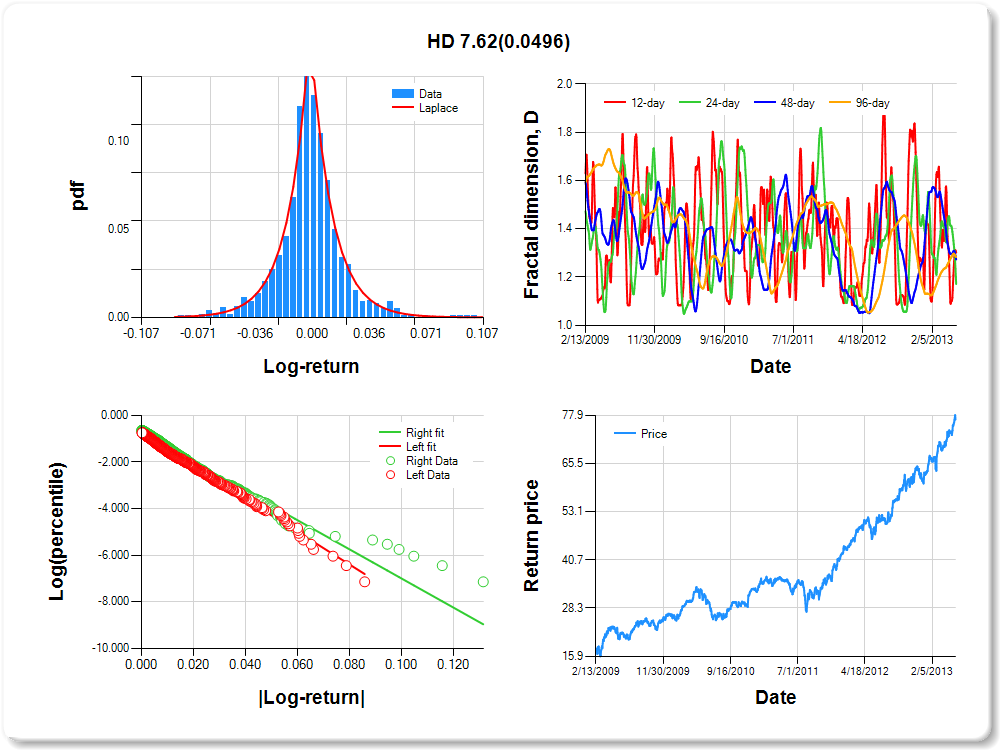

HD

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.06 |

0.08 |

0.75 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.348 |

0.212 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.793 |

0.057 |

-13.815 |

0.0000 |

|log-return| |

-70.050 |

2.944 |

-23.795 |

0.0000 |

I(right-tail) |

0.040 |

0.078 |

0.514 |

0.6071 |

|log-return|*I(right-tail) |

7.616 |

3.876 |

1.965 |

0.0496 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.699 |

0.829 |

0.727 |

0.717 |

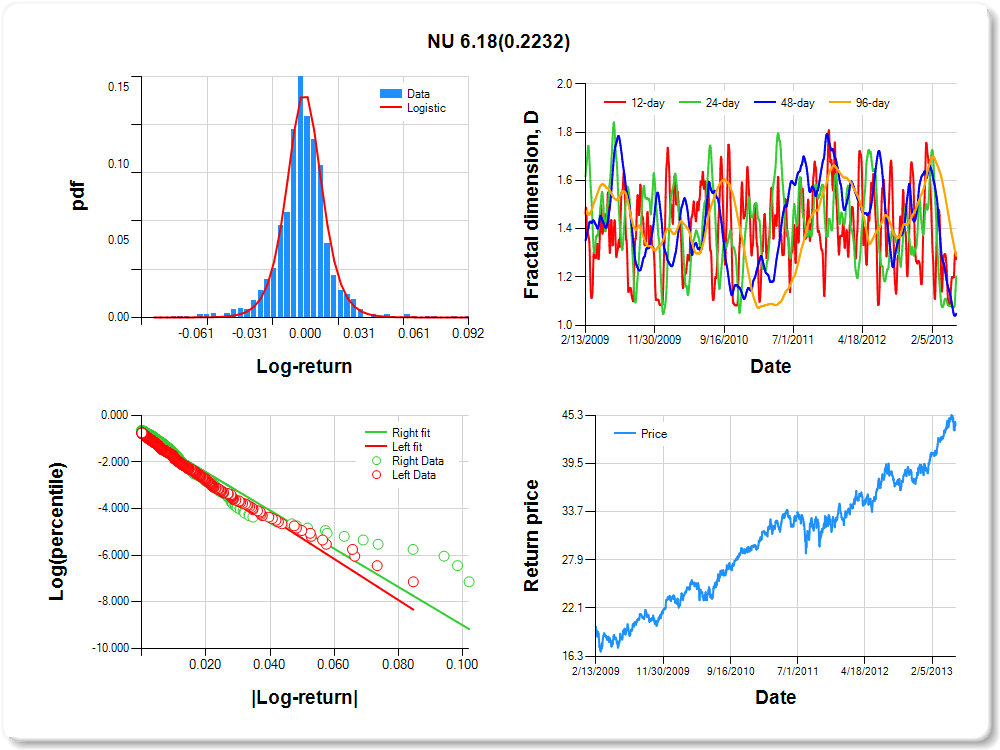

NU

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.07 |

1.68 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.137 |

0.117 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.854 |

0.056 |

-15.246 |

0.0000 |

|log-return| |

-88.095 |

3.737 |

-23.576 |

0.0000 |

I(right-tail) |

0.066 |

0.077 |

0.855 |

0.3928 |

|log-return|*I(right-tail) |

6.180 |

5.071 |

1.219 |

0.2232 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.726 |

0.797 |

0.952 |

0.712 |

PFE

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.04 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.06 |

1.34 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.099 |

0.125 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.813 |

0.055 |

-14.755 |

0.0000 |

|log-return| |

-78.961 |

3.300 |

-23.930 |

0.0000 |

I(right-tail) |

0.134 |

0.080 |

1.676 |

0.0940 |

|log-return|*I(right-tail) |

-1.787 |

4.691 |

-0.381 |

0.7034 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.676 |

0.608 |

0.848 |

0.711 |

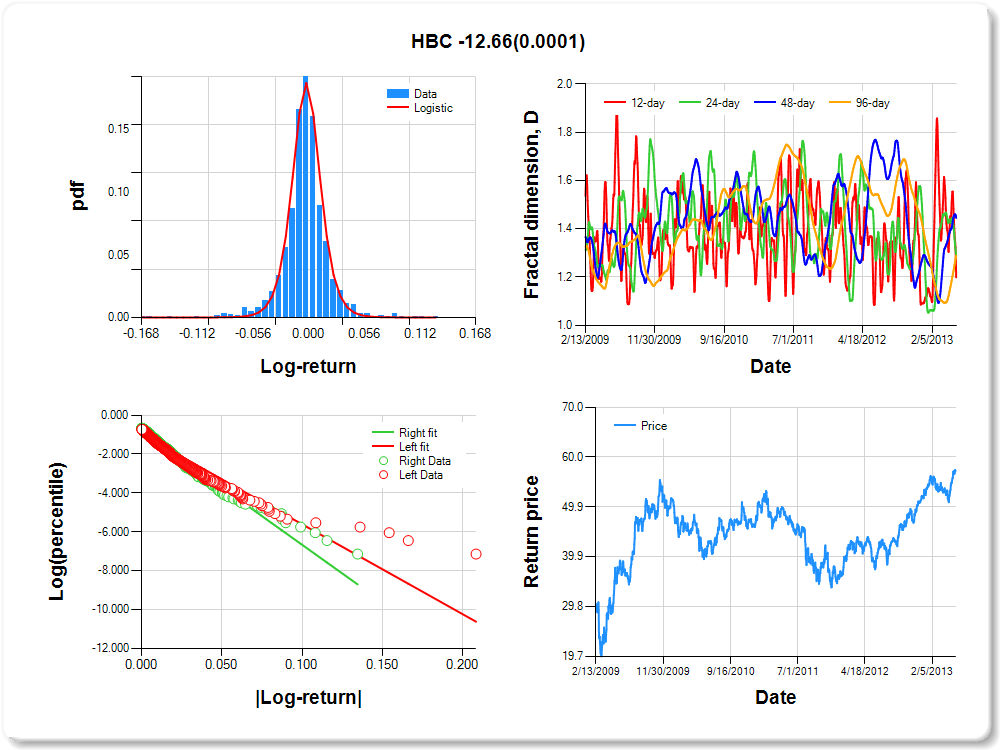

HBC

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.09 |

-0.07 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.06 |

0.09 |

0.79 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.377 |

0.092 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.984 |

0.052 |

-19.045 |

0.0000 |

|log-return| |

-46.203 |

2.001 |

-23.093 |

0.0000 |

I(right-tail) |

0.212 |

0.074 |

2.849 |

0.0045 |

|log-return|*I(right-tail) |

-12.659 |

3.123 |

-4.054 |

0.0001 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.801 |

0.711 |

0.555 |

0.711 |

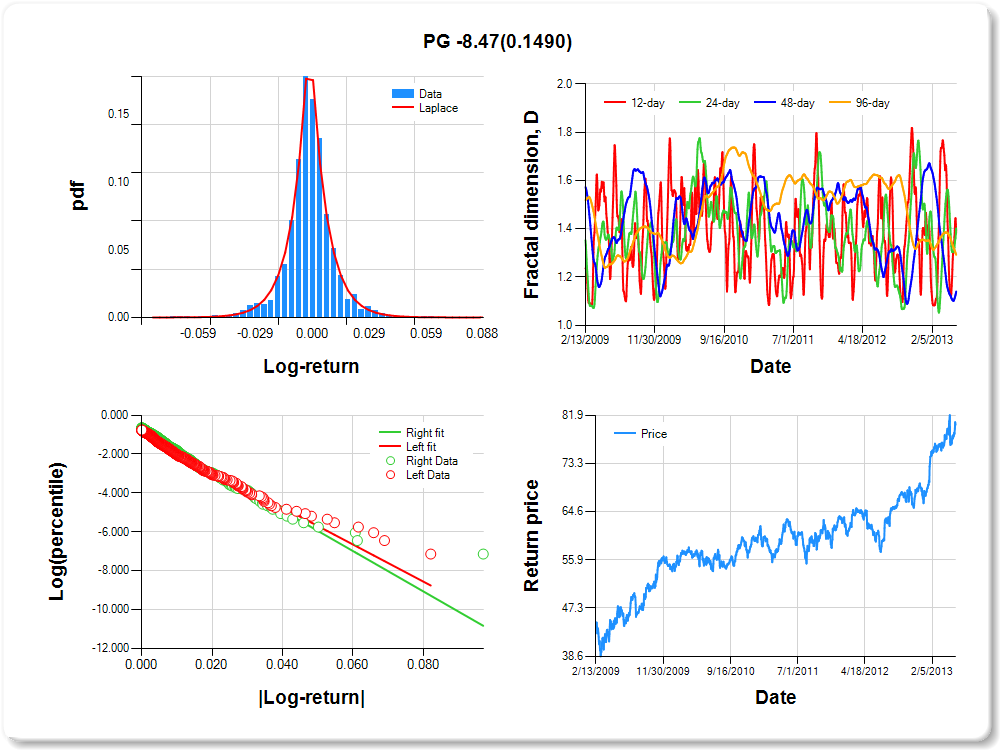

PG

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.02 |

0.04 |

0.04 |

1.17 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.138 |

0.158 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.915 |

0.055 |

-16.687 |

0.0000 |

|log-return| |

-95.360 |

4.082 |

-23.364 |

0.0000 |

I(right-tail) |

0.173 |

0.077 |

2.257 |

0.0242 |

|log-return|*I(right-tail) |

-8.469 |

5.865 |

-1.444 |

0.1490 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.617 |

0.598 |

0.860 |

0.708 |

DTE

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.07 |

0.81 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.220 |

0.099 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.922 |

0.058 |

-16.031 |

0.0000 |

|log-return| |

-84.446 |

3.708 |

-22.777 |

0.0000 |

I(right-tail) |

0.127 |

0.076 |

1.673 |

0.0947 |

|log-return|*I(right-tail) |

4.197 |

4.944 |

0.849 |

0.3961 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.711 |

0.811 |

0.960 |

0.703 |

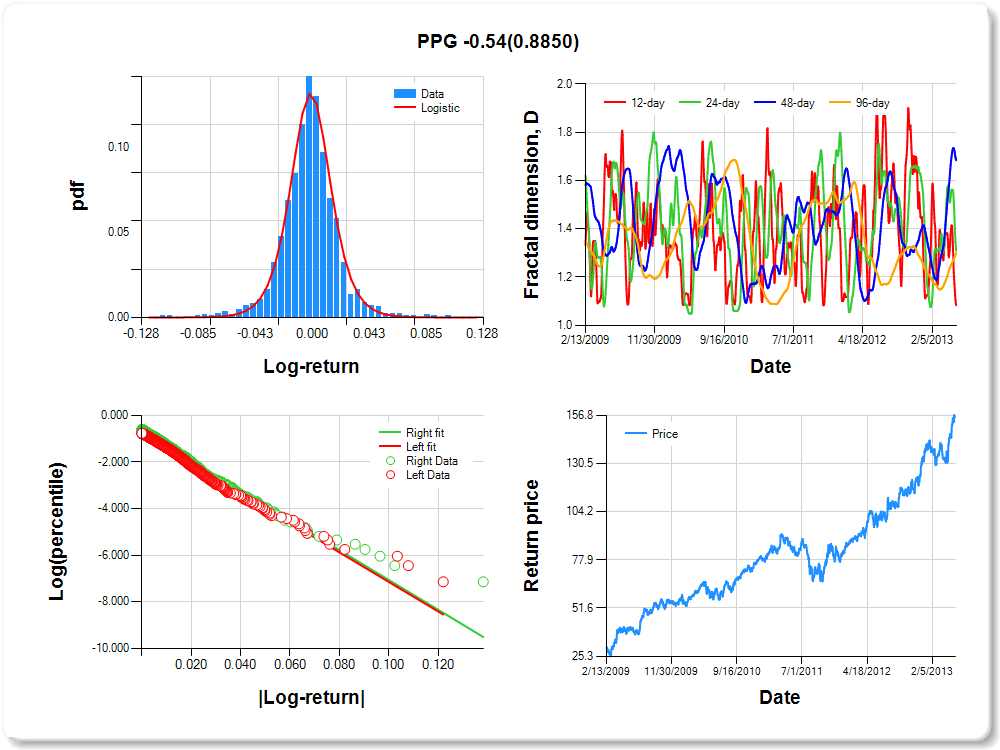

PPG

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.06 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.06 |

0.07 |

0.66 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.090 |

0.130 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.800 |

0.059 |

-13.642 |

0.0000 |

|log-return| |

-63.383 |

2.715 |

-23.344 |

0.0000 |

I(right-tail) |

0.138 |

0.080 |

1.735 |

0.0830 |

|log-return|*I(right-tail) |

-0.537 |

3.710 |

-0.145 |

0.8850 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.917 |

0.690 |

0.316 |

0.700 |

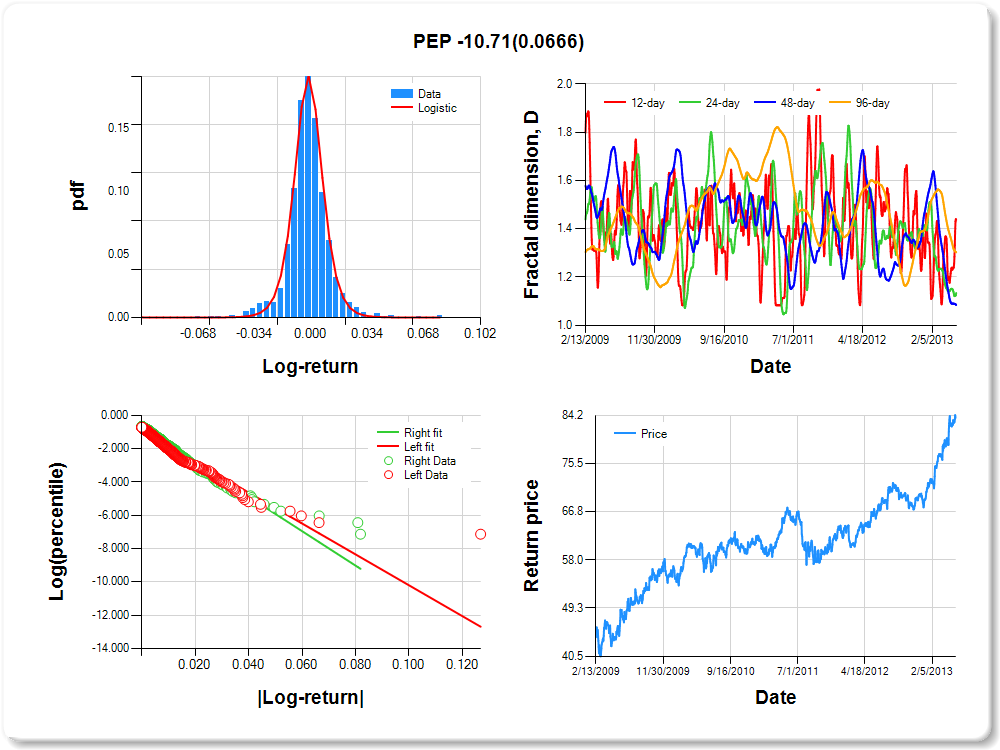

PEP

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.03 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.04 |

0.44 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.376 |

0.090 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.928 |

0.053 |

-17.563 |

0.0000 |

|log-return| |

-92.657 |

4.006 |

-23.128 |

0.0000 |

I(right-tail) |

0.184 |

0.076 |

2.416 |

0.0158 |

|log-return|*I(right-tail) |

-10.713 |

5.836 |

-1.836 |

0.0666 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.563 |

0.866 |

0.916 |

0.698 |

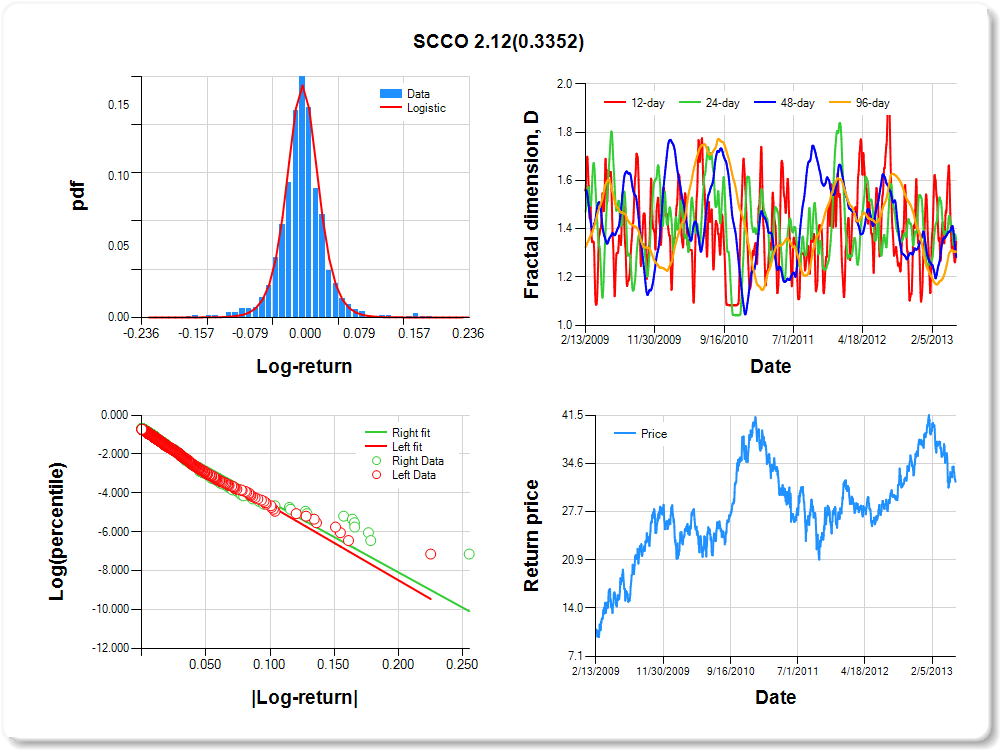

SCCO

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.13 |

-0.09 |

-0.05 |

-0.03 |

-0.02 |

0.00 |

0.02 |

0.05 |

0.10 |

0.17 |

1.52 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.103 |

0.105 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.810 |

0.055 |

-14.607 |

0.0000 |

|log-return| |

-38.337 |

1.604 |

-23.905 |

0.0000 |

I(right-tail) |

-0.018 |

0.076 |

-0.237 |

0.8128 |

|log-return|*I(right-tail) |

2.119 |

2.198 |

0.964 |

0.3352 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.651 |

0.644 |

0.717 |

0.695 |

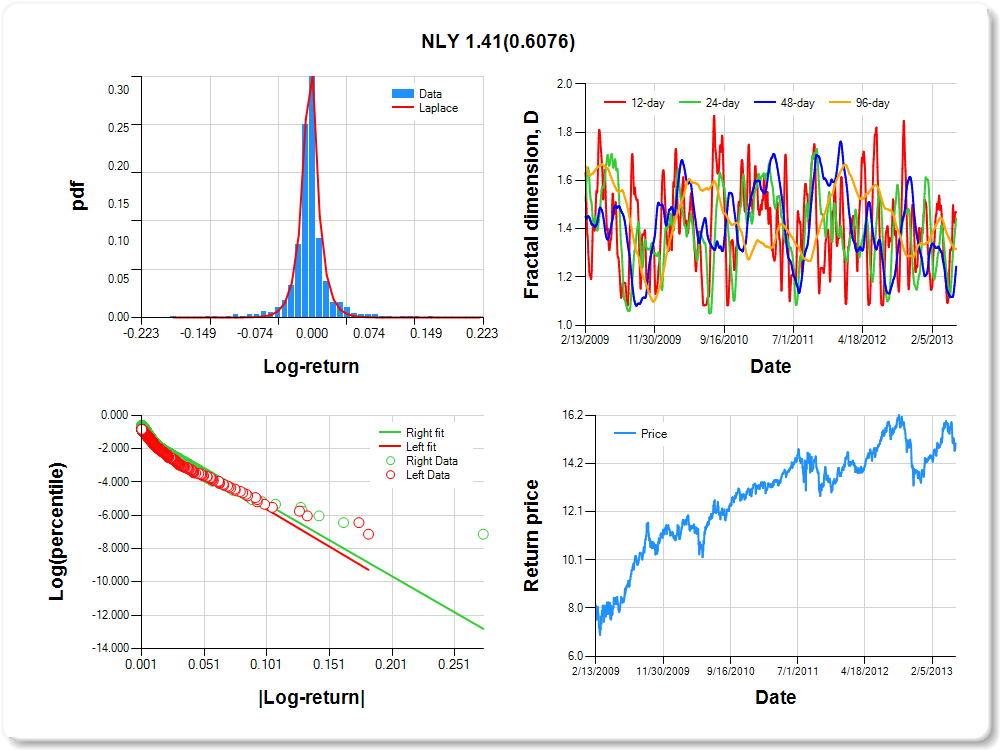

NLY

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.09 |

-0.08 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.08 |

0.10 |

0.51 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.335 |

0.079 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.161 |

0.053 |

-21.913 |

0.0000 |

|log-return| |

-44.664 |

2.049 |

-21.793 |

0.0000 |

I(right-tail) |

0.172 |

0.070 |

2.447 |

0.0145 |

|log-return|*I(right-tail) |

1.407 |

2.739 |

0.514 |

0.6076 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.531 |

0.557 |

0.756 |

0.683 |

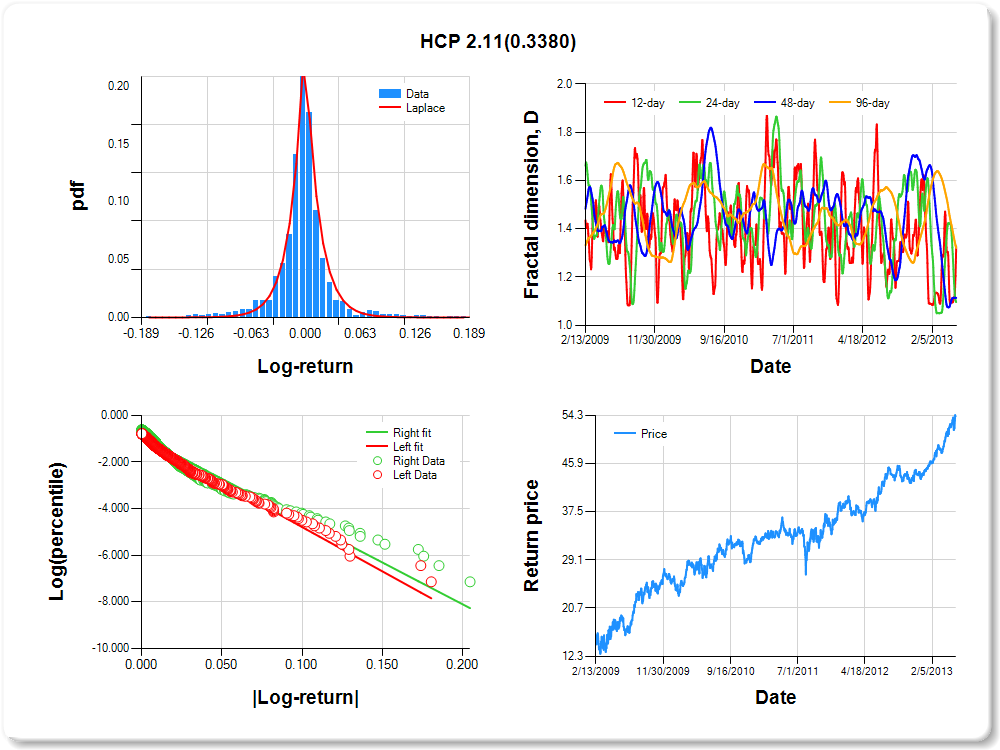

HCP

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.12 |

-0.10 |

-0.05 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.05 |

0.12 |

0.15 |

1.26 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.085 |

0.139 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.997 |

0.054 |

-18.500 |

0.0000 |

|log-return| |

-37.923 |

1.641 |

-23.108 |

0.0000 |

I(right-tail) |

0.062 |

0.072 |

0.864 |

0.3877 |

|log-return|*I(right-tail) |

2.110 |

2.202 |

0.959 |

0.3380 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.673 |

0.904 |

0.886 |

0.680 |

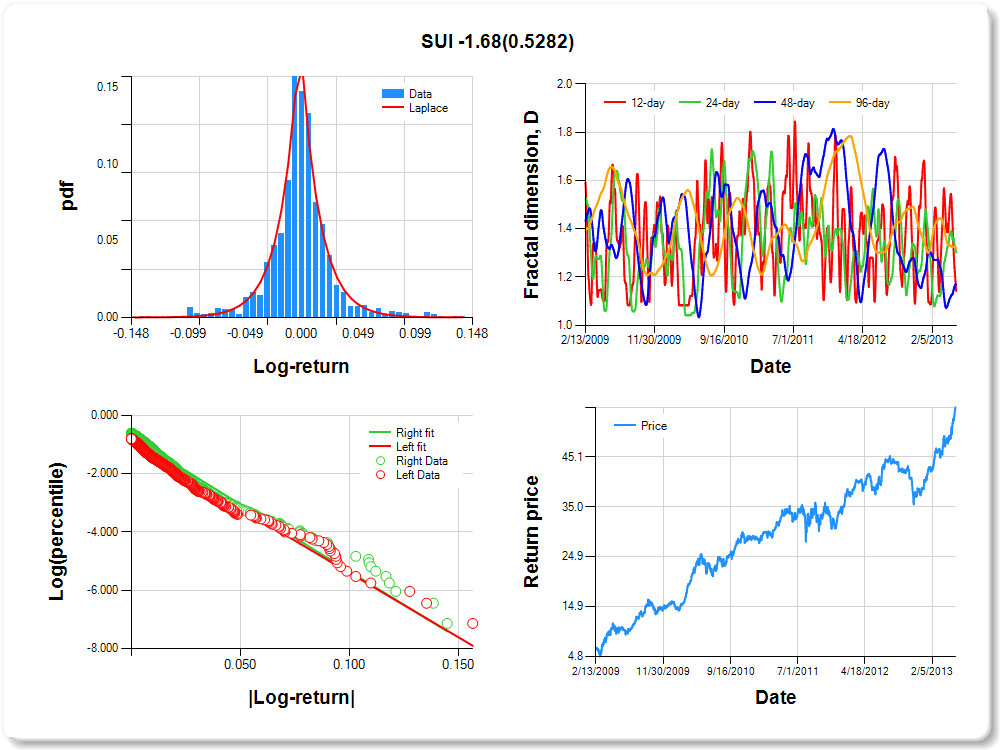

SUI

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.09 |

-0.09 |

-0.04 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.09 |

0.12 |

0.75 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.080 |

0.187 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.976 |

0.055 |

-17.595 |

0.0000 |

|log-return| |

-44.244 |

1.932 |

-22.899 |

0.0000 |

I(right-tail) |

0.222 |

0.076 |

2.935 |

0.0034 |

|log-return|*I(right-tail) |

-1.676 |

2.656 |

-0.631 |

0.5282 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.858 |

0.698 |

0.829 |

0.679 |

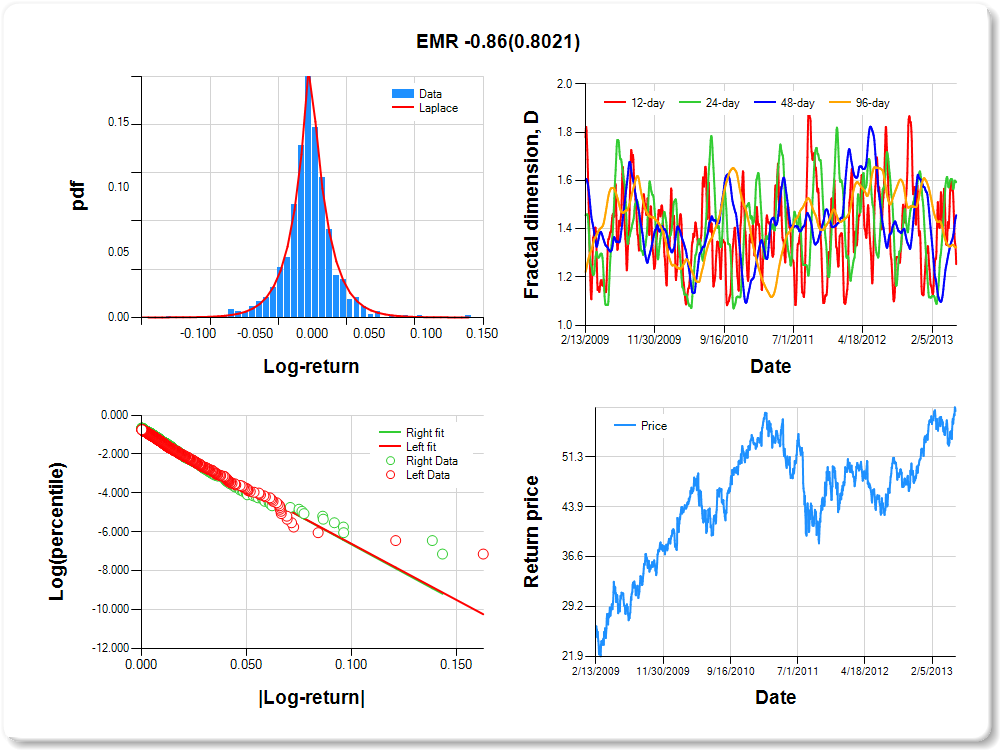

EMR

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.06 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.06 |

0.09 |

0.32 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.118 |

0.165 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.836 |

0.056 |

-14.940 |

0.0000 |

|log-return| |

-57.762 |

2.449 |

-23.590 |

0.0000 |

I(right-tail) |

0.056 |

0.077 |

0.733 |

0.4638 |

|log-return|*I(right-tail) |

-0.857 |

3.419 |

-0.251 |

0.8021 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.746 |

0.406 |

0.544 |

0.676 |

MMC

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.06 |

0.09 |

1.84 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.015 |

0.158 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.870 |

0.056 |

-15.628 |

0.0000 |

|log-return| |

-68.106 |

2.917 |

-23.347 |

0.0000 |

I(right-tail) |

0.031 |

0.077 |

0.404 |

0.6860 |

|log-return|*I(right-tail) |

4.167 |

3.948 |

1.056 |

0.2914 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.686 |

0.463 |

0.827 |

0.675 |

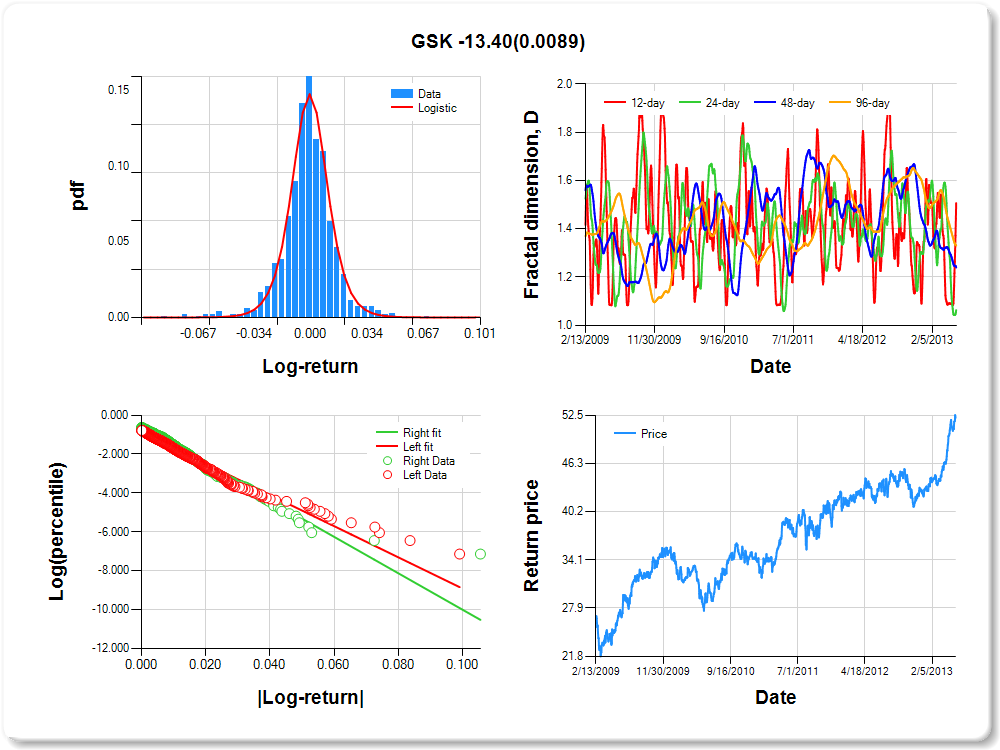

GSK

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

1.05 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.034 |

0.116 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.880 |

0.057 |

-15.395 |

0.0000 |

|log-return| |

-80.161 |

3.475 |

-23.070 |

0.0000 |

I(right-tail) |

0.256 |

0.080 |

3.196 |

0.0014 |

|log-return|*I(right-tail) |

-13.399 |

5.114 |

-2.620 |

0.0089 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.493 |

0.937 |

0.760 |

0.669 |

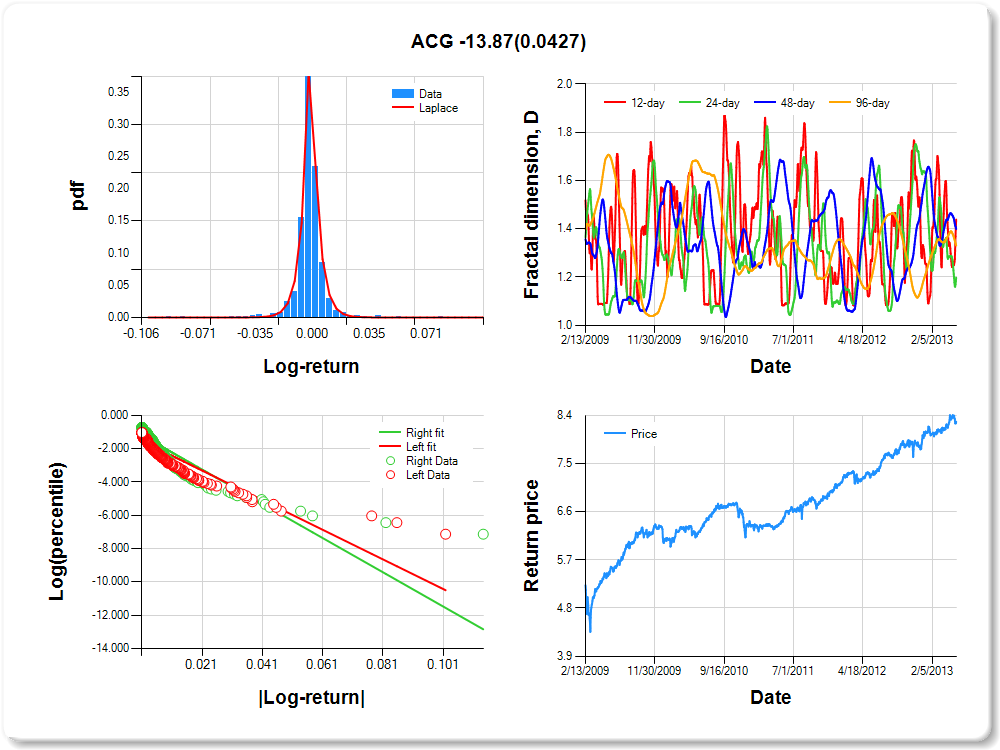

ACG

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.03 |

-0.01 |

-0.01 |

0.00 |

0.00 |

0.00 |

0.01 |

0.03 |

0.04 |

0.88 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.086 |

0.072 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.435 |

0.057 |

-25.050 |

0.0000 |

|log-return| |

-88.944 |

4.785 |

-18.589 |

0.0000 |

I(right-tail) |

0.352 |

0.077 |

4.595 |

0.0000 |

|log-return|*I(right-tail) |

-13.870 |

6.835 |

-2.029 |

0.0427 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.562 |

0.802 |

0.601 |

0.669 |

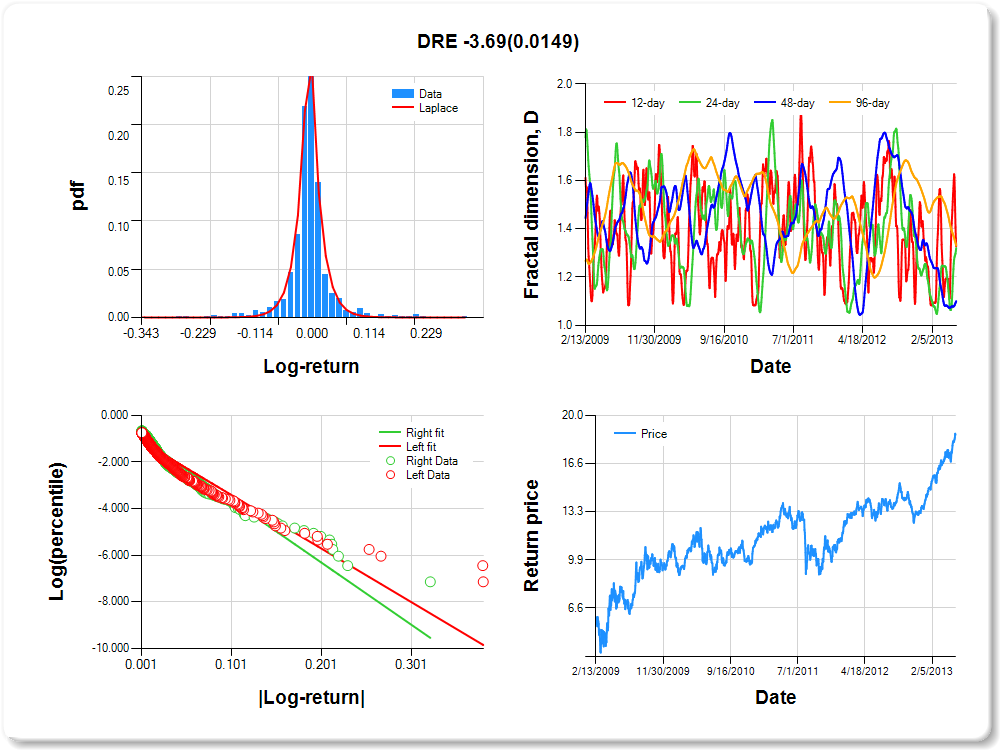

DRE

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.18 |

-0.14 |

-0.06 |

-0.04 |

-0.01 |

0.00 |

0.01 |

0.06 |

0.15 |

0.22 |

0.58 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.147 |

0.097 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.121 |

0.049 |

-22.743 |

0.0000 |

|log-return| |

-22.973 |

1.017 |

-22.596 |

0.0000 |

I(right-tail) |

0.137 |

0.069 |

1.979 |

0.0480 |

|log-return|*I(right-tail) |

-3.691 |

1.514 |

-2.437 |

0.0149 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.673 |

0.680 |

0.900 |

0.669 |

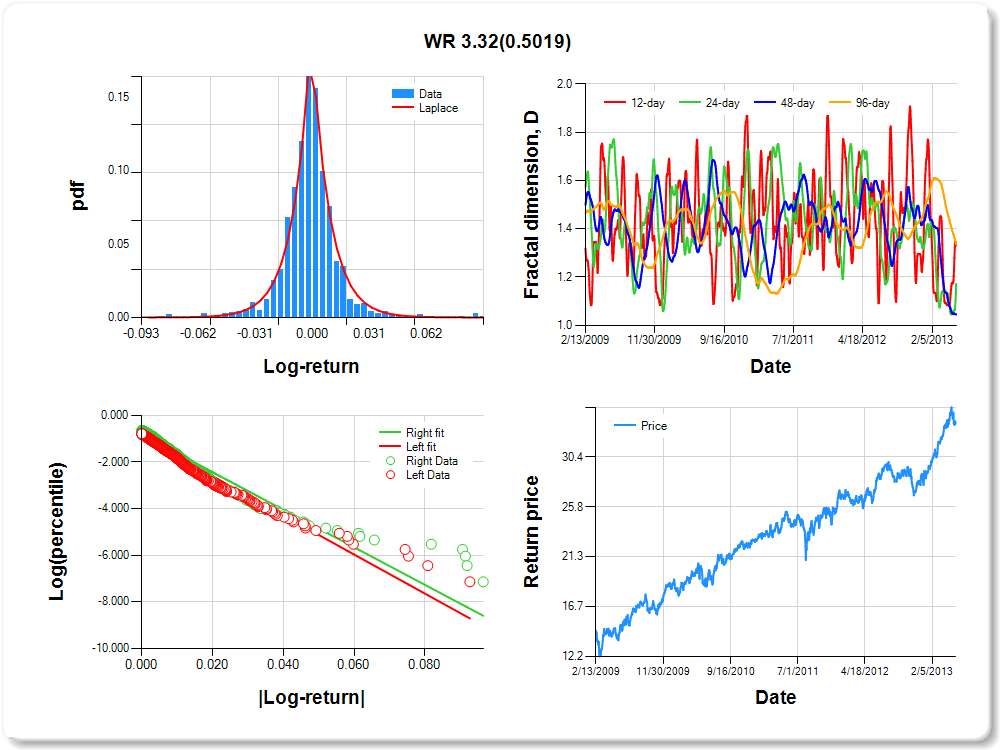

WR

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.06 |

0.43 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.012 |

0.177 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.922 |

0.056 |

-16.352 |

0.0000 |

|log-return| |

-83.780 |

3.657 |

-22.911 |

0.0000 |

I(right-tail) |

0.110 |

0.077 |

1.428 |

0.1536 |

|log-return|*I(right-tail) |

3.320 |

4.942 |

0.672 |

0.5019 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.669 |

0.828 |

0.955 |

0.665 |

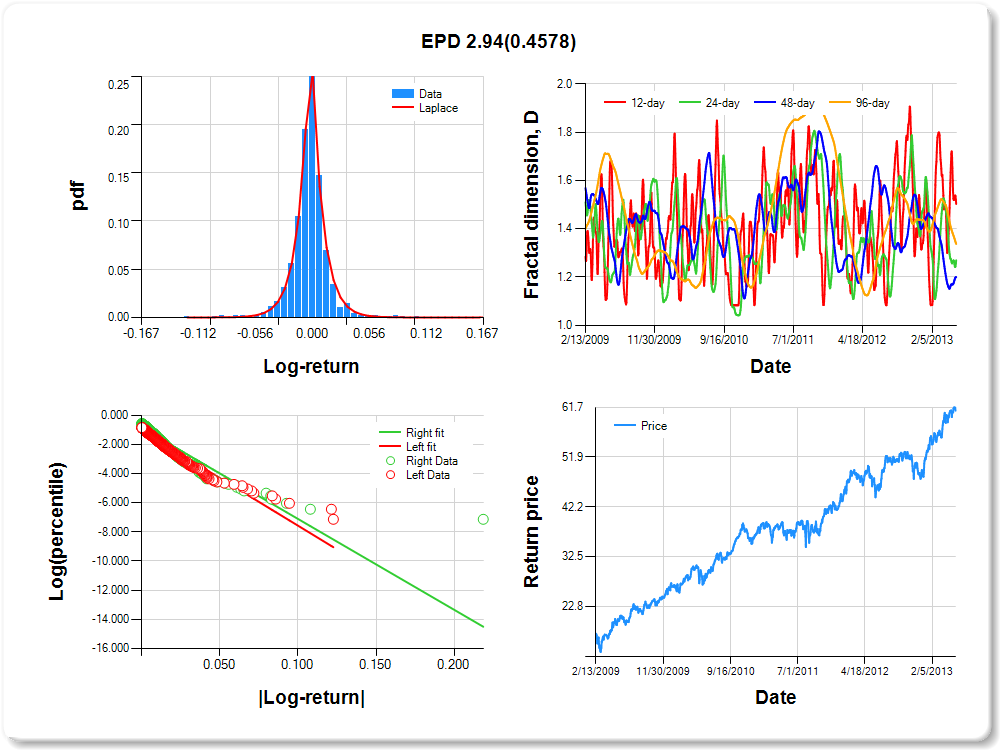

EPD

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.07 |

1.39 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.466 |

0.109 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.039 |

0.057 |

-18.370 |

0.0000 |

|log-return| |

-65.269 |

2.968 |

-21.990 |

0.0000 |

I(right-tail) |

0.168 |

0.074 |

2.269 |

0.0234 |

|log-return|*I(right-tail) |

2.943 |

3.962 |

0.743 |

0.4578 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.497 |

0.730 |

0.800 |

0.663 |

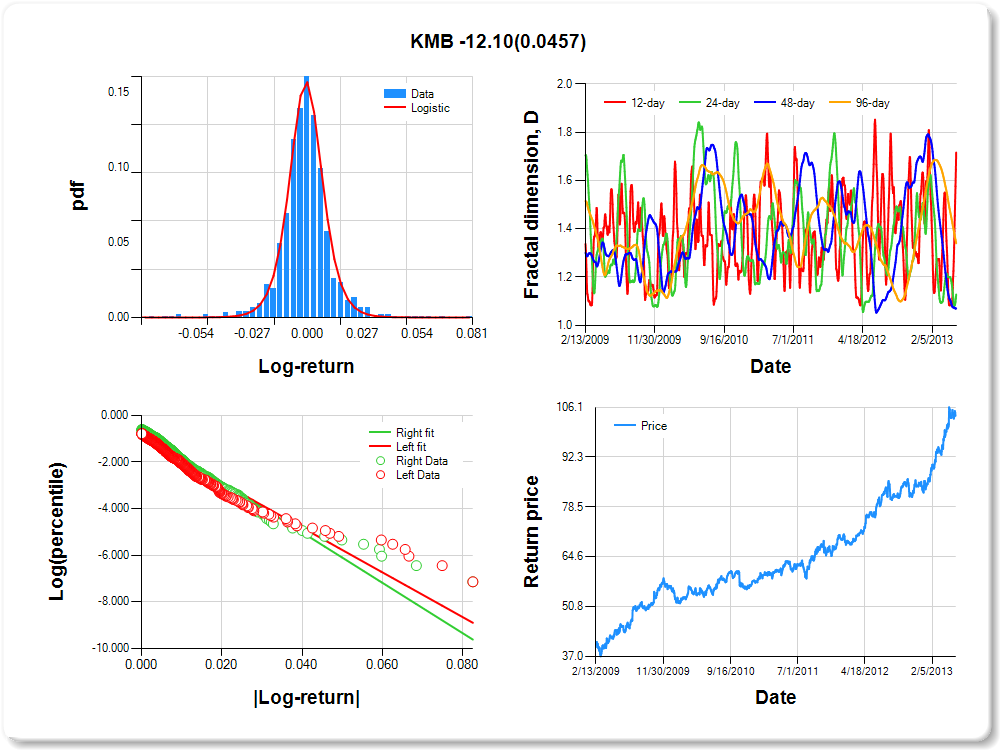

KMB

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.04 |

-0.02 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.02 |

0.03 |

0.05 |

1.16 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.021 |

0.109 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.976 |

0.055 |

-17.704 |

0.0000 |

|log-return| |

-95.814 |

4.238 |

-22.606 |

0.0000 |

I(right-tail) |

0.278 |

0.077 |

3.635 |

0.0003 |

|log-return|*I(right-tail) |

-12.097 |

6.047 |

-2.001 |

0.0457 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.284 |

0.872 |

0.930 |

0.660 |

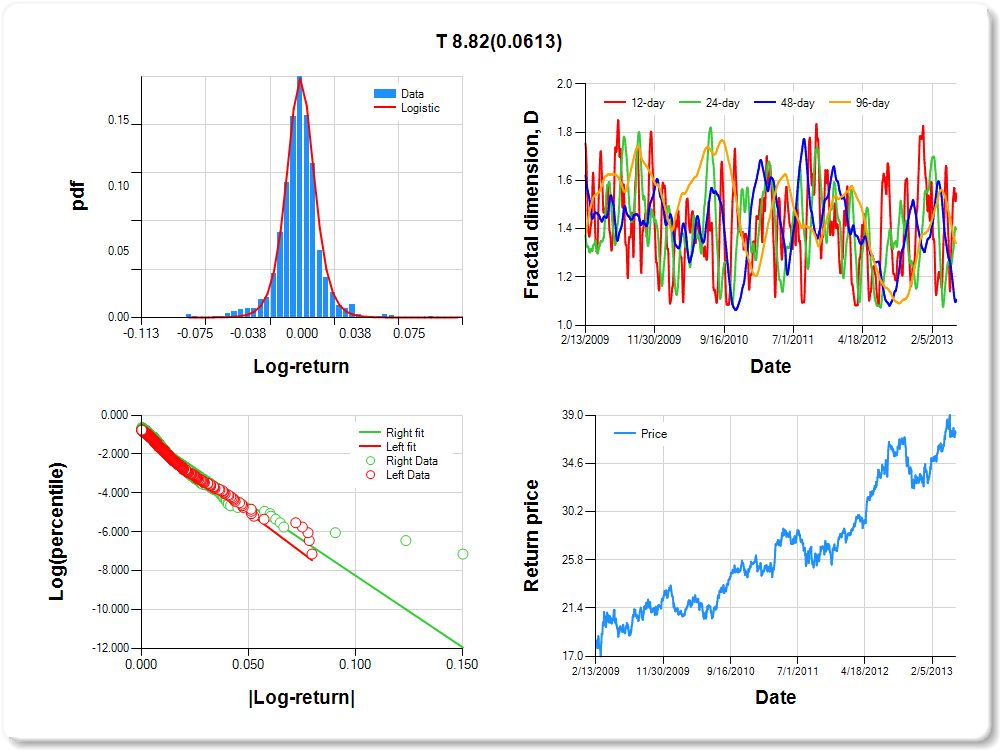

T

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.06 |

-0.18 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.512 |

0.094 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.876 |

0.056 |

-15.653 |

0.0000 |

|log-return| |

-82.350 |

3.526 |

-23.355 |

0.0000 |

I(right-tail) |

-0.001 |

0.076 |

-0.017 |

0.9863 |

|log-return|*I(right-tail) |

8.824 |

4.711 |

1.873 |

0.0613 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.453 |

0.599 |

0.894 |

0.658 |

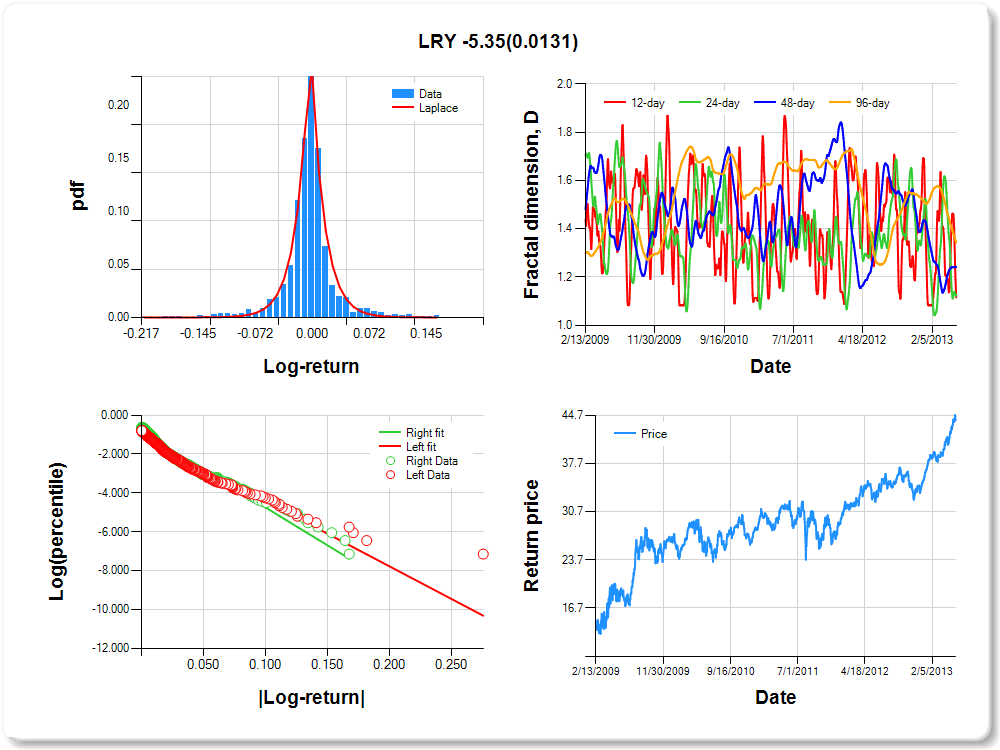

LRY

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.13 |

-0.11 |

-0.05 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.05 |

0.11 |

0.13 |

0.83 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.431 |

0.130 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.061 |

0.053 |

-20.102 |

0.0000 |

|log-return| |

-33.549 |

1.483 |

-22.620 |

0.0000 |

I(right-tail) |

0.206 |

0.072 |

2.865 |

0.0042 |

|log-return|*I(right-tail) |

-5.347 |

2.151 |

-2.486 |

0.0131 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.884 |

0.877 |

0.758 |

0.658 |

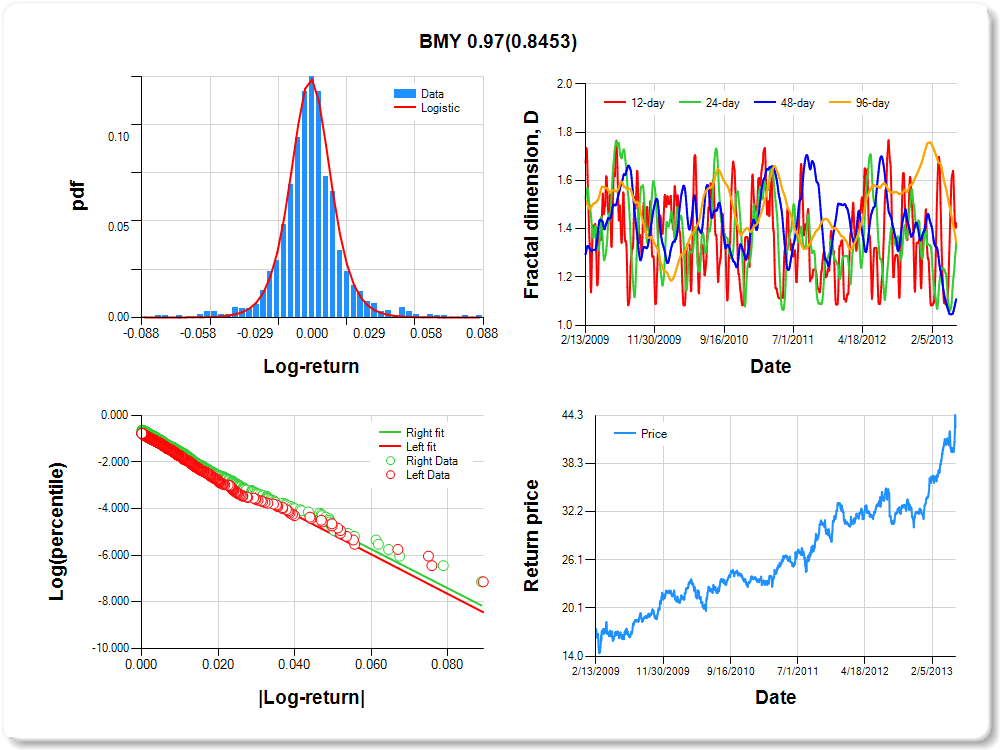

BMY

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.05 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.06 |

0.05 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.020 |

0.129 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.861 |

0.057 |

-15.057 |

0.0000 |

|log-return| |

-84.732 |

3.649 |

-23.223 |

0.0000 |

I(right-tail) |

0.166 |

0.079 |

2.103 |

0.0356 |

|log-return|*I(right-tail) |

0.966 |

4.949 |

0.195 |

0.8453 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.594 |

0.650 |

0.891 |

0.656 |

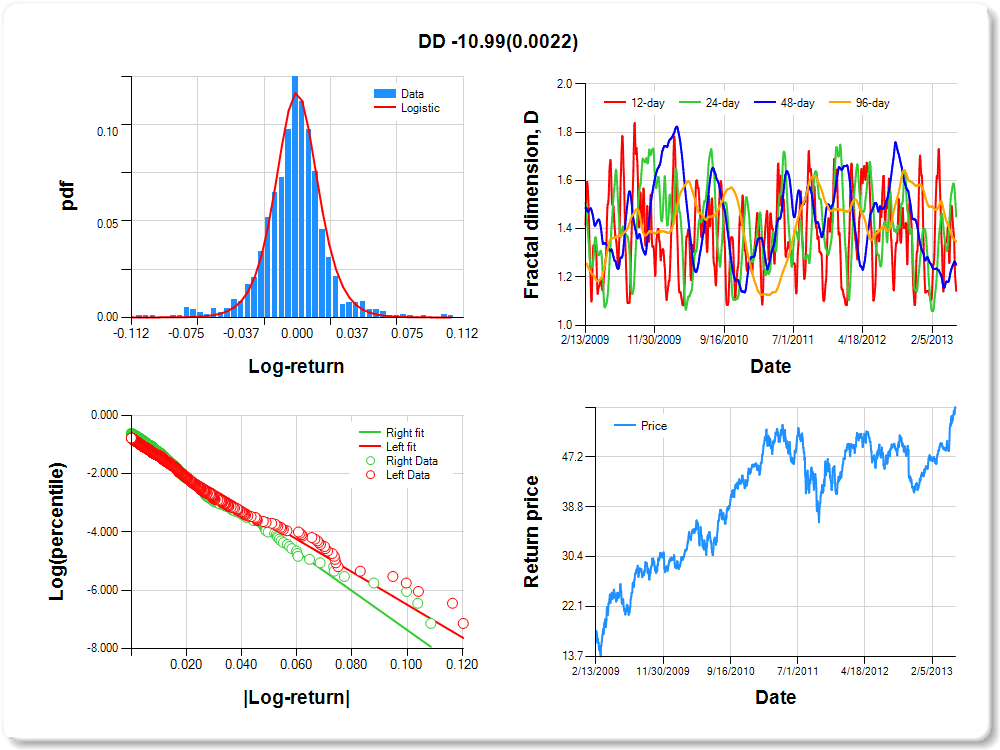

DD

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.08 |

-0.07 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.06 |

0.08 |

0.48 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.117 |

0.141 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.878 |

0.057 |

-15.433 |

0.0000 |

|log-return| |

-56.085 |

2.415 |

-23.225 |

0.0000 |

I(right-tail) |

0.233 |

0.079 |

2.953 |

0.0032 |

|log-return|*I(right-tail) |

-10.994 |

3.591 |

-3.062 |

0.0022 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.857 |

0.549 |

0.749 |

0.653 |

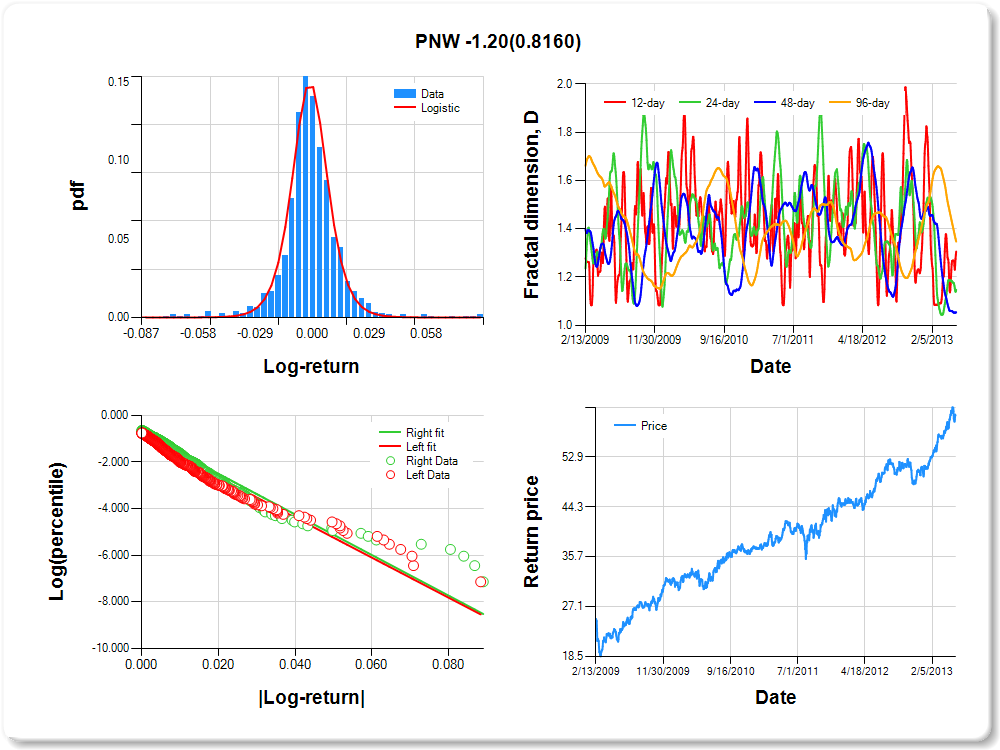

PNW

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.06 |

1.55 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.001 |

0.114 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.943 |

0.054 |

-17.438 |

0.0000 |

|log-return| |

-85.826 |

3.704 |

-23.170 |

0.0000 |

I(right-tail) |

0.183 |

0.076 |

2.408 |

0.0162 |

|log-return|*I(right-tail) |

-1.198 |

5.148 |

-0.233 |

0.8160 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.694 |

0.853 |

0.946 |

0.653 |

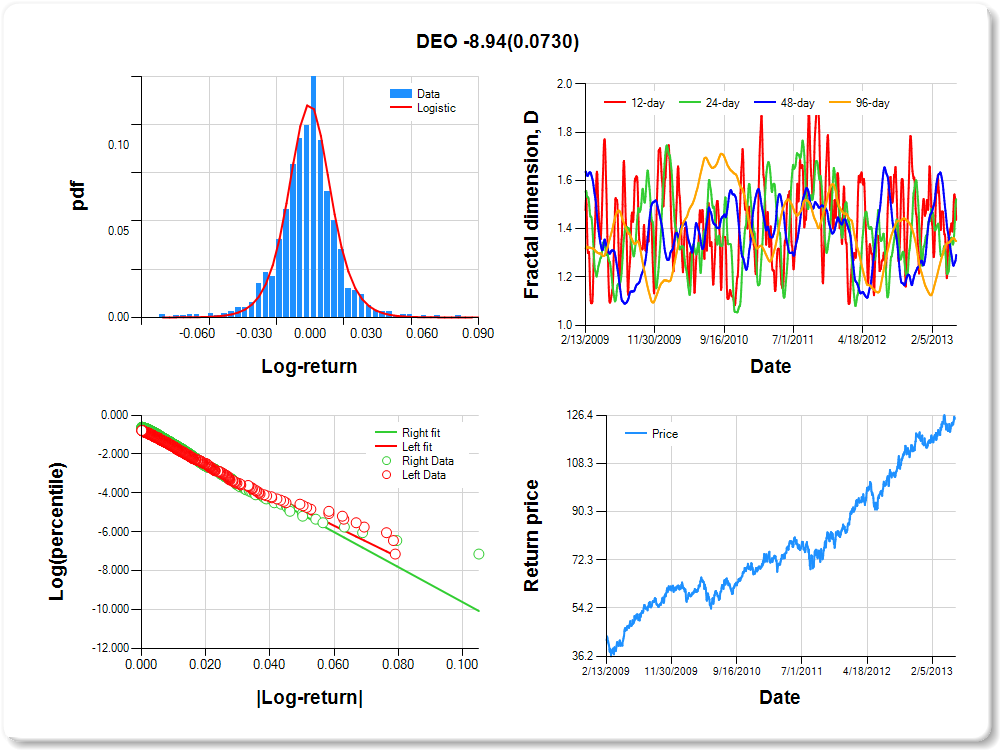

DEO

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

1.36 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.216 |

0.138 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.821 |

0.059 |

-13.994 |

0.0000 |

|log-return| |

-80.980 |

3.483 |

-23.250 |

0.0000 |

I(right-tail) |

0.210 |

0.080 |

2.603 |

0.0094 |

|log-return|*I(right-tail) |

-8.940 |

4.982 |

-1.795 |

0.0730 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.563 |

0.477 |

0.708 |

0.651 |

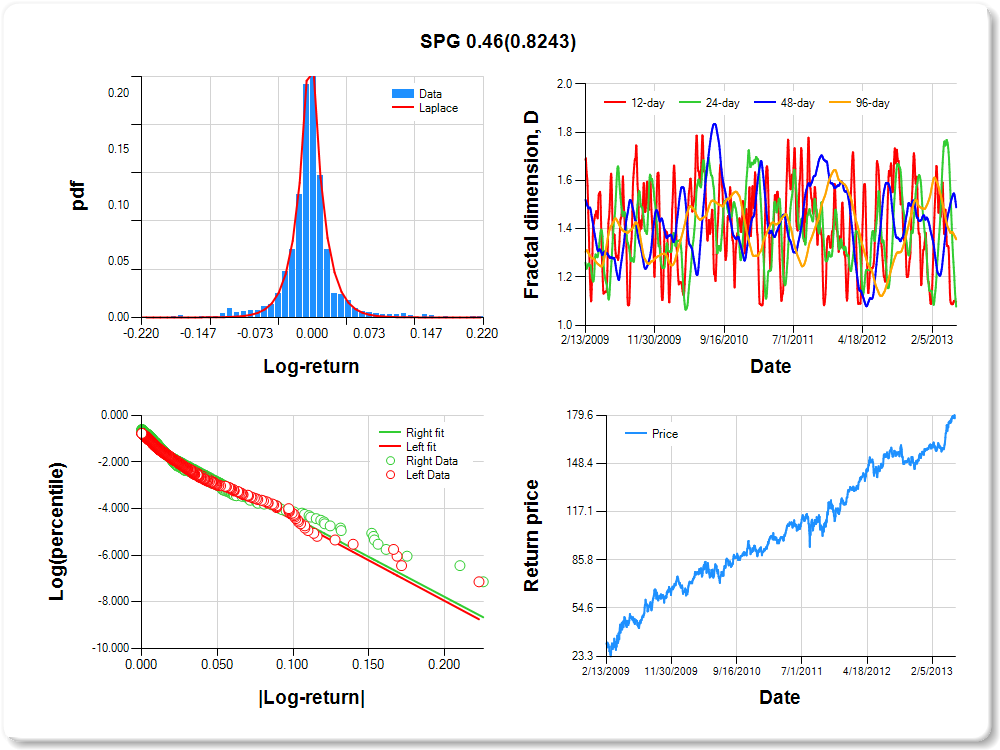

SPG

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.12 |

-0.10 |

-0.05 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.05 |

0.13 |

0.17 |

0.04 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.002 |

0.122 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.017 |

0.053 |

-19.242 |

0.0000 |

|log-return| |

-34.669 |

1.502 |

-23.087 |

0.0000 |

I(right-tail) |

0.081 |

0.071 |

1.139 |

0.2550 |

|log-return|*I(right-tail) |

0.455 |

2.051 |

0.222 |

0.8243 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.903 |

0.922 |

0.511 |

0.644 |

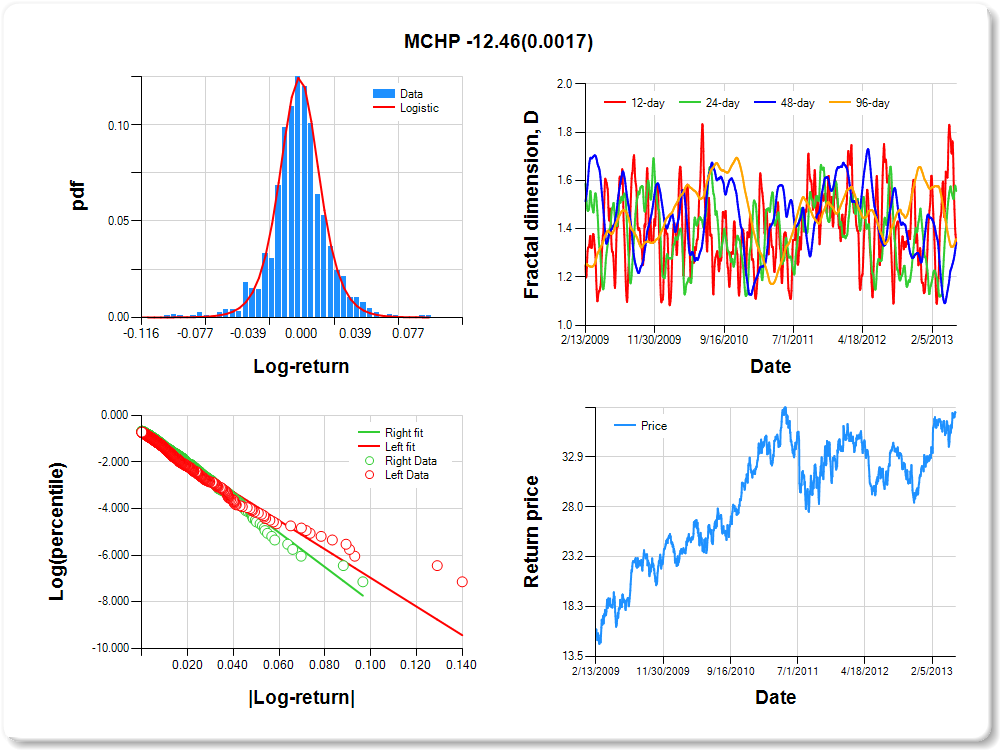

MCHP

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.08 |

-0.06 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.06 |

1.27 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.321 |

0.137 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.820 |

0.055 |

-14.797 |

0.0000 |

|log-return| |

-61.375 |

2.589 |

-23.703 |

0.0000 |

I(right-tail) |

0.237 |

0.081 |

2.910 |

0.0037 |

|log-return|*I(right-tail) |

-12.455 |

3.959 |

-3.146 |

0.0017 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.666 |

0.443 |

0.658 |

0.642 |

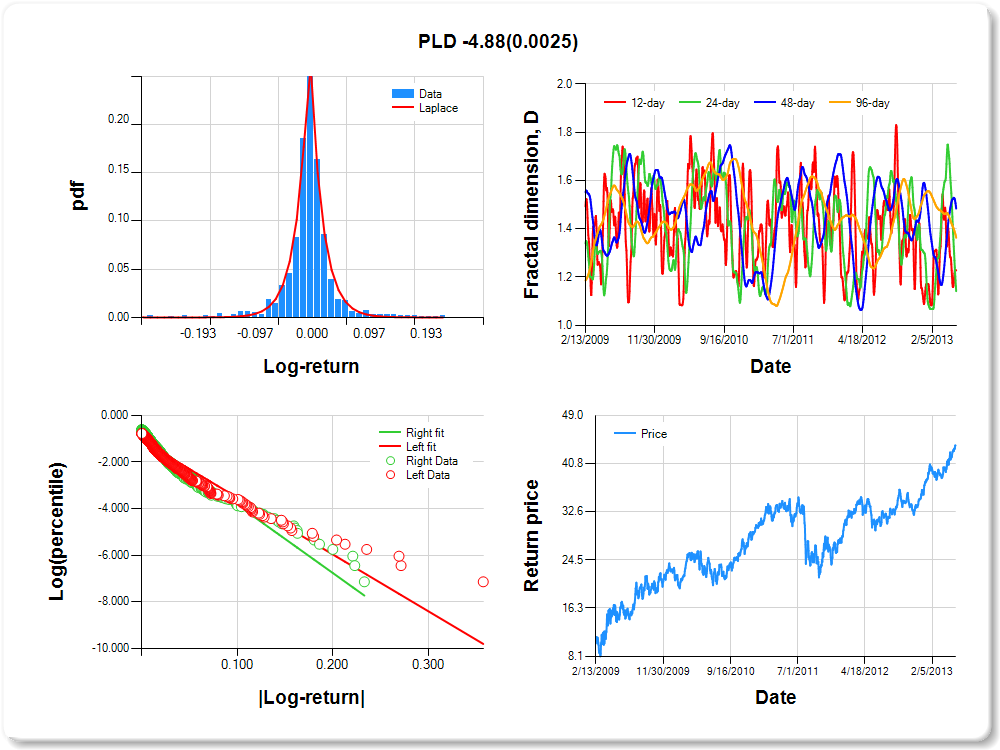

PLD

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.18 |

-0.14 |

-0.06 |

-0.04 |

-0.01 |

0.00 |

0.02 |

0.06 |

0.15 |

0.20 |

0.80 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.367 |

0.124 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.091 |

0.052 |

-21.141 |

0.0000 |

|log-return| |

-24.351 |

1.079 |

-22.570 |

0.0000 |

I(right-tail) |

0.180 |

0.071 |

2.559 |

0.0106 |

|log-return|*I(right-tail) |

-4.876 |

1.607 |

-3.034 |

0.0025 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.772 |

0.858 |

0.516 |

0.637 |

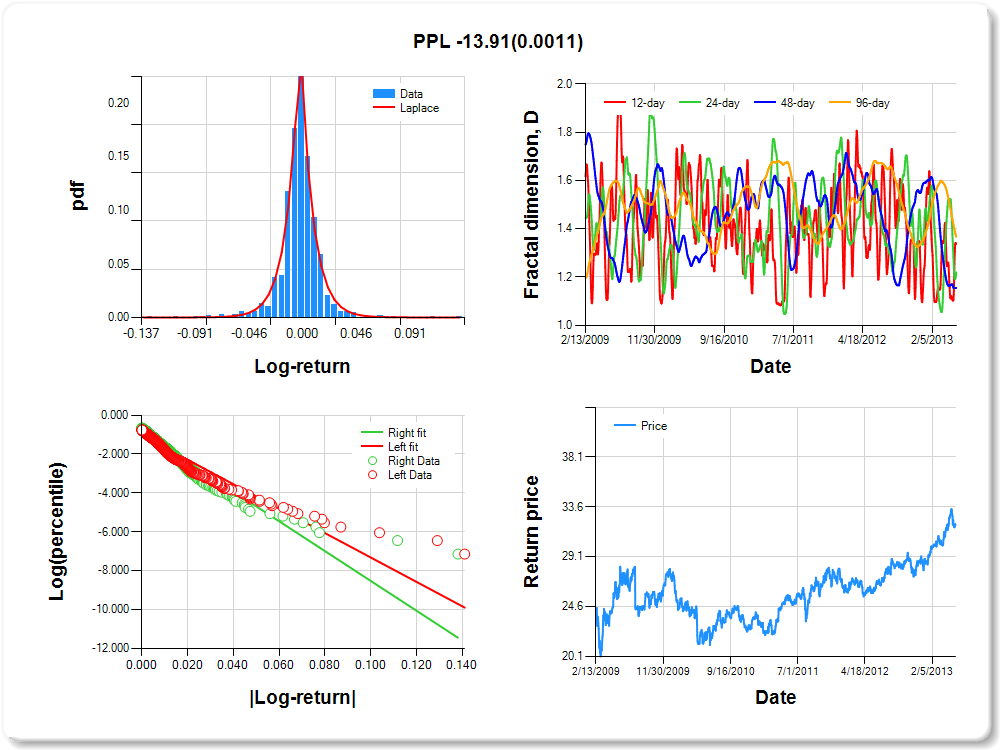

PPL

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.08 |

-0.06 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.05 |

0.06 |

0.82 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.019 |

0.129 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.023 |

0.052 |

-19.530 |

0.0000 |

|log-return| |

-62.807 |

2.773 |

-22.651 |

0.0000 |

I(right-tail) |

0.188 |

0.074 |

2.537 |

0.0113 |

|log-return|*I(right-tail) |

-13.905 |

4.251 |

-3.271 |

0.0011 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.662 |

0.781 |

0.845 |

0.633 |

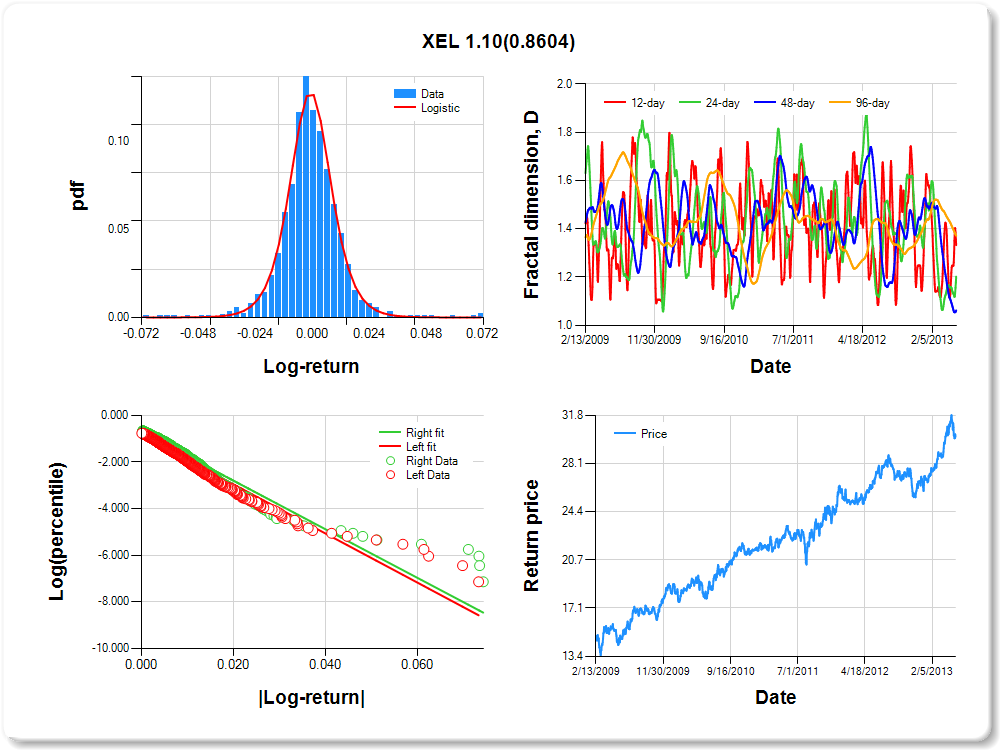

XEL

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.03 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.05 |

1.22 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.003 |

0.134 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.856 |

0.057 |

-14.954 |

0.0000 |

|log-return| |

-105.226 |

4.554 |

-23.104 |

0.0000 |

I(right-tail) |

0.137 |

0.080 |

1.717 |

0.0863 |

|log-return|*I(right-tail) |

1.105 |

6.282 |

0.176 |

0.8604 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.668 |

0.798 |

0.938 |

0.629 |

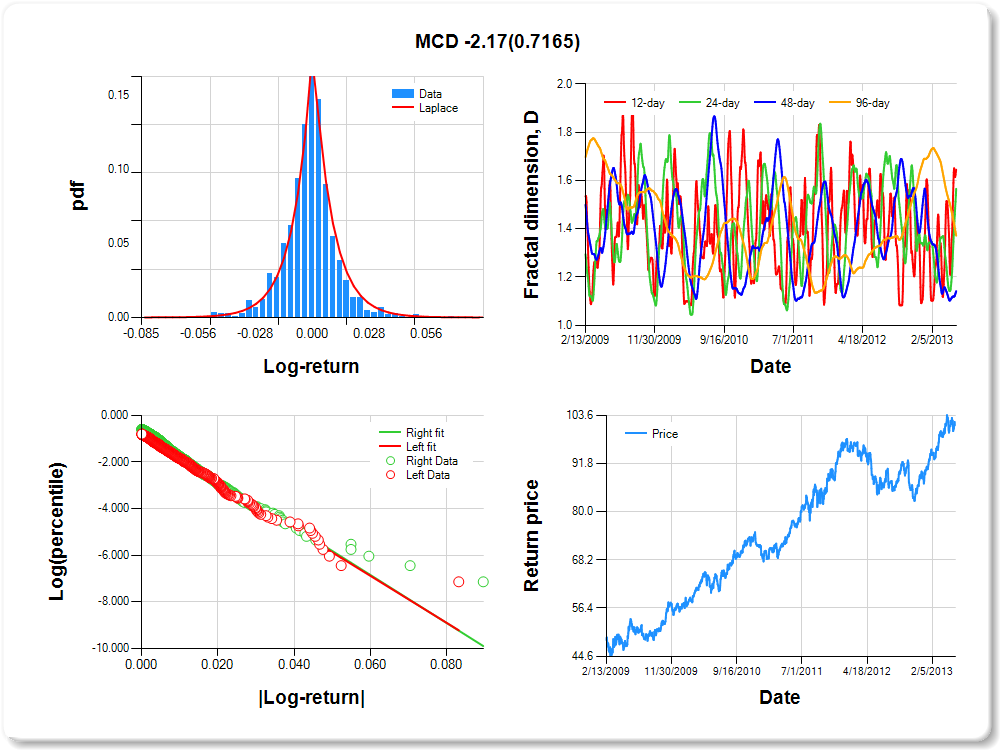

MCD

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.04 |

1.78 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.026 |

0.186 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.836 |

0.060 |

-14.037 |

0.0000 |

|log-return| |

-100.718 |

4.378 |

-23.005 |

0.0000 |

I(right-tail) |

0.167 |

0.080 |

2.102 |

0.0358 |

|log-return|*I(right-tail) |

-2.168 |

5.967 |

-0.363 |

0.7165 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.355 |

0.434 |

0.858 |

0.629 |

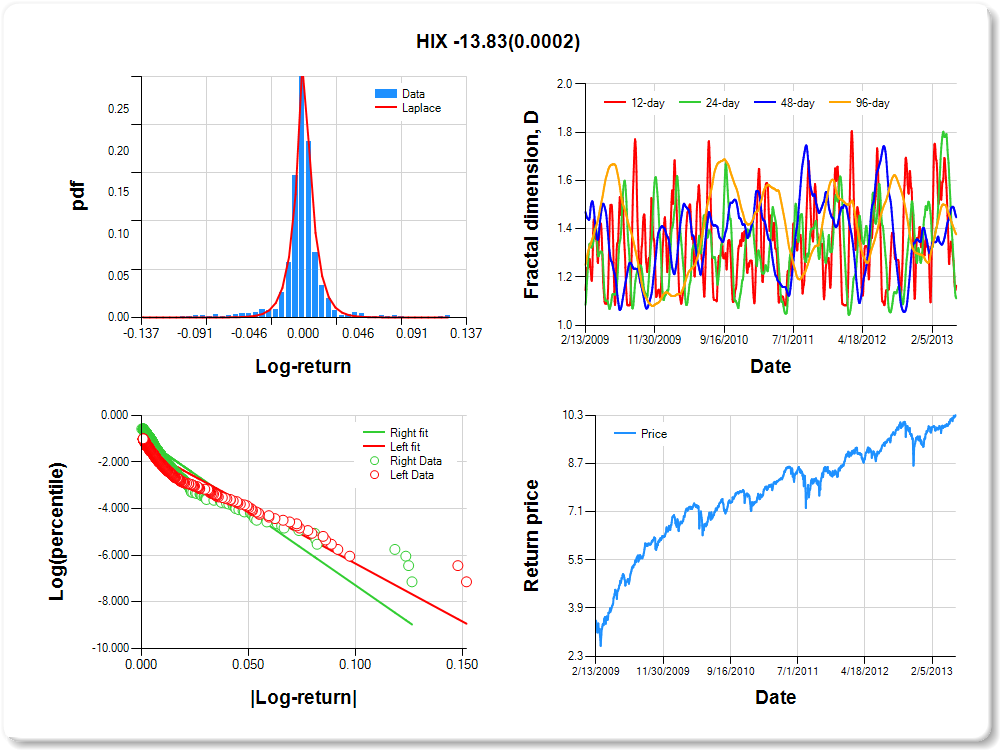

HIX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.08 |

-0.07 |

-0.02 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.02 |

0.06 |

0.08 |

0.88 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.188 |

0.096 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.386 |

0.056 |

-24.678 |

0.0000 |

|log-return| |

-49.598 |

2.508 |

-19.772 |

0.0000 |

I(right-tail) |

0.456 |

0.073 |

6.255 |

0.0000 |

|log-return|*I(right-tail) |

-13.829 |

3.649 |

-3.790 |

0.0002 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.836 |

0.888 |

0.552 |

0.623 |

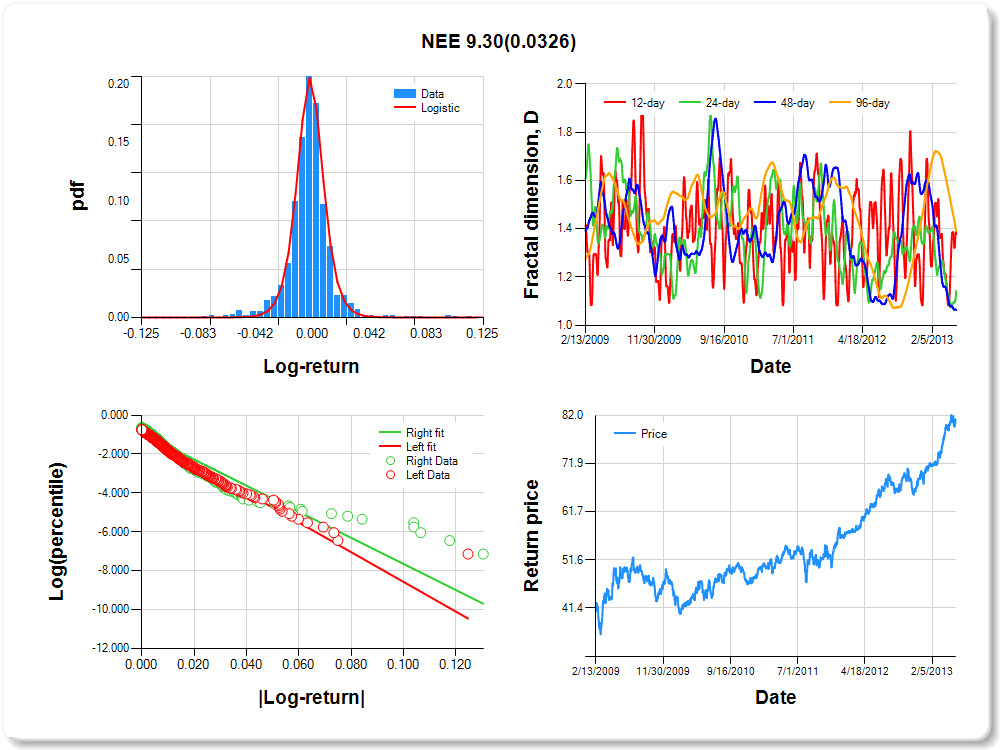

NEE

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.05 |

0.08 |

0.94 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.028 |

0.083 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.924 |

0.054 |

-17.159 |

0.0000 |

|log-return| |

-76.432 |

3.271 |

-23.369 |

0.0000 |

I(right-tail) |

-0.008 |

0.073 |

-0.109 |

0.9135 |

|log-return|*I(right-tail) |

9.297 |

4.345 |

2.140 |

0.0326 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.620 |

0.857 |

0.935 |

0.609 |

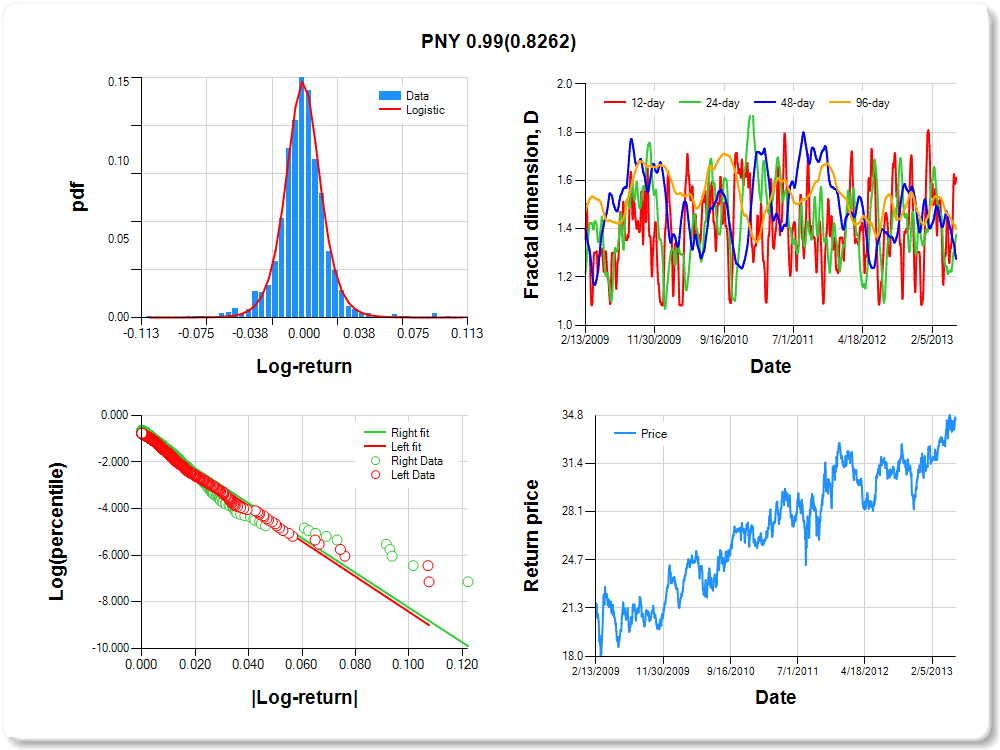

PNY

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.07 |

0.82 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.094 |

0.114 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.853 |

0.057 |

-14.922 |

0.0000 |

|log-return| |

-75.579 |

3.260 |

-23.182 |

0.0000 |

I(right-tail) |

0.081 |

0.078 |

1.044 |

0.2966 |

|log-return|*I(right-tail) |

0.987 |

4.494 |

0.220 |

0.8262 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.388 |

0.623 |

0.725 |

0.601 |

LLY

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.05 |

0.06 |

0.38 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.005 |

0.131 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.978 |

0.056 |

-17.501 |

0.0000 |

|log-return| |

-72.339 |

3.206 |

-22.565 |

0.0000 |

I(right-tail) |

0.219 |

0.076 |

2.885 |

0.0040 |

|log-return|*I(right-tail) |

-9.089 |

4.598 |

-1.977 |

0.0483 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.649 |

0.730 |

0.782 |

0.597 |

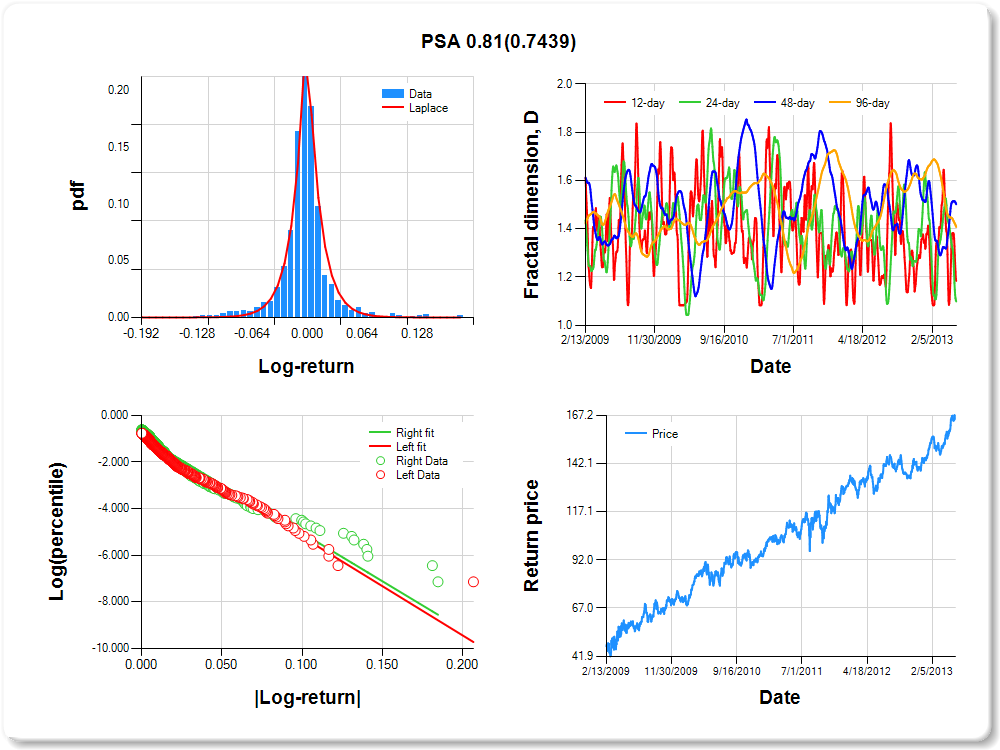

PSA

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.10 |

-0.09 |

-0.04 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.10 |

0.14 |

0.85 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.120 |

0.130 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.996 |

0.053 |

-18.726 |

0.0000 |

|log-return| |

-42.191 |

1.823 |

-23.150 |

0.0000 |

I(right-tail) |

0.089 |

0.072 |

1.240 |

0.2153 |

|log-return|*I(right-tail) |

0.812 |

2.484 |

0.327 |

0.7439 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.816 |

0.901 |

0.498 |

0.592 |

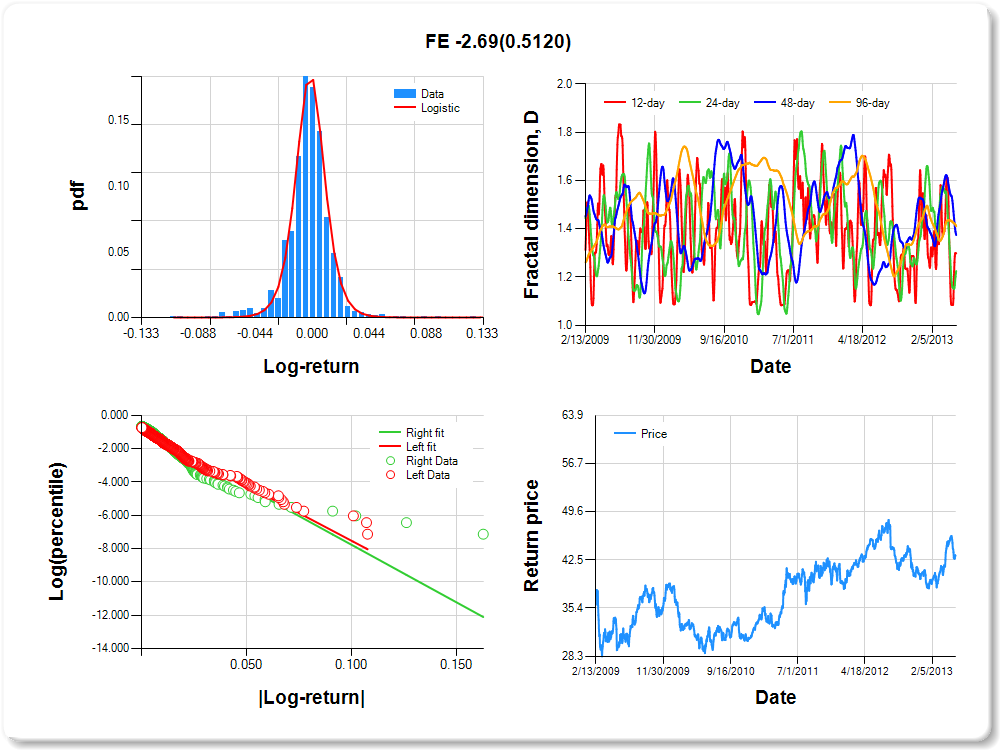

FE

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.06 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.06 |

0.16 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.338 |

0.092 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.897 |

0.054 |

-16.516 |

0.0000 |

|log-return| |

-66.309 |

2.815 |

-23.554 |

0.0000 |

I(right-tail) |

0.027 |

0.075 |

0.358 |

0.7203 |

|log-return|*I(right-tail) |

-2.691 |

4.104 |

-0.656 |

0.5120 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.702 |

0.775 |

0.626 |

0.590 |

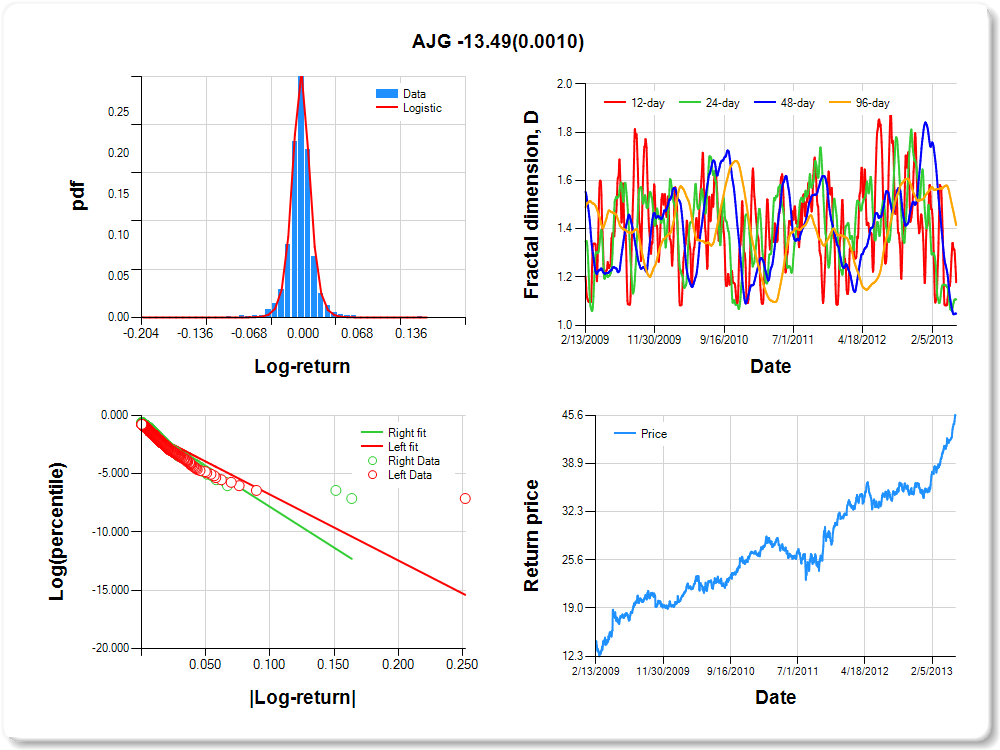

AJG

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.04 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.05 |

0.06 |

0.28 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.373 |

0.057 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.147 |

0.052 |

-22.087 |

0.0000 |

|log-return| |

-56.443 |

2.780 |

-20.305 |

0.0000 |

I(right-tail) |

0.301 |

0.073 |

4.122 |

0.0000 |

|log-return|*I(right-tail) |

-13.486 |

4.078 |

-3.307 |

0.0010 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.822 |

0.893 |

0.951 |

0.585 |

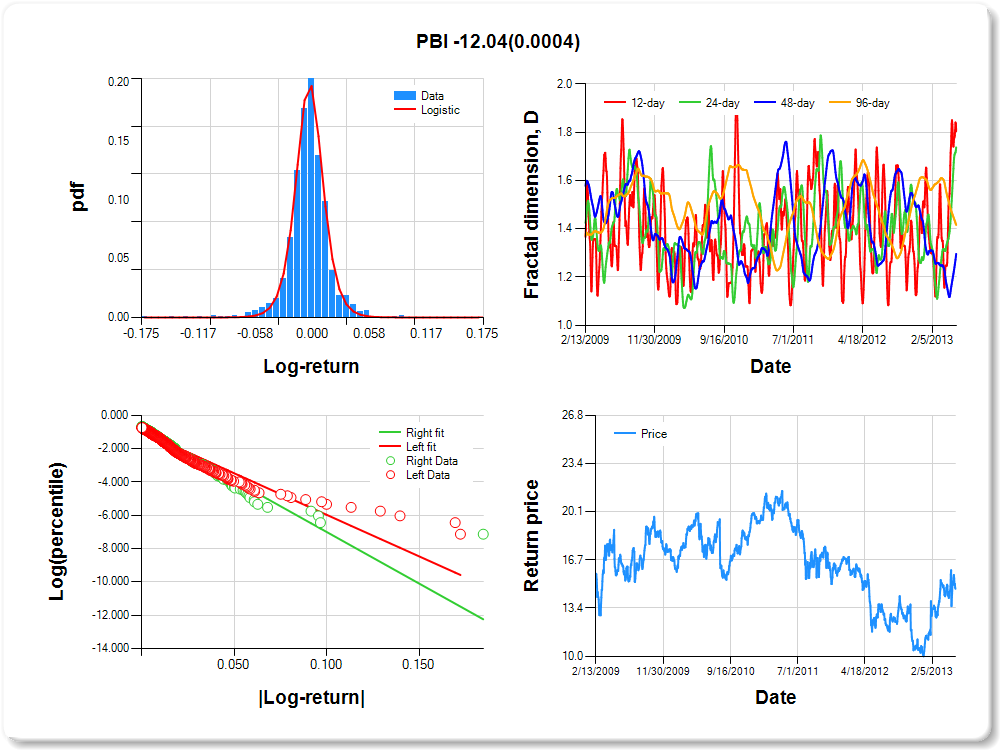

PBI

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.10 |

-0.06 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.06 |

0.06 |

0.11 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.055 |

0.086 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.974 |

0.053 |

-18.387 |

0.0000 |

|log-return| |

-49.854 |

2.195 |

-22.713 |

0.0000 |

I(right-tail) |

0.179 |

0.076 |

2.360 |

0.0184 |

|log-return|*I(right-tail) |

-12.037 |

3.402 |

-3.538 |

0.0004 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.195 |

0.262 |

0.704 |

0.584 |

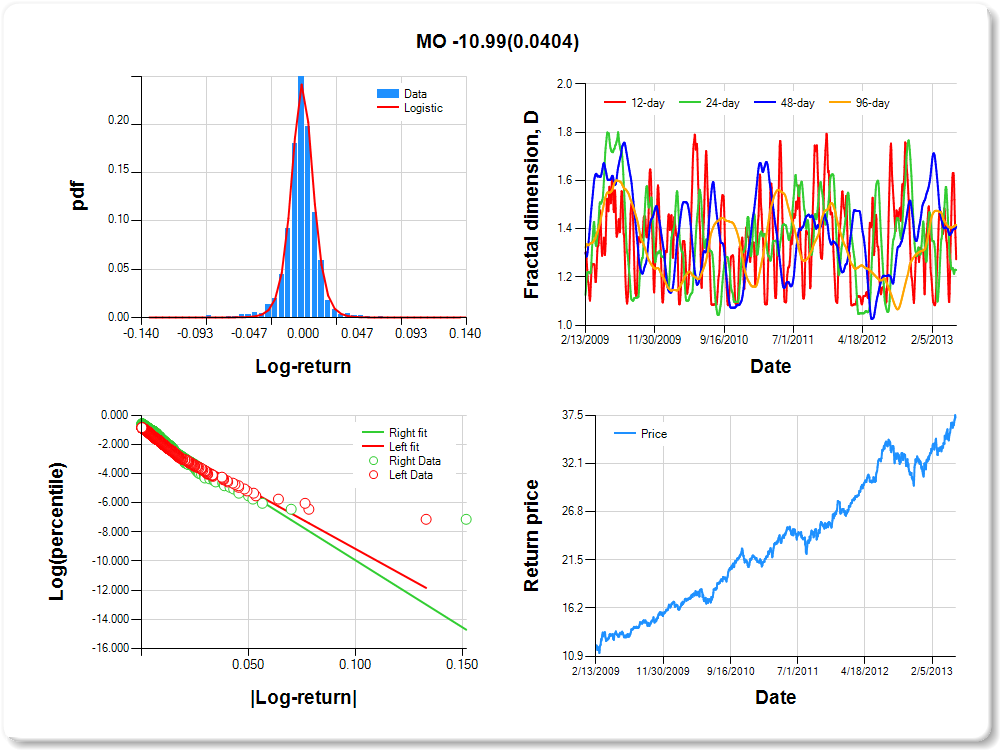

MO

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.05 |

0.00 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.096 |

0.072 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.056 |

0.056 |

-18.705 |

0.0000 |

|log-return| |

-80.933 |

3.744 |

-21.617 |

0.0000 |

I(right-tail) |

0.323 |

0.077 |

4.210 |

0.0000 |

|log-return|*I(right-tail) |

-10.993 |

5.357 |

-2.052 |

0.0404 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.726 |

0.770 |

0.589 |

0.584 |

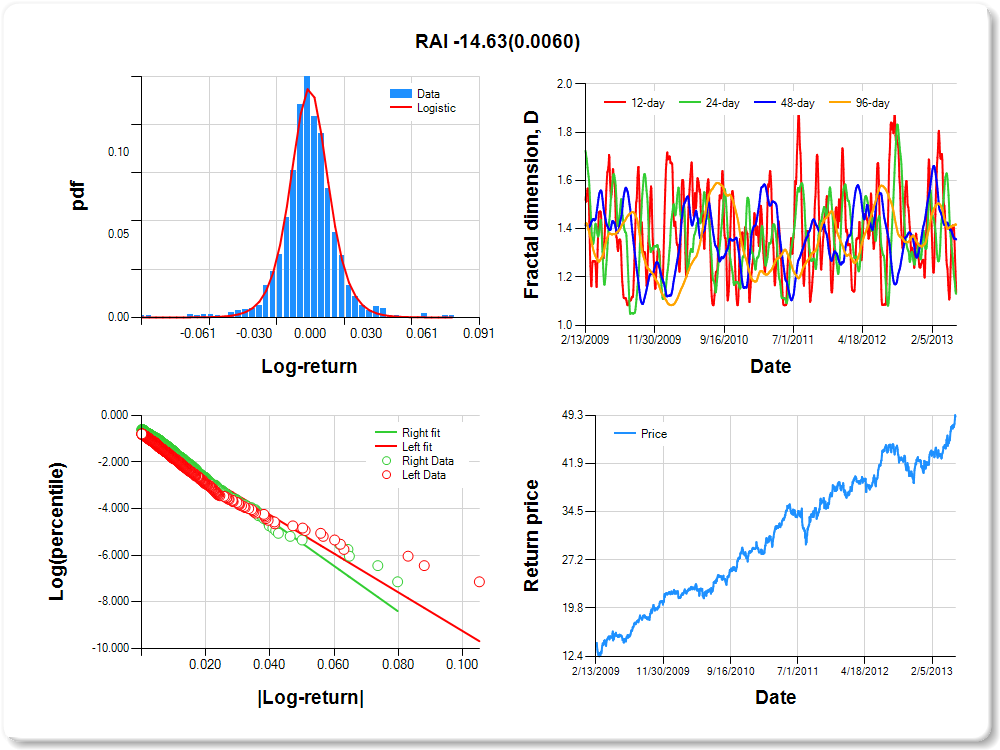

RAI

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

1.05 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.258 |

0.124 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.946 |

0.056 |

-16.794 |

0.0000 |

|log-return| |

-82.851 |

3.666 |

-22.600 |

0.0000 |

I(right-tail) |

0.351 |

0.079 |

4.437 |

0.0000 |

|log-return|*I(right-tail) |

-14.634 |

5.314 |

-2.754 |

0.0060 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.865 |

0.870 |

0.644 |

0.583 |

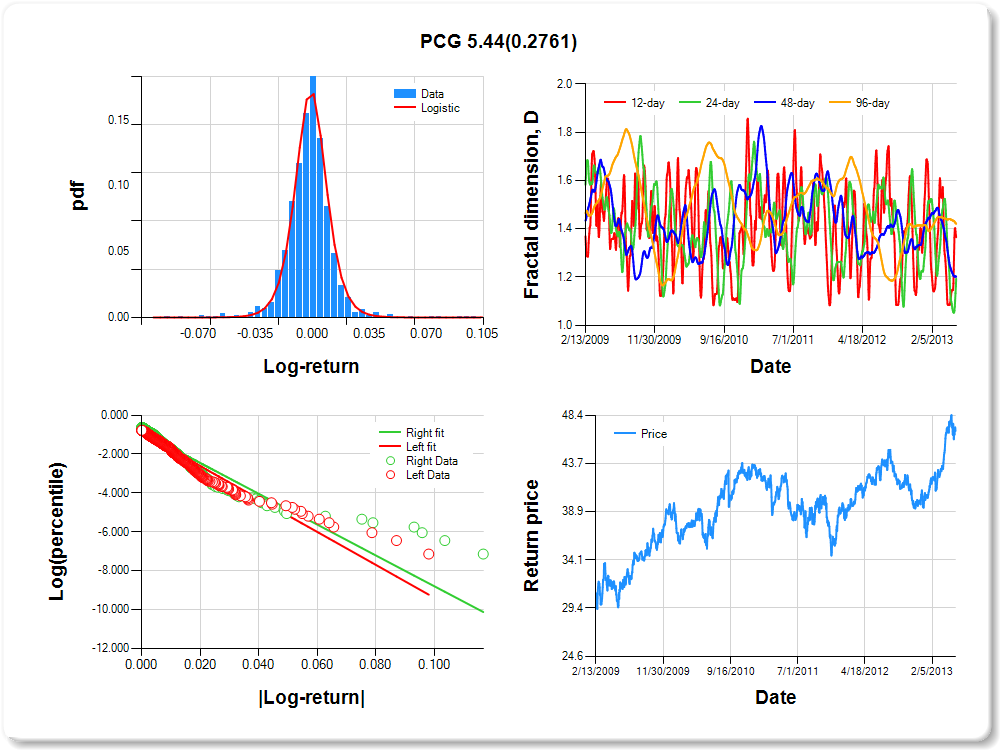

PCG

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.06 |

0.49 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.130 |

0.099 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.908 |

0.056 |

-16.198 |

0.0000 |

|log-return| |

-84.701 |

3.708 |

-22.844 |

0.0000 |

I(right-tail) |

0.049 |

0.075 |

0.655 |

0.5127 |

|log-return|*I(right-tail) |

5.438 |

4.991 |

1.090 |

0.2761 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.635 |

0.807 |

0.799 |

0.580 |

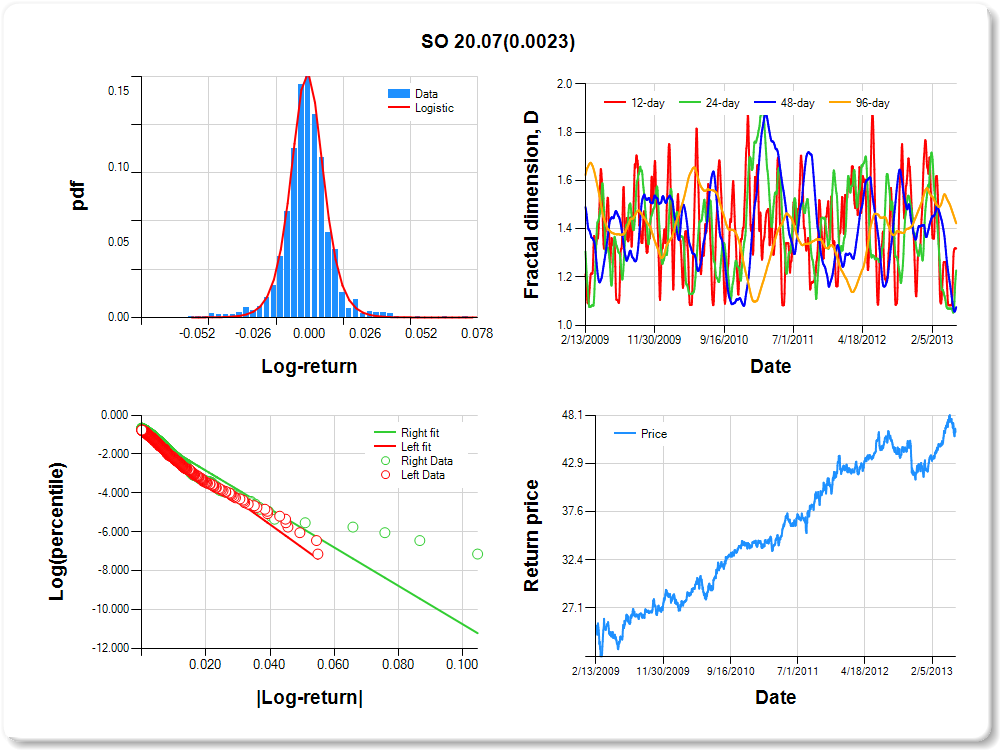

SO

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.02 |

0.04 |

0.04 |

0.56 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.524 |

0.105 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.847 |

0.057 |

-14.947 |

0.0000 |

|log-return| |

-118.729 |

5.068 |

-23.428 |

0.0000 |

I(right-tail) |

-0.013 |

0.077 |

-0.175 |

0.8611 |

|log-return|*I(right-tail) |

20.075 |

6.583 |

3.050 |

0.0023 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.682 |

0.772 |

0.925 |

0.577 |

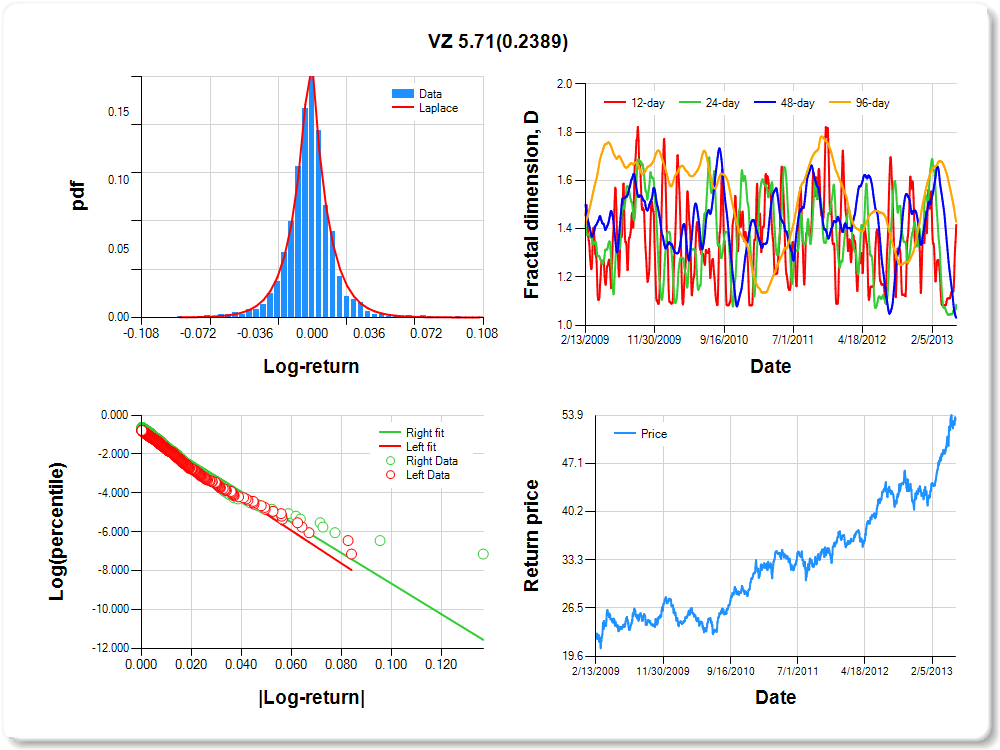

VZ

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.06 |

1.17 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.397 |

0.165 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.861 |

0.057 |

-15.047 |

0.0000 |

|log-return| |

-84.348 |

3.624 |

-23.274 |

0.0000 |

I(right-tail) |

0.078 |

0.077 |

1.012 |

0.3118 |

|log-return|*I(right-tail) |

5.707 |

4.844 |

1.178 |

0.2389 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.584 |

0.915 |

0.969 |

0.571 |

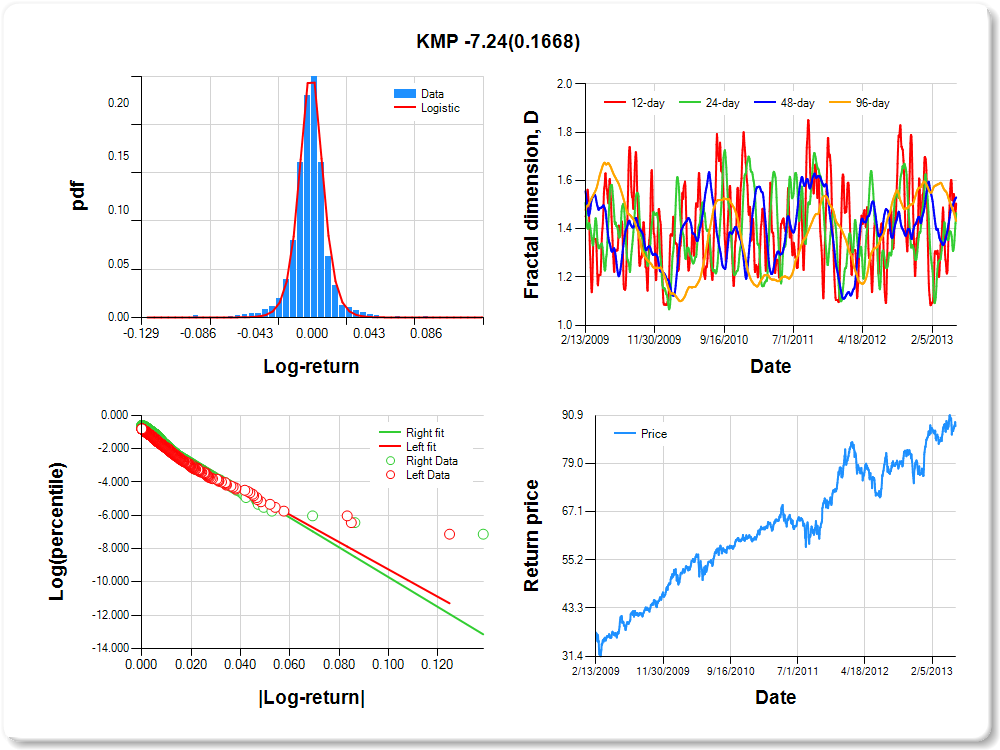

KMP

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

0.82 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.068 |

0.074 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.037 |

0.055 |

-18.867 |

0.0000 |

|log-return| |

-82.095 |

3.716 |

-22.092 |

0.0000 |

I(right-tail) |

0.262 |

0.075 |

3.483 |

0.0005 |

|log-return|*I(right-tail) |

-7.240 |

5.234 |

-1.383 |

0.1668 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.495 |

0.534 |

0.469 |

0.568 |

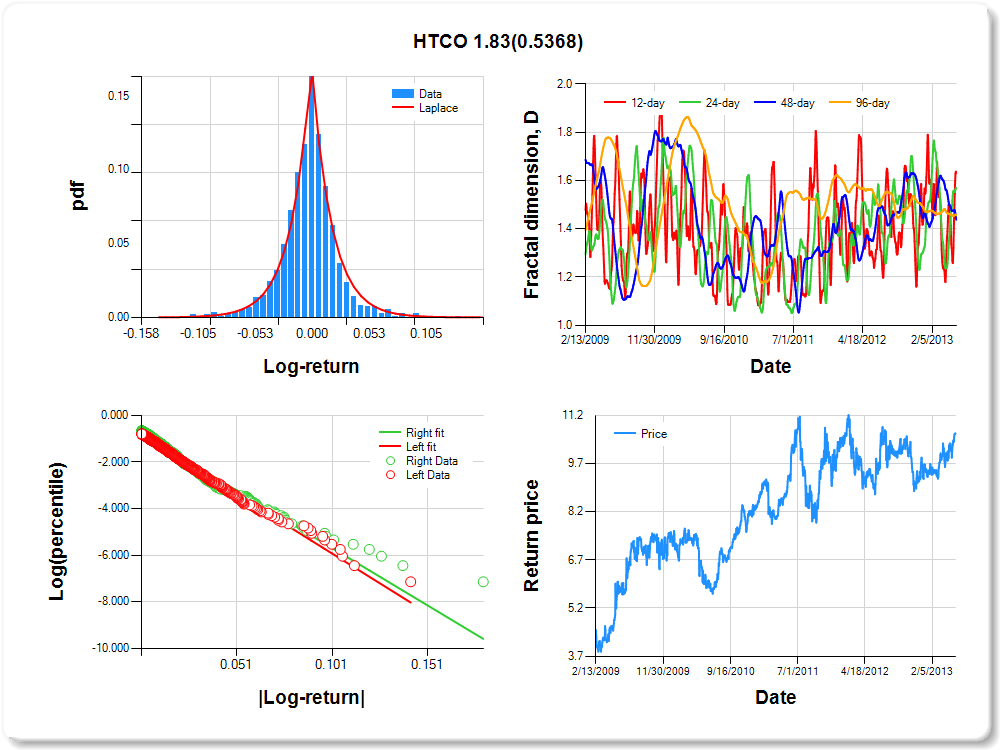

HTCO

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.09 |

-0.07 |

-0.04 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.08 |

0.10 |

1.03 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.180 |

0.197 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.800 |

0.060 |

-13.320 |

0.0000 |

|log-return| |

-50.835 |

2.195 |

-23.162 |

0.0000 |

I(right-tail) |

0.050 |

0.081 |

0.620 |

0.5353 |

|log-return|*I(right-tail) |

1.835 |

2.969 |

0.618 |

0.5368 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.366 |

0.430 |

0.562 |

0.545 |

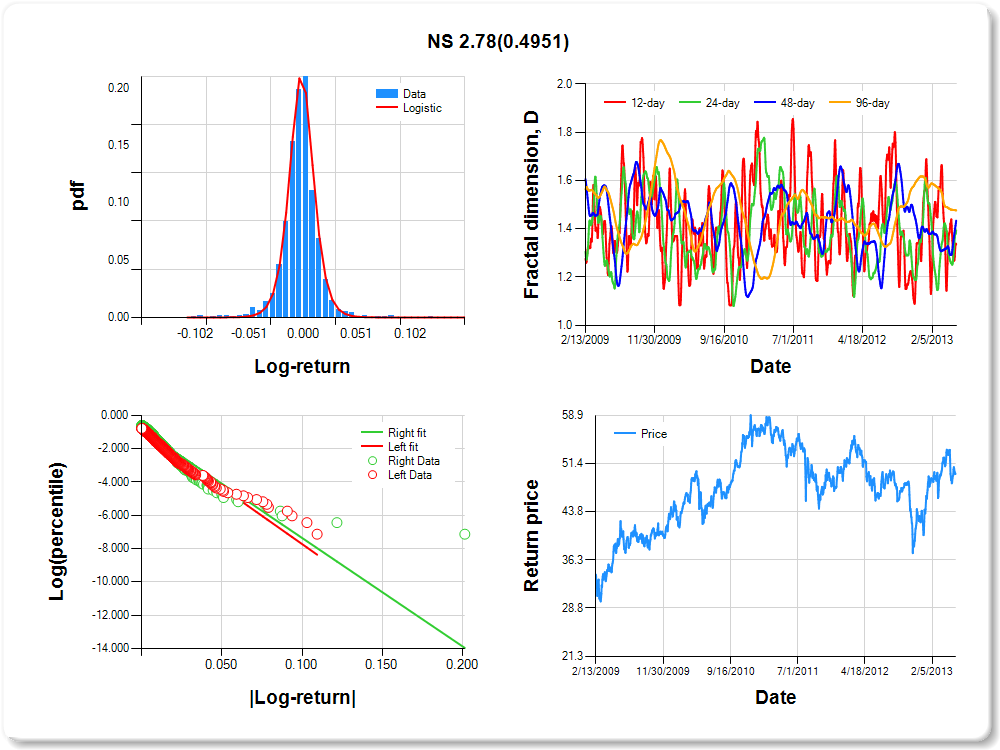

NS

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.08 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.05 |

0.06 |

0.03 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.492 |

0.081 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.946 |

0.056 |

-16.943 |

0.0000 |

|log-return| |

-67.779 |

2.973 |

-22.798 |

0.0000 |

I(right-tail) |

0.090 |

0.075 |

1.204 |

0.2290 |

|log-return|*I(right-tail) |

2.778 |

4.071 |

0.682 |

0.4951 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.664 |

0.606 |

0.566 |

0.524 |

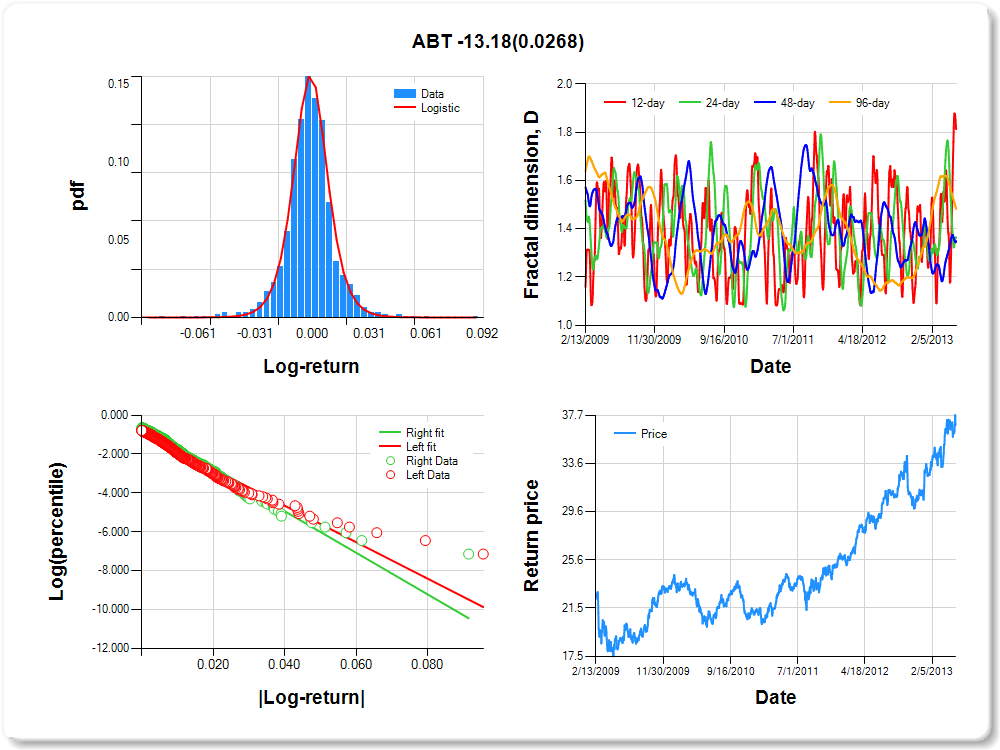

ABT

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.04 |

0.00 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.052 |

0.110 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.880 |

0.057 |

-15.377 |

0.0000 |

|log-return| |

-93.807 |

4.093 |

-22.917 |

0.0000 |

I(right-tail) |

0.249 |

0.080 |

3.097 |

0.0020 |

|log-return|*I(right-tail) |

-13.181 |

5.946 |

-2.217 |

0.0268 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.186 |

0.635 |

0.651 |

0.518 |

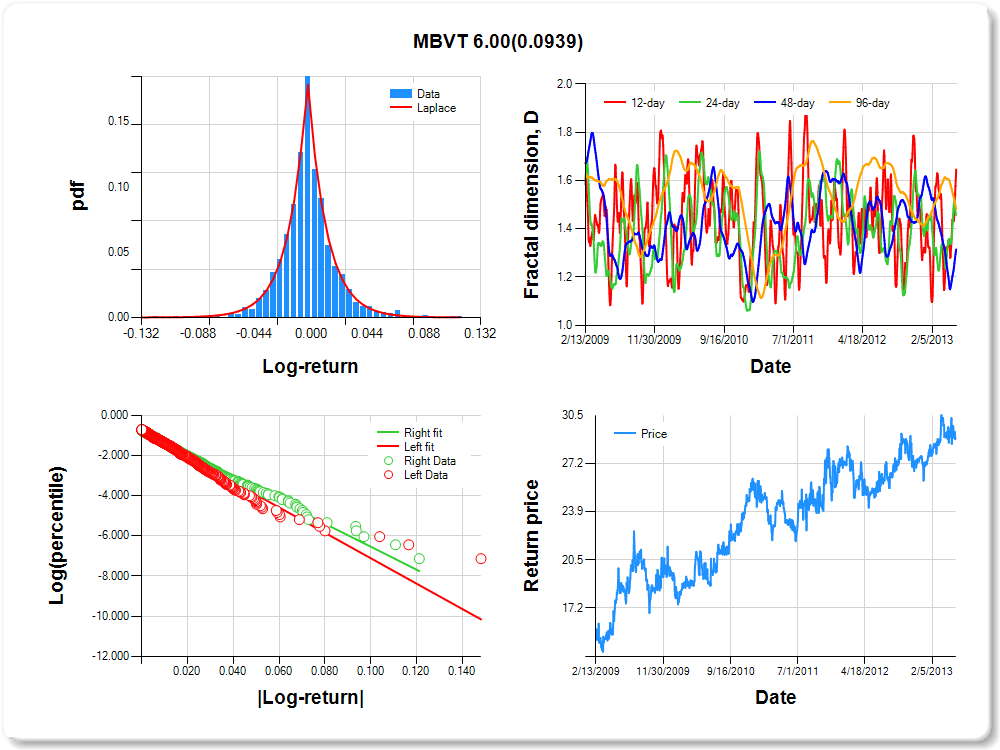

MBVT

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.07 |

0.08 |

1.81 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.168 |

0.187 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.779 |

0.056 |

-13.863 |

0.0000 |

|log-return| |

-63.180 |

2.651 |

-23.833 |

0.0000 |

I(right-tail) |

-0.027 |

0.080 |

-0.337 |

0.7364 |

|log-return|*I(right-tail) |

5.995 |

3.576 |

1.677 |

0.0939 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.354 |

0.542 |

0.685 |

0.517 |

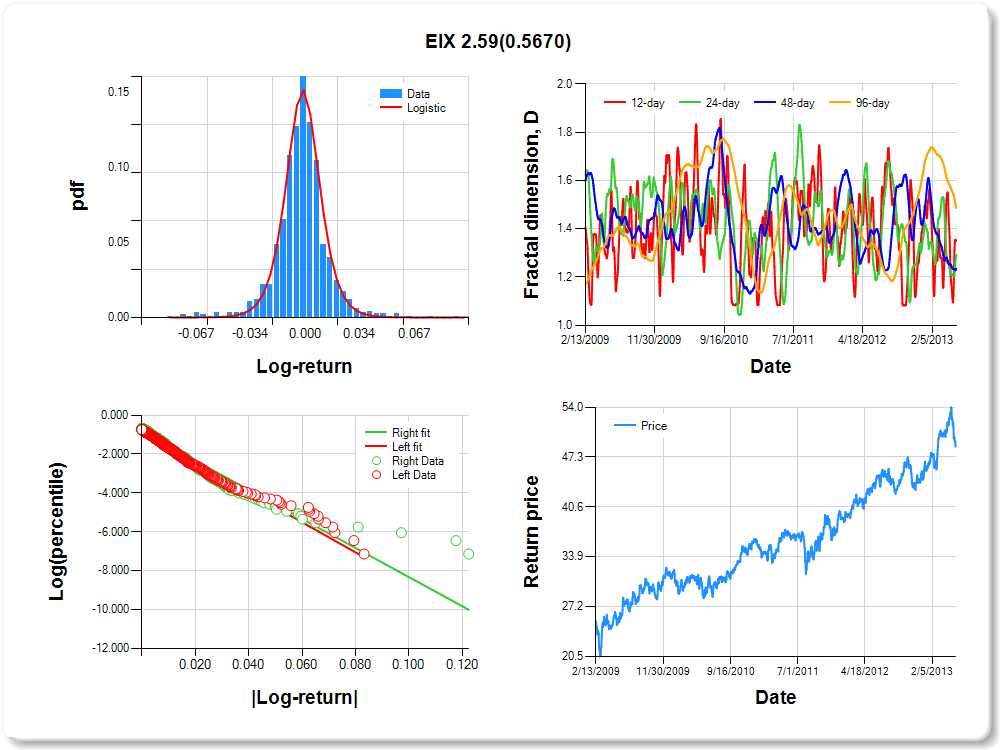

EIX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.05 |

0.06 |

0.13 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.317 |

0.113 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.842 |

0.055 |

-15.183 |

0.0000 |

|log-return| |

-77.479 |

3.269 |

-23.703 |

0.0000 |

I(right-tail) |

0.015 |

0.076 |

0.194 |

0.8461 |

|log-return|*I(right-tail) |

2.590 |

4.523 |

0.573 |

0.5670 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.649 |

0.707 |

0.765 |

0.514 |

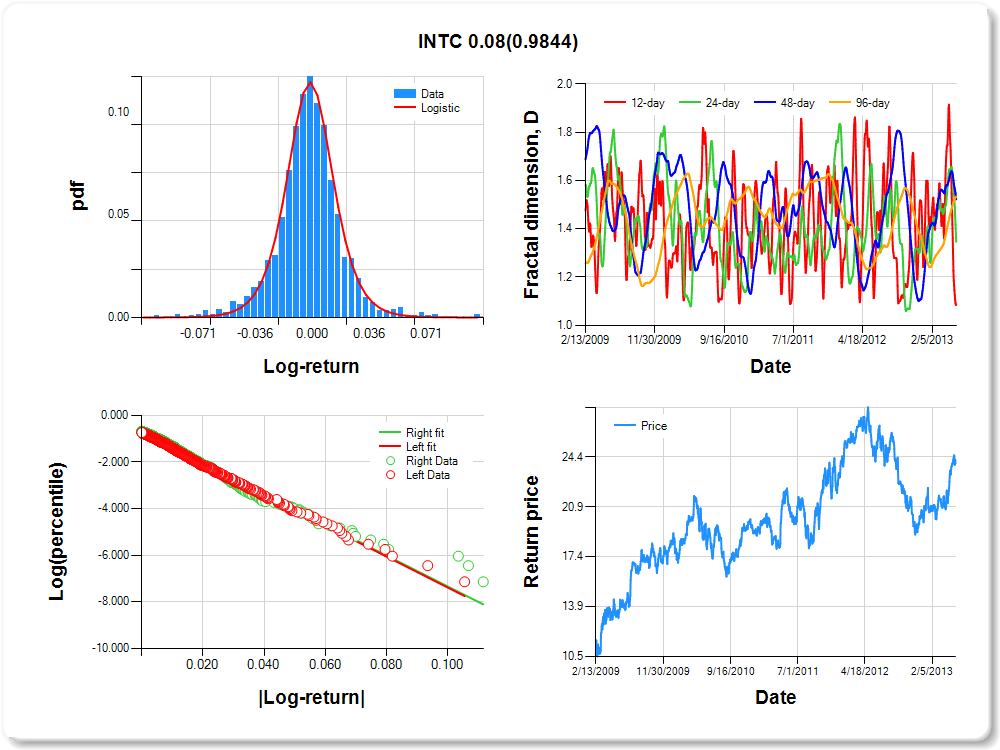

INTC

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.06 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.06 |

0.07 |

1.07 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.038 |

0.150 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.731 |

0.059 |

-12.460 |

0.0000 |

|log-return| |

-66.341 |

2.776 |

-23.901 |

0.0000 |

I(right-tail) |

0.039 |

0.081 |

0.475 |

0.6346 |

|log-return|*I(right-tail) |

0.076 |

3.878 |

0.020 |

0.9844 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.914 |

0.654 |

0.478 |

0.466 |

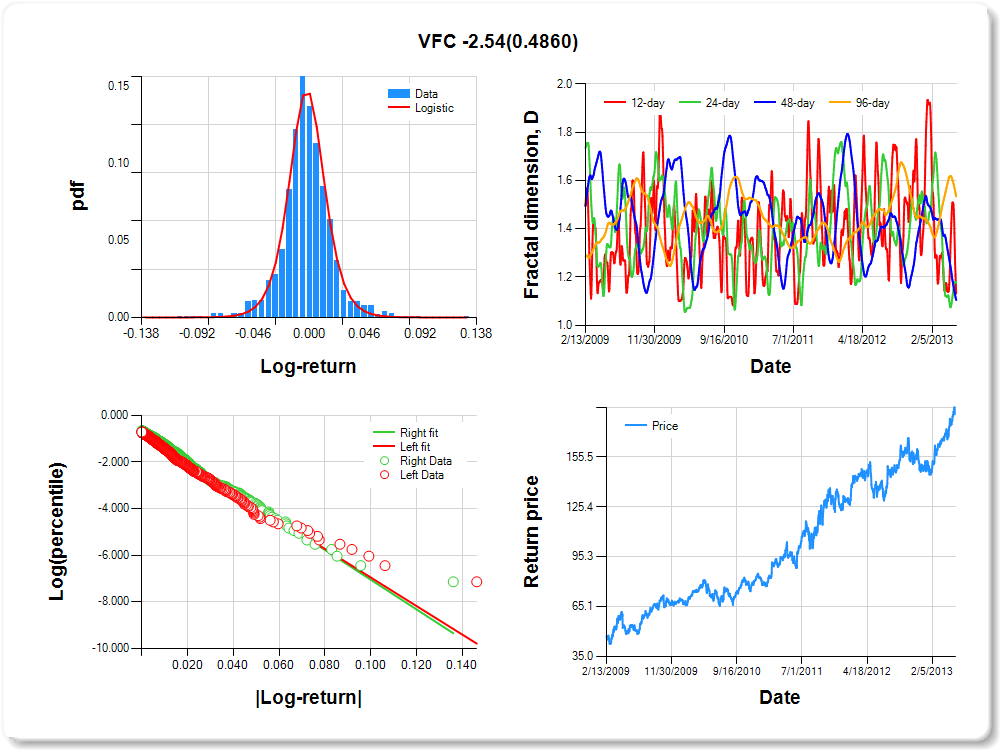

VFC

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.06 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.06 |

0.07 |

2.21 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.072 |

0.116 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.834 |

0.055 |

-15.231 |

0.0000 |

|log-return| |

-61.232 |

2.565 |

-23.869 |

0.0000 |

I(right-tail) |

0.160 |

0.078 |

2.042 |

0.0414 |

|log-return|*I(right-tail) |

-2.536 |

3.640 |

-0.697 |

0.4860 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.869 |

0.825 |

0.895 |

0.466 |

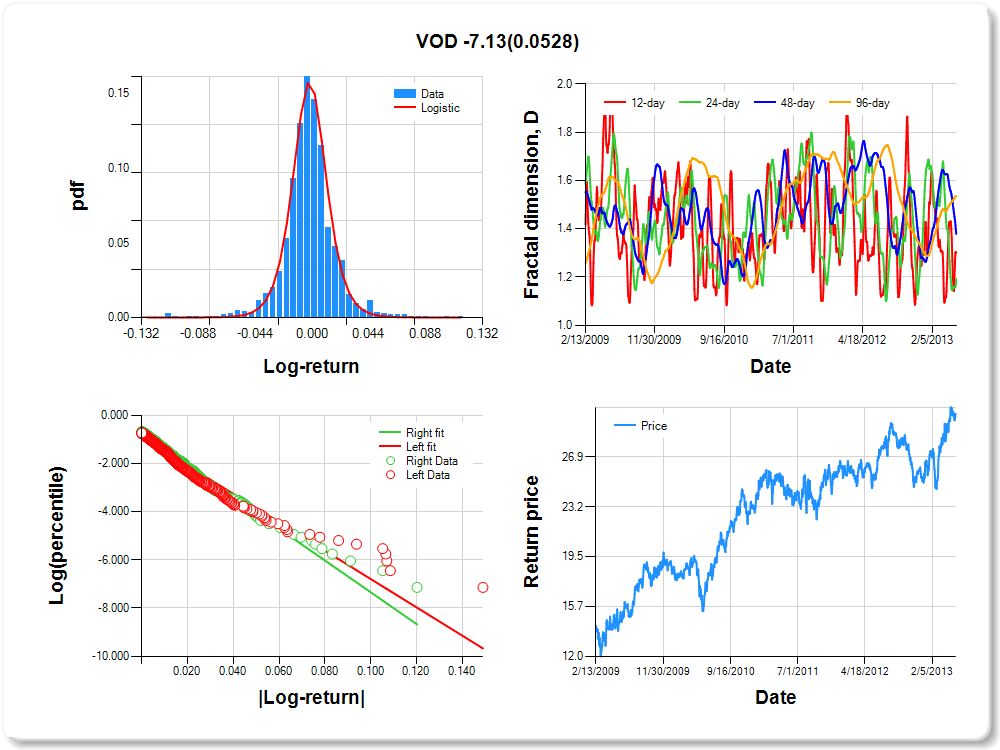

VOD

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.09 |

-0.06 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.06 |

0.08 |

0.98 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.190 |

0.108 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |